Cryptocurrency is considered a taxable asset in many jurisdictions, including the U.S., where residents are required to report income from crypto assets and pay the relevant taxes.

For example, selling tokens for a higher price than you bought them can incur capital gains taxes. Money from crypto staking is taxed at the ordinary income rate in some countries.

This article is a general guide to understanding when crypto assets are taxable and how they’re taxed. However, it’s always advisable to consult local tax authorities and professionals for detailed information.

Do you have to pay tax on crypto?

Tax implications for crypto assets ultimately depend on the laws of your country. Some countries don’t consider virtual currency a taxable asset, while others consider it taxable and have precise laws about the taxes incurred from crypto transactions.

In countries that levy taxes on crypto, residents are taxed at different rates depending on how their tokens were acquired. For example, buying and selling crypto for profit incurs a capital gains tax, while staking income is taxed at the ordinary rate. Capital gains taxes are often lower than ordinary income taxes.

If you send or receive crypto as a gift, it might be taxable above a specified threshold. You should verify what is considered taxable income with local tax professionals, ensuring compliance with the law.

Crypto tax in the U.S.

The Internal Revenue Service (IRS) is the agency responsible for tax collection in the U.S., and it has precise guidelines governing digital assets. The IRS requires reporting cryptocurrency transactions on your tax return and paying the relevant taxes. Let’s dive deeper into crypto tax in the U.S. and explore what is considered taxable and what is not.

Not taxable

- Buying and holding. Just purchasing and holding crypto isn’t a taxable event. You’ll only incur taxes if you sell the crypto at a profit or earn passive income from it.

- Receiving a gift. Getting crypto as a gift won't incur a tax until you sell the tokens for cash or earn staking income from them.

- Giving a gift. You can gift crypto without incurring taxes if you haven’t exceeded the $13.9 million lifetime gift tax exemption. If your gift exceeds $19,000 per recipient, you're required to file a gift tax return (without incurring a tax liability), and the amount will count towards the $13.9 million exemption threshold.

- Donations to registered non-profit organizations. Crypto donations to a registered 501(c)(3) charitable organization can reduce your tax liability, based on the donated amount.

Tax on crypto gains

- Selling crypto for fiat. You'll owe capital gains taxes whenever you sell tokens for cash at a profit. If you sell tokens at a loss, you may be able to deduct that loss from your general tax obligations.

- Conversions. When you convert one token to another, for example, BTC to ETH, the IRS considers this a taxable event. You'll owe taxes on crypto gains if you sold the token for more than you paid for it. This tax applies whether you sold the tokens for cash or in exchange for another token.

Capital gains are short-term or long-term, depending on the duration you hold the asset. If you sell crypto within a year of acquiring it, it’s considered short-term capital gains and taxed at the ordinary income rate.

If you hold the tokens for more than a year before selling them at a profit, it’s considered long-term capital gains and taxed at a lower rate than ordinary income.

Taxable as income

- Receiving payments in crypto. If you receive payments as an employee or contractor in cryptocurrency, it’s considered ordinary income and will be taxed according to your income tax bracket. The same applies to receiving cryptocurrency as a payment for goods and services.

- Mining crypto. Crypto mining rewards are considered income and taxed at the fair market value, i.e., the price of the coins when you receive them. If you run a crypto mining business, the gross proceeds are taxed as self-employment income.

- Staking rewards. If you lock your tokens on a blockchain and receive staking rewards, you’ll pay income taxes based on the fair market value of the tokens.

- Incentives. Crypto received as incentives, such as airdrops, hard forks, and referrals, is taxed as personal income. You'll need to report this crypto income and pay the relevant tax rate.

How is crypto taxed?

Taxes on crypto are paid directly to your domestic tax collection agency. Most jurisdictions accept tax payments only in fiat currency, so digital tokens must be converted into fiat currency before payment.

