Most guides treat multisig as a personal security upgrade. If you run payouts for an exchange, an iGaming brand, or a brokerage, that framing misses the point. Multisig wallets for institutions solve a governance problem: no single employee should be able to move client funds, treasury reserves, or settlement balances on their own authority.

A multisignature wallet requires M of N designated keys to approve a transaction before it broadcasts. That simple rule turns key management into an organizational control: it reduces insider risk, enforces dual authorization on material transfers, and leaves an approval trail compliance teams can show to auditors and regulators.

We'll map M-of-N thresholds to organizational roles, walk through approval queues and signing workflows, compare multisig with MPC for high-volume payment operations, outline sector-specific architectures, and show how the right configuration supports MiCA, Travel Rule, and FCA custody expectations.

Key Takeaways

- For institutions, multisig functions less as a personal security tool and more as a governance layer for controlling high-volume treasury and payout operations.

- Different M-of-N thresholds let institutions match signer requirements to wallet tiers, from fast hot-wallet payouts to stricter reserve and board-level transfers.

- When comparing multisig with MPC, payment-focused businesses should weigh on-chain transparency and policy control against latency, flexibility, and operational complexity.

- Approval queues separate routine payouts from large treasury movements, cutting internal fraud risk while preserving speed where it matters.

- Because multisig creates shared authorization and immutable approval records, it supports segregation of duties, audit readiness, and Travel Rule-aligned processes.

What Multisig Wallets Actually Do for Institutional Operations

Institutional multisig operationalizes segregation of duties: several named approvers must sign before funds move, which directly addresses insider fraud and unauthorized transfer risk.

Chainalysis reported $3.4 billion stolen across crypto in 2025, with the Bybit breach alone accounting for $1.5 billion, and most major service losses still trace back to compromised keys and social engineering rather than broken smart contracts. A single compromised key on a single-signature wallet is a total loss. The same key under a 3-of-5 policy is a contained incident.

The real value, though, is workflow control. A well-designed multisig setup governs payout approvals, treasury rebalancing, address whitelisting, and policy enforcement across hot, warm, and cold wallet tiers. Finance proposes, compliance reviews, security signs. The wallet enforces your internal control framework in code rather than in a PDF nobody reads.

Implementation paths differ by chain, and that matters for planning. Bitcoin supports native multisig at the script level. EVM chains typically rely on smart-contract wallets such as Safe. TRON offers permissioned accounts with weighted keys. Each route carries different fee profiles, recovery procedures, and integration work, so evaluating crypto wallet types for business use should happen before you commit to an architecture.

How the M-of-N Threshold Model Maps to Organizational Governance

Threshold selection is a governance decision first and a technical one second. Signers map to roles, departments, geographies, and business continuity requirements, so the question isn't "how many signatures?" but "which functions must agree before value moves?"

Lower thresholds improve speed for routine operations. Higher thresholds reduce key-person risk for reserves and exceptional transfers. Before locking in any model, evaluate quorum failure scenarios, staff availability across time zones, and signatory succession when people leave.

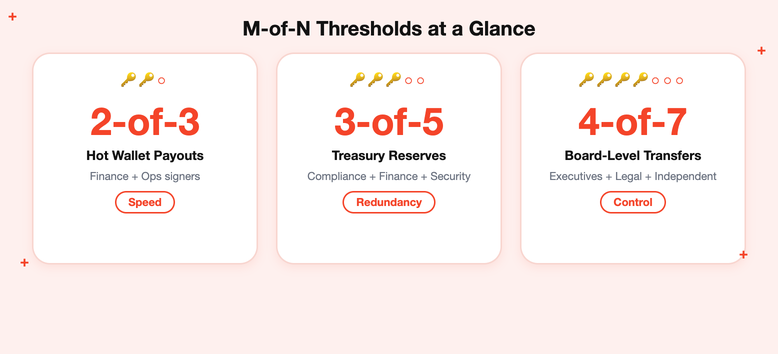

2-of-3 Configurations for Operational Hot Wallets

The 2-of-3 setup is the standard operational hot-wallet pattern: one signer in finance, one in operations, and a backup key held separately, often offline or with a custody provider. It keeps daily withdrawals fast because any two available approvers can clear the queue.

