Wallet infrastructure is a payments system layer, not a storage feature. For processors and exchanges running on-chain settlement at scale, the wallet stack determines who can move funds, which chains generate revenue, and whether compliance teams can produce audit-grade evidence on demand.

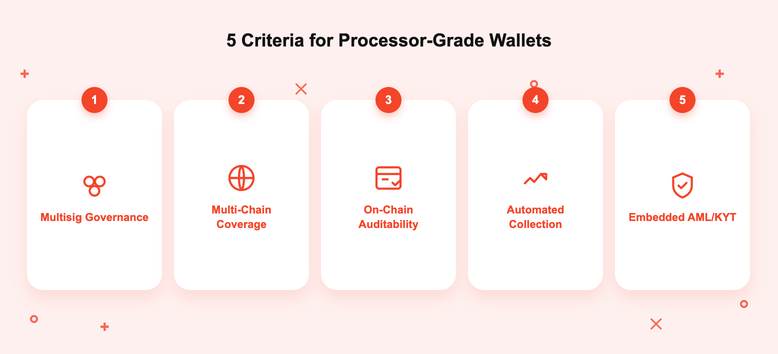

This guide evaluates wallet infrastructure on five operator-grade criteria: multisig governance, multi-chain coverage, on-chain auditability, automated fund collection, and embedded AML. It assumes you already understand private keys, hot and cold storage, and blockchain settlement.

For context on why crypto rails complement traditional PSP stacks, see Why Should PSPs and Crypto Payment Processors Work Together?.

Key Takeaways

- Business wallet infrastructure must include multisig controls, tiered team permissions, and configurable approval workflows to reduce insider-risk exposure on high-value outflows.

- Relying on exchange-custodied wallets can limit on-chain auditability, creating compliance blind spots for regulated processors managing high-volume settlement.

- Multi-chain coverage directly affects which customer segments a processor can serve, making broad blockchain support an operational revenue consideration.

- Automated deposit address generation and fund sweeping can dramatically reduce manual reconciliation overhead for processors handling thousands of daily transactions.

- AML and KYT monitoring embedded at the wallet layer can support real-time compliance controls more effectively than bolted-on screening tools.

Personal Wallets vs. Business Wallet Infrastructure

Personal crypto wallets and business wallet infrastructure solve fundamentally different problems. A personal wallet manages one user's keys. Business infrastructure manages key policies, role-based permissions, multi-chain fund flows, and compliance obligations across thousands of daily operations, with internal signers, external auditors, and regulators all touching the same ledger.

Operators who apply personal-wallet criteria (app ratings, fingerprint unlock, mobile UI polish) to infrastructure selection expose themselves to governance failures, compliance gaps, and reconciliation bottlenecks at scale.

Why Individual Wallet Criteria Don't Scale

Individual wallet criteria assume one signer, low volume, and no compliance reporting. Operator criteria look different: API depth, callback configurability, role-based access, signature thresholds, and audit-trail completeness. A retail wallet asks whether one user can recover a seed phrase.

A business wallet must answer how four authorized signers rotate when an executive leaves, how outflow limits adjust for new payout customers, and how every transaction maps to an immutable audit record.

[[aa-cta]]

Ready to evaluate infrastructure built for high-volume on-chain operations?

[[/a]]

Why Payment Processors Need Purpose-Built Wallets

Payment processors face multiparty fund flows, intra-day liquidity demands, and continuous regulatory obligations that generic wallets were never designed to handle. Purpose-built infrastructure provides the policy engines, automation hooks, and compliance layers these operations require, from per-merchant deposit addresses to programmable approval chains for treasury sweeps.

Custodial exchange wallets create three structural problems. First, counterparty risk: the operator does not control keys, so a custodian's outage threatens settlement obligations. Second, audit-trail dependence: the custodian controls the ledger of record, so regulators must trust a third party rather than verify on-chain. Third, policy limits: most exchange wallets cannot enforce role-based approvals at the granularity a payments operation requires.

On-Chain Settlement Is Now a Core Payment Rail

On-chain settlement has shifted from speculative use case to mainstream payment rail. Triple-A's 2026 market report estimates stablecoin cross-border payments at $17.9 trillion globally, with $14.7 trillion flowing through B2B channels.

McKinsey's analysis of on-chain money architecture documents how banks, payment processors, and treasury platforms now integrate tokenized cash and stablecoin rails into core settlement infrastructure. Blockchain-based payment gateways route real merchant revenue at scale, so the wallet stack must support 24/7 uptime, sub-minute confirmation handling, and instant reconciliation against on-chain truth.