As mentioned, tax liabilities depend on how you acquired the token, whether as income or from short-term or long-term investments. You can estimate how much you’ll owe by calculating your income, gains, and losses. However, it’s advisable to consult a tax professional for the final say.

Tax-free crypto

U.S. residents can earn tax-free crypto in some cases.

- Capital gains exemption. If your total income (including crypto gains) is less than $48,350, you'll pay no short-term or long-term capital gains tax. However, you still need to report crypto transactions on your tax return.

- Loss deduction. Suppose you buy tokens and sell them at a loss. You can use the losses to offset your tax liability by up to $3,000 annually. Losses over $3,000 can be carried over and claimed in future years (within the $3,000-per-year limit) for tax optimization purposes.

Calculating crypto income

If you’re an employee working formally in the U.S., you’re likely used to having federal and state income taxes deducted directly from your pay stubs.

The income you earn from cryptocurrency, such as trading, mining, and staking, is subject to the same taxes, but isn't deducted directly. You'll have to report these earnings yourself and pay the required taxes, depending on your tax bracket.

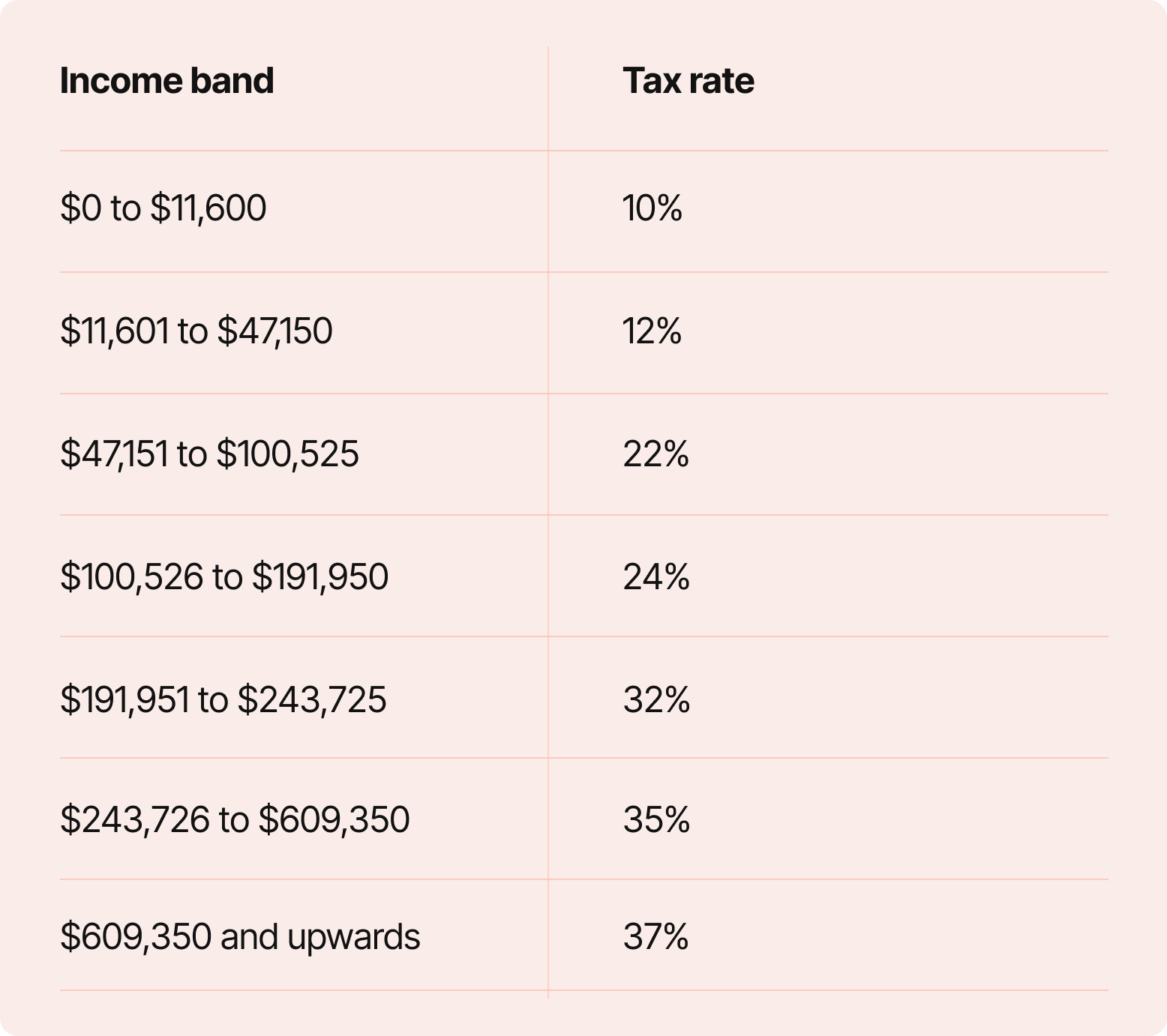

The table above shows the IRS’s income tax bracket guidelines as of 2025. You pay a percentage of your income in these brackets, and as your crypto income increases, the tax rate on the next bracket is higher.

Note that if your crypto income jumps to a higher bracket, you only pay the higher tax rate on the part in the new bracket, not the entire income.

For example, if you earn $90,000 in crypto, the first $11,600 is taxed at 10% and the next $11,601 to $47,150 is taxed at 12%. Only the amount above $47,150 ($90,000 − $47,150 = $42,850) is taxed at 22%. You can visit IRS.gov for more information on federal income tax brackets.

If you use a cryptocurrency exchange, you’ll likely be able to generate a detailed report about your earnings, including from virtual currencies, stablecoins, and non-fungible tokens (NFTs). You can then use this report as a guide when filling out tax forms and calculating your tax liability.