One warning from practice: colocated keys or overlapping administrators quietly nullify the governance benefit. If the same person controls two devices, you've built an expensive single-signature wallet.

3-of-5 Configurations for Treasury Reserves

A 3-of-5 policy is the common treasury reserve model. It balances redundancy with control across compliance, finance, security, and sometimes an external custody participant. Losing one or even two keys doesn't strand funds, yet no small clique can move reserves alone.

Geographic separation matters here. Signers in different locations, with at least one key in offline storage, keep the treasury recoverable through travel, outages, or personnel changes.

4-of-7 Configurations for Board-Level or Large Transfers

Reserve 4-of-7 for board-level governance: acquisition settlements, exchange listing deposits, or transfers large enough that evidentiary control matters more than speed. Seven signers across executives, legal, and independent parties create a decision record no individual can fabricate.

The tradeoff is real: stronger oversight slows settlement. Pair this model with preapproved emergency procedures and escalation paths so a genuine crisis doesn't stall behind an unreachable director.

[[aa-cta]]

📢 Tier Your Treasury Without Slowing Your Payouts

B2BINPAY Enterprise Wallets combine hot, warm, and cold tiers with role-based approvals in one regulated platform.

[[/a]]

Multisig vs. MPC: A Decision Framework for High-Volume Businesses

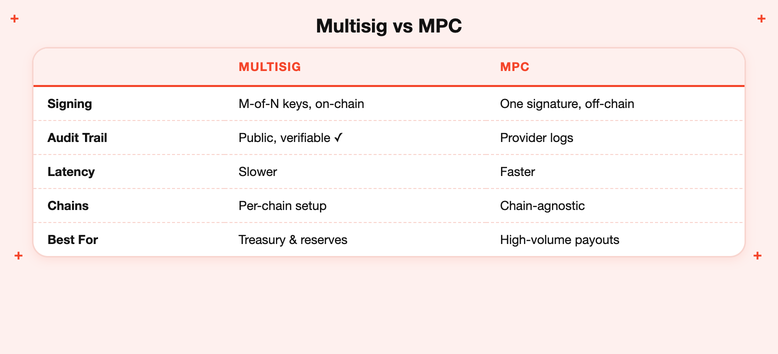

Here's the buyer question in one line: choose multisig when visible on-chain policy and auditable approval trails matter more than minimum signing latency. Multisig publishes its governance rules on-chain, where reviewers, counterparties, and regulators can verify them independently.

MPC (multi-party computation) takes the opposite route. It splits one private key into shares held by multiple parties, who jointly produce a single signature off-chain. Understanding how MPC wallets distribute private key shares helps clarify the tradeoff: MPC signs faster and works identically across chains, but its approval logic lives inside the provider's software rather than on a public ledger.

For orientation, Safe is the reference smart-contract multisig on EVM chains, while Fireblocks is the familiar MPC benchmark. The practical decision comes down to transaction profile:

- High-frequency, low-value flows (thousands of withdrawals daily): on-chain multisig latency and per-signature fees become prohibitive; MPC or a tiered hybrid wins.

- Treasury and reserve movements: multisig's transparent policy and immutable approval record outweigh its slower settlement.

- Regulated entities facing audits: on-chain proof of dual control is easier to evidence than a vendor attestation about key shares.

Most high-volume payment businesses end up with both: MPC-style speed at the hot tier, multisig control over reserves.