Multisig Controls and Team Access Management

Multisig wallet architecture requires multiple authorized signers before funds move, eliminating single points of failure and reducing insider-threat exposure. For processors managing large daily outflows, configurable approval workflows and tiered team permissions are non-negotiable operational controls.

Treat multisig as a governance architecture: who can approve, at what threshold, and how approval chains route across regions. A 2-of-3 policy might secure routine sweeps under $10,000, while 3-of-5 with executive participation might gate transfers above $250,000. The infrastructure must encode these rules in policy, not process documents.

How Multisig Reduces Insider Risk and Fraud

Multisig requires multiple signers before any transaction broadcasts, so no single team member can move funds unilaterally even if credentials are stolen. Modern processors layer this with patterns like BVNK's four-eyes approval, where two independent reviewers must confirm material outflows. B2BINPAY Custody applies the same logic with multisig wallets, layered with multi-factor authentication, video-confirmed withdrawals above defined thresholds, and address blocklists.

Multi-Chain Support as an Operational Requirement

Multi-chain support determines which customers a processor can serve. Supporting 20-plus blockchains through one vendor eliminates the overhead of managing separate point solutions for Ethereum, BNB Chain, TRON, Polygon, Avalanche, and Layer 2s. Each additional chain integration carries a maintenance tail across node infrastructure, RPC monitoring, and smart contract audits.

Chain Coverage and Customer Revenue Impact

A processor supporting only Bitcoin and Ethereum excludes customers transacting on Solana, TRON, BNB Chain, Polygon, and Layer 2 networks. iGaming operators concentrate on TRON for stablecoin payouts. Asian e-commerce flows lean on BNB Chain. DeFi-native businesses settle on Ethereum mainnet and Arbitrum. Excluding any network means rejecting real revenue.

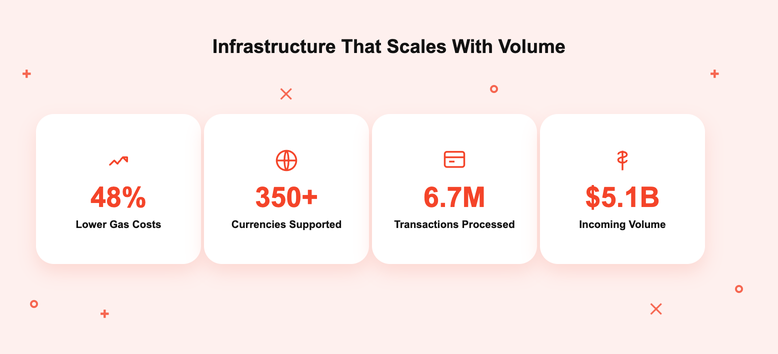

B2BINPAY's WaaS supports 350-plus currencies across major commercial chains, with automatic address duplication across compatible networks (such as ERC20 and BEP20) to reduce user-error losses. The fee model charges commission once per transaction rather than per chain hop, reducing gas costs by roughly 48% versus per-step pricing. For operators evaluating altcoin payment processor options, chain coverage and per-chain economics should be modeled together.

On-Chain Auditability and Reconciliation

On-chain wallet infrastructure creates immutable, verifiable transaction records directly on public blockchains. For regulated processors, that auditability supports regulatory reporting, internal audit trails, and back-office reconciliation without depending on a third party's ledger. When a regulator asks for proof of a settlement on a specific date, an on-chain record is verifiable in seconds.

When a processor relies on an exchange-custodied wallet, the audit trail is controlled by the exchange. Discrepancies between the operator's accounting and the custodian's records become reconciliation disputes that take weeks to resolve.

Immutable Records for Regulatory Reporting

On-chain transaction records cannot be altered retroactively, which makes them a stronger audit foundation than off-chain ledgers maintained by third-party custodians. Every transfer, contract call, and policy change is timestamped, signed, and replicated across thousands of nodes.

B2BINPAY Custody pairs that on-chain truth with real-time dashboards plus detailed monthly reports covering wallet balances, transaction history, and fees. For regulated operators preparing for audits, having both layers (immutable on-chain proof and structured back-office reporting) shortens preparation cycles and strengthens compliance posture.

[[aa-cta-blue]]

Need institutional-grade reporting on every transaction?

See B2BINPAY's onboarding flow

[[/a]]

Automated Fund Collection at Scale

Processors generating thousands of daily deposits across unique addresses cannot rely on manual fund collection. Automated sweep mechanics, configurable thresholds, and callback-driven reconciliation are the operational baseline for high-volume on-chain infrastructure.

At 10,000 daily deposits, manual collection becomes operationally infeasible: treasury teams watch block explorers, gas markets reward inefficient timing, and consolidation transactions stack into unmanageable queues.