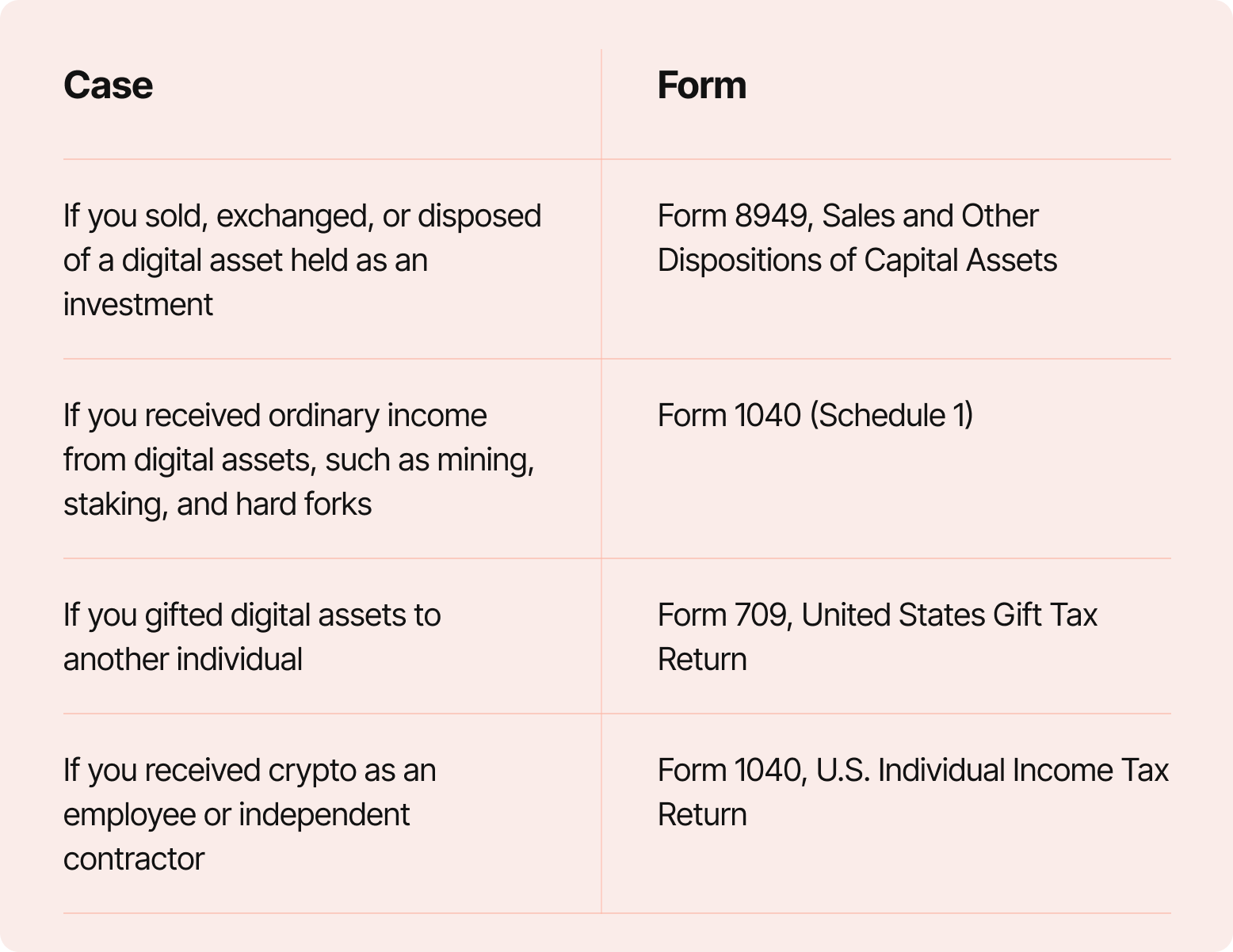

The table below outlines the tax forms applicable to various types of digital asset transactions for U.S. taxpayers:

Calculating crypto gains and losses

The key to calculating crypto gains and losses is knowing the cost basis, i.e., the amount you started with. When you sell crypto, subtract the cost basis from the sale price to determine the profit or loss.

For example, if you buy crypto for $12,000 and sell it for $15,000, your profit is the amount sold minus the cost basis ($15,000 − $12,000 = $3,000). In this case, you’ll pay capital gains taxes on $3,000 of income.

In contrast, if you sell the tokens for $10,000, you’d have incurred a $2,000 loss. You’re not liable for capital gains taxes, as you didn’t make any gain. You can report this $2,000 loss on your tax return and use it to offset up to $3,000 in tax on income earned from other sources.

Short-term capital gains for crypto

Capital gains taxes can be short-term or long-term, depending on how long you held onto your capital assets before selling them. If you hold your tokens for less than a tax year before selling, you'll incur a short-term capital gains tax on the profits.

Short-term capital gains are taxed at your ordinary income rate, depending on the volume of profits. The top federal income tax bracket is 37%, so you could pay up to that if you sold tokens at a high profit.

Long-term capital gains for crypto

If you hold onto your tokens for over a year before selling them, you’ll generally pay a lower tax rate on the crypto sales profits. Investments held for over one year are considered long-term capital gains and taxed at reduced rates of 0%, 15%, or 20%, depending on your income.

If you’re wondering why, the government levies lower taxes on long-term capital gains to encourage longer-term investments in the economy. Another reason is that long-term capital gains are partly inflationary, so a lower tax rate creates an incentive to make long-term investments even during times of high inflation.

Can the IRS track your cryptocurrency?

Yes, the IRS can track your cryptocurrency assets. It’s a federal tax agency with the power to subpoena cryptocurrency exchanges and banking institutions for information about individuals.

All crypto exchanges serving U.S. residents are legally required to conduct Know Your Customer (KYC) checks. Hence, you’ll need to provide identification documents to trade and withdraw your funds seamlessly. Exchanges also keep records of all customers’ transactions, which can be provided to the IRS upon request.