How Approval Queues and Signing Workflows Operate in Practice

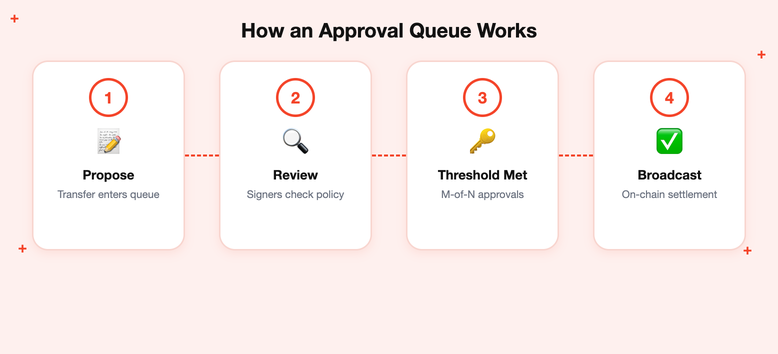

The workflow is concrete: a proposed transaction enters an approval queue, designated signers review it against policy, and the transaction broadcasts only after the threshold is met. Nothing moves because one person clicked a button.

Queues are what make multisig usable at volume. They support dual control, exception routing, and audit evidence for payment teams that can't manually approve every payout.

Automation handles the routine: spending limits, address whitelists, risk scoring, and callback-based status updates accelerate standard flows without surrendering governance. A withdrawal to a whitelisted address under the daily limit clears quickly; anything unusual routes to human reviewers.

Routine Payout Flows vs. Large Treasury Movements

Run two lanes. Low-value batch payouts use lower thresholds and faster approvals. Treasury sweeps and large transfers trigger higher thresholds and stronger verification.

B2BINPAY structures its own operations this way: approval queues govern on-chain payouts, while exceptional transfers face manual review and video-confirmed checks before release. Knowing how businesses hold and withdraw crypto assets across tiers is the foundation this dual-lane model builds on.

[[aa-cta-grey]]

📢 Automate Routine Payouts, Keep Dual Control

Wallet-as-a-Service from B2BINPAY pairs API-driven payout automation with approval workflows your compliance team defines.

[[/a]]

Sector-Specific Multisig Architectures

Multisig design should follow your transaction profile, client money rules, and settlement urgency. One template rarely fits every vertical. Here's how the model changes across three institutional profiles.

Crypto Exchanges: Hot, Warm, and Cold Wallet Tiering

Exchanges run a three-tier model: hot wallets for customer withdrawals, warm wallets for intraday rebalancing, and cold multisig reserves for long-term holdings and disaster recovery. Thresholds scale with the tier: perhaps 2-of-3 on hot, 3-of-5 on warm, 4-of-7 on cold. Operators also need reconciliation, whitelist controls, and clean integration between withdrawal APIs and scheduled treasury sweeps.

iGaming Operators: Player Fund Segregation and Dual-Control Withdrawals

iGaming operators must segregate player funds from operating balances, process frequent withdrawals, and keep dual control over higher-risk payouts. Multisig supports approval rules around VIP withdrawals, fraud-review holds, and strict separation between safeguarded player funds and the operating treasury. When a licensing authority asks how player balances are protected, a distinct multisig wallet with named signers beats an internal ledger entry.

Forex and CFD Brokers: Crypto Settlement With Distributed Signing Authority

For brokers, the issue is settlement governance. Client funding, hedging balances, and omnibus reserves move between crypto and fiat constantly, so signing authority should be distributed between treasury, compliance, and finance. Controlled approvals make it far easier to reconcile crypto inflows, conversions, and fiat settlement obligations, particularly when auto-conversion is settling exposure into EUR or USD on every inbound payment.

[[aa-cta-blue]]

📢 Settle Crypto Flows With Compliance Built In

B2BINPAY combines AML screening, Travel Rule KYT, and instant fiat settlement via SEPA and SWIFT under regional licences.

[[/a]]

How Multisig Satisfies Regulatory Requirements

Compliance is an architecture outcome, not a checkbox. Multisig helps regulated entities evidence segregation of duties, controlled approvals, and recoverable key management, which is precisely what supervisors look for in custody arrangements.