Deposit Address Generation and Sweep Mechanics

Business-grade infrastructure generates unique deposit addresses per customer automatically, then sweeps incoming funds into a consolidated treasury address based on configurable thresholds and callback triggers. This removes manual reconciliation overhead and reduces gas costs by batching consolidation into fewer, larger transactions.

B2BINPAY's WaaS handles this end-to-end with automatic per-merchant address generation, configurable deposit thresholds, callback URL configuration, and a single-commission gas model. For technical integration depth, the Payment Gateway API guide details webhook patterns, sandbox testing, and error handling that processors should validate before committing to a vendor.

AML and KYT as Infrastructure-Level Requirements

AML screening and Know Your Transaction (KYT) monitoring must be embedded at the wallet infrastructure layer, not added as external tools after deployment. For regulated processors, transaction monitoring is an operational control that triggers real-time decisions such as holds, alerts, and address freezes.

Bolted-on AML means a separate vendor screens transactions after they post, generating retrospective reports days later. Embedded KYT means screening runs inline with transaction execution, with policy decisions enforced before funds leave the wallet. The first model produces compliance evidence. The second prevents compliance failures.

Why Compliance Must Be Embedded, Not Bolted On

Embedded compliance shifts AML and sanctions screening from periodic review into a continuous control surface. When KYT runs at the wallet layer, the same engine that signs transactions also enforces sanctioned-address blocks, high-risk flow holds, and Travel Rule data capture. FATF guidance specifically favors that design pattern for virtual asset service providers.

B2BINPAY runs KYT screening on every transaction across WaaS and crypto payment processing, layered with KYC controls during onboarding and address blocklists at the wallet level. B2BINPAY EL SALVADOR S.A. DE C.V. operates under a CNAD PSAD registration and Central Reserve Bank PSB authorization, supervised by SSF. B2BINPAY MAURITIUS LTD holds VASP licence GB24203002 under the Virtual Asset and Initial Token Offering Services Act 2021.

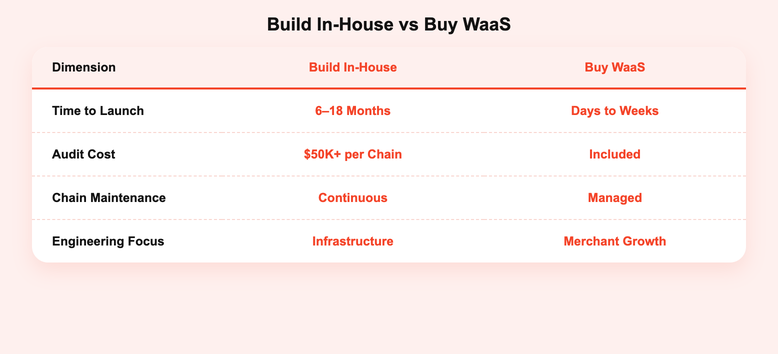

Build vs. Buy: In-House Wallet Costs

Building multisig, multi-chain infrastructure in-house requires sustained engineering investment, third-party audits, and ongoing maintenance across every supported chain. Most processors underestimate that cost until they are mid-build.

Treat build versus buy as a long-horizon decision with three recurring cost categories: engineering, audit, and operations. For broader payment-gateway economics framing, the total-cost-of-ownership lens matters more than headline integration cost.

Engineering, Audit, and Maintenance Overhead

Three cost categories recur in in-house builds. First, smart contract audits per chain: each multisig contract requires independent security review, and every chain upgrade triggers a new audit cycle costing $50,000 to several hundred thousand dollars.

Second, key management maintenance: hardware security modules, key rotation, and disaster recovery testing run continuously. Third, chain-specific node infrastructure or RPC costs. These costs do not amortize: audits expire, chains hard-fork, and the team that ships v1 is rarely the team that maintains v3.

Time-to-Market and Vendor Risk Trade-Offs

A purpose-built WaaS typically integrates in days to weeks, while a production-ready in-house multisig system spans 6 to 18 months from architecture through audit. Every quarter spent building infrastructure is a quarter not spent on merchant acquisition.

Assess WaaS providers on uptime SLAs, incident history, financial stability, and regulatory registrations. B2BINPAY's dual licensing (VASP licence GB24203002 in Mauritius plus CNAD PSAD registration and Central Reserve Bank PSB authorization in El Salvador), combined with $5.1 billion incoming volume and 6.7 million transactions processed by 2025 across 983 business customers, provides the operating evidence that supports a buy decision.