U.S. citizens and residents are required to report crypto transactions to the IRS and pay taxes on relevant income and profits. Failure to do this may result in an extensive tax audit or prosecution for tax evasion.

Crypto tax in the U.K.

HM Revenue & Customs (HMRC) is the U.K.'s tax collection authority. According to its guidelines, digital assets are treated like shares and taxed accordingly. Hence, residents are required to pay income or capital gains taxes on crypto transactions where applicable.

Capital gains

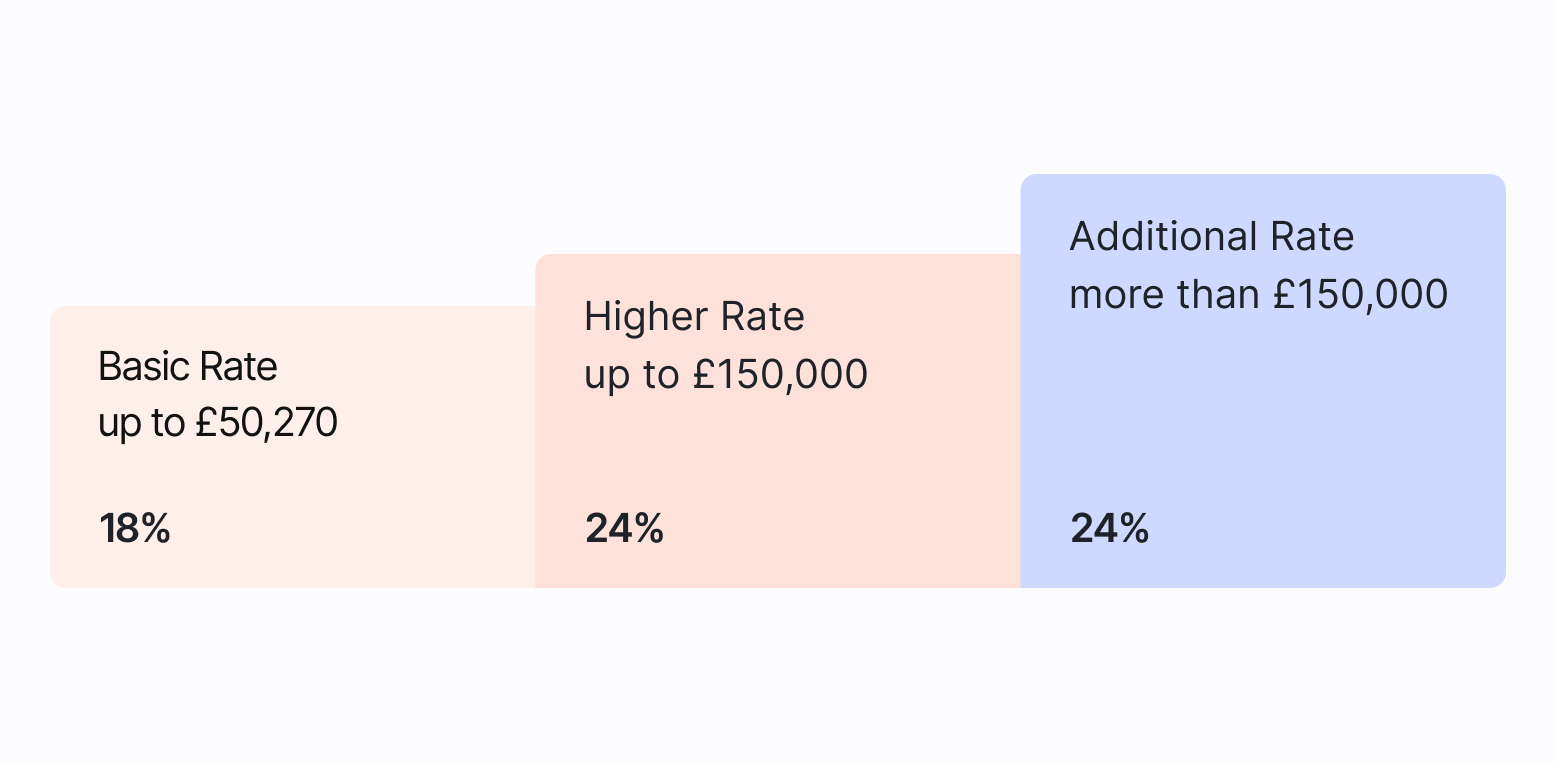

U.K. taxpayers have an annual capital gains tax-free allowance of £3,000. If your profits exceed this level, you're required to pay capital gains taxes, depending on the amount.