Under MiCA Article 75, crypto-asset service providers in the EU must maintain a custody policy that minimizes the risk of client asset loss through fraud, cyber threats, or negligence, and must segregate client assets from their own. A documented multisig policy with role-mapped signers is strong supporting evidence for both.

The FATF Travel Rule adds identity and transfer-metadata obligations; per the FATF's June 2025 update, 99 jurisdictions have passed or are progressing Travel Rule legislation, so payment flows increasingly need KYT screening wired into the approval workflow itself. FCA-style custody expectations in the UK point the same direction: clear organizational arrangements and records that prove control.

Be honest about the limitation: multisig alone doesn't make you compliant. It generates the immutable approval history that auditors rely on for internal controls testing, incident reviews, and regulator-facing reporting, but it must sit alongside KYC, transaction screening, and reporting systems.

Build Your Institutional Multisig Infrastructure With B2BINPAY

Running signing policies, payout automation, compliance screening, and fiat settlement across separate vendors is how gaps appear. B2BINPAY brings them together: Custody with multisig protection and video-confirmed withdrawals, Wallet-as-a-Service for API-driven payout operations, and a DeFi App for teams that need governed access to on-chain markets, all operating under regional licences with AML and Travel Rule KYT built in.

That's the practitioner's difference. B2BINPAY runs approval queues, tiered wallets, and dual-control policies for its own regulated operations across 350+ cryptocurrencies and 20+ blockchains, then gives clients the same infrastructure with a flat 0.5% processing fee and 0% rolling reserve.

[[aa-cta]]

Are You Evaluating Custody Architecture This Quarter?

Start where the governance already works. Onboarding is automated and takes less than 24 hours.

[[/a]]

Frequently Asked Questions about Multisig Wallets for Institutions

What is the difference between multisig and MPC wallets for institutions?

Multisig wallets require several independent signatures on-chain before funds move, while MPC produces one signature from distributed key shares behind the scenes. For institutions, multisig usually offers clearer approval logs and simpler policy enforcement, while MPC helps when low-latency signing matters. The better fit depends on whether your priority is auditability for payouts and treasury governance, or speed for continuous transaction flows.

How do multisig wallets work for corporate treasury management?

In corporate treasury, a multisig wallet turns key control into a workflow: one employee proposes a transfer and other authorized signers approve it. That model separates routine payouts from larger reserve movements by using different thresholds, wallet tiers, and approval queues. For high-volume businesses, it also creates cleaner reconciliation because proposal, approval, and broadcast events are logged alongside settlement and swap activity.

Are multisig wallets compliant with MiCA and Travel Rule requirements?

Multisig wallets are not compliant by default, but they support compliance by enforcing segregation of duties, controlled approvals, and durable audit trails. For MiCA and Travel Rule programs, the critical issue is connecting signing workflows with identity checks, transaction screening, and transfer metadata. In practice, institutions need multisig plus KYT, KYC, reporting, and policy controls rather than a wallet acting as a standalone compliance system.

What are the risks of multisig wallets for institutions?

The main risks are quorum failure, poor key recovery planning, signer collusion, and operational delays when critical approvers are unavailable. Institutions reduce that exposure with tested succession procedures, geographically separated keys, HSM-backed custody, and lower thresholds only for tightly limited hot wallets. You also need a migration plan for signer changes, because personnel turnover can lock funds if governance isn't updated quickly.

What should institutions look for when choosing multisig wallets for high-volume payment operations?

Focus on approval queues, role-based permissions, hot and warm wallet tiering, and API support before you compare signer counts alone. For payment businesses, the right platform should connect multisig governance with payouts, swaps, reporting, and compliance checks in one operating flow. That is why B2BINPAY positions multisig within broader wallet infrastructure, where treasury controls and execution speed can be balanced realistically.

Disclaimer: The service has legal and jurisdiction limitations. Please check T&Cs on https://b2binpay.com/en/risk-disclaimer

.svg)