How B2BINPAY's WaaS and Custody Meet the Criteria

B2BINPAY's wallet stack combines WaaS for high-volume processor flows with Custody for institutional storage. Together they form a non-custodial, regulated, multi-chain infrastructure layer that maps directly to the five evaluation criteria above.

Pricing is structured for commercial use at scale: coin transactions at 0.25–0.40%, token transactions at 0.35–0.50%, outgoing transactions at 0%, with crypto settlement immediate and fiat on T+1. SEPA payouts run at 0.50% with a €10 minimum and SWIFT at 0.50% with a €20 minimum. A sandbox lets engineering teams validate integrations fee-free before production cutover.

Audited Multisig Smart Contracts and Key Control

B2BINPAY Custody uses multisig wallets requiring multiple keys to authorize fund movement, with third-party security audits validating the contract layer. Withdrawal controls layer multi-factor authentication, video-confirmed transactions above defined thresholds, manual verification flows, and denylists. The non-custodial WaaS model keeps key control with the processor at all times.

350+ Currencies and Multi-Chain Operations

B2BINPAY supports 350-plus currencies across Bitcoin, Ethereum, BNB Chain, TRON, Polygon, Avalanche, Solana, Arbitrum, Optimism, and Base. Automatic address duplication across compatible networks (such as ERC20 and BEP20) prevents user-error losses when customers send identical tokens on parallel chains. The single-commission gas model charges once per transaction rather than per chain hop, reducing gas costs by roughly 48% versus per-step pricing.

Choose Infrastructure Built for On-Chain Operations

The five criteria that separate purpose-built infrastructure from generic alternatives are clear: multisig governance with role-based approvals, multi-chain coverage aligned with customer revenue, on-chain auditability that survives regulatory review, automated fund collection that scales past 10,000 daily deposits, and embedded AML and KYT screening. Infrastructure scoring well on all five is the operational foundation a processor needs to run on-chain settlement at institutional scale.

B2BINPAY is built as that foundation: a regulated, non-custodial infrastructure layer covering WaaS for high-volume merchant flows and Custody for institutional storage, with KYT on every transaction, 350-plus currencies, and licensed operating entities in El Salvador and Mauritius.

The fastest way to validate fit is to test the sandbox and review commercial terms against your transaction profile.

[[aa-cta-grey]]

Become a B2BINPAY client and start with infrastructure built for the operational reality of on-chain payments.

[[/a]]

Frequently Asked Questions about Best Wallet Infrastructure

What is the best wallet infrastructure for B2B payments?

The best wallet infrastructure for B2B payments combines non-custodial key control, multisig governance, embedded AML and KYT screening, and multi-chain coverage in a single API-driven layer.

Generic custodial wallets lack the approval workflows and on-chain auditability that regulated payment processors require. Platforms such as B2BINPAY's WaaS and Custody are designed for this operational profile, covering 350-plus currencies with built-in compliance controls.

Should payment processors use custodial or non-custodial wallet infrastructure?

Non-custodial architecture is generally the stronger choice for payment processors because it keeps key control inside the operator's own systems rather than delegating it to a third party. Custodial exchange wallets introduce counterparty risk and can limit on-chain auditability. A non-custodial model such as B2BINPAY's WaaS can help processors maintain independent audit trails and reduce exposure to vendor-side incidents.

What security controls matter most when evaluating wallet infrastructure for exchanges and payment platforms?

Multisig approval workflows and tiered team permissions are the most operationally critical controls because they prevent any single team member from moving funds unilaterally. Beyond multisig, look for configurable outflow thresholds, address blocklists, MFA enforcement, and third-party smart contract audits. B2BINPAY's Custody layers video-confirmed withdrawals and manual verification on top of standard multisig to address institutional risk requirements.

How do businesses automate fund collection and wallet sweeping across many deposit addresses?

Business-grade wallet infrastructure generates unique deposit addresses per customer automatically, then sweeps incoming funds into a consolidated treasury address based on configurable minimum thresholds and callback triggers. B2BINPAY's WaaS handles this through callback URL configuration and automatic fund consolidation, charging gas commission once per transaction rather than per individual sweep.

Why does on-chain auditability matter for payment processors and regulated crypto businesses?

On-chain transaction records are immutable and verifiable directly on the blockchain, which makes them a stronger audit foundation than off-chain ledgers maintained by third-party custodians. Embedding wallet infrastructure with real-time reporting, as B2BINPAY Custody offers, can reduce audit preparation time and strengthen positioning during compliance reviews.

Disclaimer: The service has legal and jurisdiction limitations. Please check T&Cs on https://b2binpay.com/en/risk-disclaimer

.svg)