Income

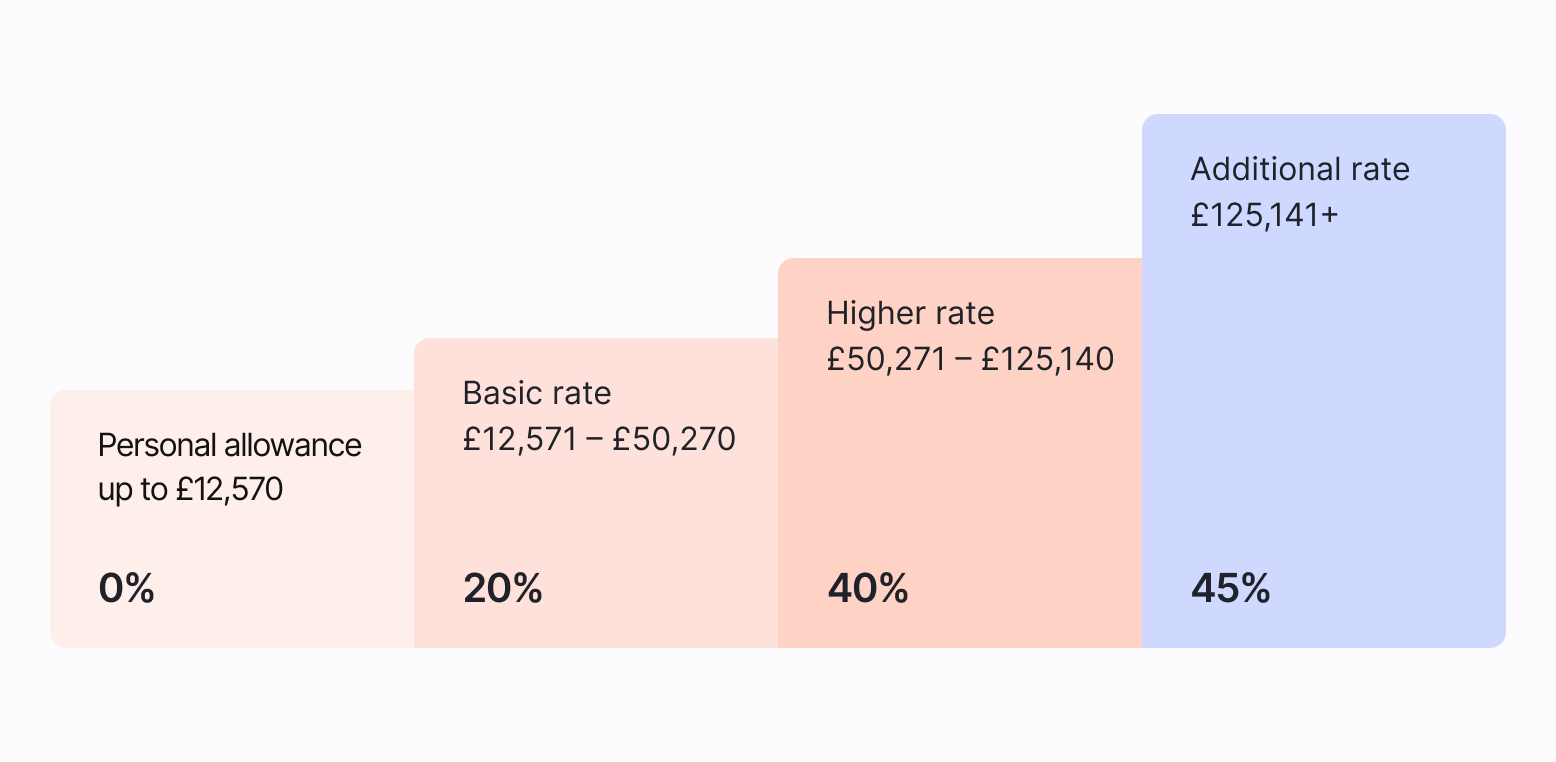

Income earned from cryptocurrency ventures, such as mining and staking, is taxed at the ordinary income rate by HMRC, based on the fair market value of the cryptocurrency at the time of the transaction. The same applies to cryptocurrency earned in exchange for goods and services, i.e., personal income.

The first £12,570 of annual income is tax-free for U.K. residents. After this band, the tax rate varies depending on the amount of cryptocurrency earned. You can check the HMRC’s official guidance for further information on crypto tax in the U.K.

When you may need to pay taxes on crypto

According to HMRC guidelines, U.K. taxpayers are liable for capital gains tax when they

- Sell cryptocurrency for cash

- Exchange cryptocurrency for another type of asset, e.g., selling BTC for USDT.

- Spend cryptocurrency to pay for goods or services.

- Transfer crypto to another person (except a declared spouse or civil partner).

- Donate tokens to a charity.

Notably, taxpayers can deduct certain costs from their capital gains, such as transaction fees and the cost of drafting a contract for the transaction.

U.K. taxpayers are also required to pay income taxes when they

- Stake cryptocurrency and earn yields.

- Mine cryptocurrency.

- Accept cryptocurrency as payment for labor, goods, and services.

For example, if you mine 0.5 BTC, you’ll recognize the fair market value of 0.5 BTC based on the current price and pay income tax. The same applies to receiving staking rewards or accepting tokens directly for goods or services. How to report and pay

To report capital gains from crypto transactions, U.K. taxpayers can either

- Use the Capital Gains Tax (CGT) real-time service to report their profits immediately.

- Complete a Self Assessment tax return at the year's end and include the transaction details. The same tax return is used to report ordinary income earned in crypto.

HMRC requires separate records for each transaction, including the type of tokens, the number of tokens sold, the date of sale, and the fair market value of the tokens in pounds sterling. Further data can be requested if the HMRC decides to conduct a compliance check.

Crypto tax software can assist you in keeping track of your transactions and how much tax you owe.

FAQ

What is the tax on crypto gains

The tax on cryptocurrency gains depends on your jurisdiction and the length of time you held the assets.

For example, the U.S. charges a 37% tax on short-term gains (on assets held for one year or less) and 15% to 20% on long-term gains (on assets held for more than one year).

In contrast, the U.K. charges 18% to 24% on capital gains and doesn’t have the distinction between short-term and long-term gains like the U.S.

What happens if I fail to report my cryptocurrency taxes?

Failure to report cryptocurrency taxes can result in significant monetary consequences or even criminal prosecution. It’s advisable to comply with relevant tax reporting laws to avoid legal issues.

When do I need to report my crypto taxes?

Taxpayers are generally required to report gains earned from crypto trades and crypto payments received for goods and services. You’ll report the transactions in your tax return and pay the required taxes based on the type of transaction.

Do cryptocurrency exchanges send tax forms?

Yes, cryptocurrency exchanges send data forms to tax agencies in compliance with local laws.

For example, if a U.S. taxpayer earns more than $600 in crypto, crypto exchanges are required to report their transactions to the IRS as “miscellaneous income,” using a Form 1099-MISC.

.svg)

-2.png)