For a CFO or head of payments, self-custody is not a personal-sovereignty argument. It is an infrastructure choice with a balance-sheet impact. Who controls the private keys to a business's crypto wallet determines counterparty risk, settlement timing, and the operational scope of treasury policy. Choose poorly and a custodial freeze can lock working capital for weeks. Choose without governance and a single lost key can do the same.

This guide reframes the self-custody conversation for businesses that already understand the basics. The focus is on key control as a treasury policy decision, the wallet architectures that scale for payment operations, and how regulated operators in forex, iGaming, and e-commerce can run non-custodial workflows without abandoning AML or KYT discipline.

Key Takeaways

- A self custody wallet gives a business direct on-chain signing authority, making key control a treasury governance decision rather than a personal security preference.

- Custodial payment processors can expose merchants to counterparty risk, including fund freezes, rolling reserves, and settlement delays outside the business's control.

- Multisig and MPC wallet architectures help organizations retain key ownership while removing the single-point-of-failure risk that raw self-custody introduces.

- Non-custodial payment infrastructure can support AML and KYT compliance requirements, making it viable for regulated operators in forex, iGaming, and e-commerce.

- Managed non-custodial infrastructure sits between raw self-custody and full third-party custody, letting businesses control keys while outsourcing integration and reconciliation complexity.

What Is a Self-Custody Wallet?

A self custody wallet is a signing system where the holder, not a third party, controls the private keys that authorize on-chain transactions. For a business, this distinction determines who can move funds, at what speed, and under what conditions. Key control is the prerequisite for every infrastructure decision that follows, from settlement workflows to compliance architecture.

Think of the private key the way a treasury function thinks about signatory rights on a corporate bank account. Whoever holds the credential can authorize movement; whoever does not must request it. On-chain finality removes the intermediating institution. There is no operations desk to call when access is restricted, and no contractual claim sitting between the organization and its funds.

For the alternative side of the spectrum, B2BINPAY's analysis of the role of crypto custodians walks through how third-party custody changes that authority model and what trade-offs it introduces for regulated operators.

Private Keys vs. Public Keys

A wallet's public key acts as an address. Counterparties send funds to it, and anyone can verify the balance and history on a public block explorer. The private key, by contrast, is the credential that signs outgoing transactions. It functions as a payment-system password with on-chain finality: any party holding it can authorize movement, and consensus only recognises the cryptographic proof, not the legal identity behind it.

For a business, the operational implication is direct. If the private key sits with a third-party processor, that processor controls fund movement. If the private key sits inside the organization, the organization carries both the responsibility and the authority to authorize every transfer.

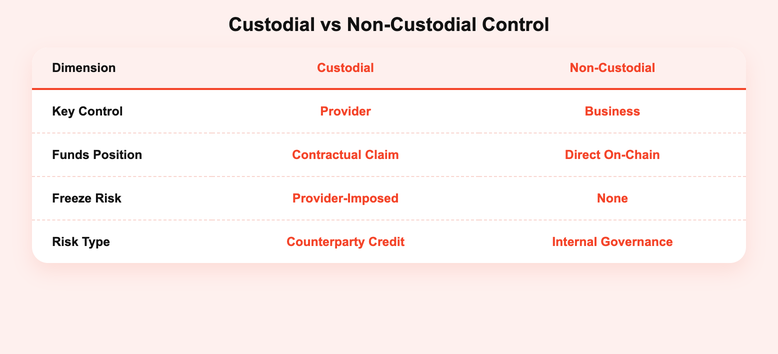

Custodial vs. Non-Custodial: Who Controls the Funds

A custodial wallet is an arrangement where the provider holds the private keys and the business holds a contractual claim on the underlying funds. Exchange accounts and many payment processor balances follow this model. The provider owes the business an amount, but the on-chain position is the provider's. If the provider freezes accounts, files for insolvency, or restricts access during a regulatory action, the business's recourse is contractual, not on-chain.

A non-custodial setup inverts that relationship. The business holds the signing credentials directly, often inside a wallet system the business operates or co-operates with a software provider. The provider may build the interface, the smart contract, or the API tooling, but they do not hold key material capable of unilaterally moving funds.

Why Key Control Is a Business Decision

For merchants, brokers, and platform operators, the choice between custodial and non-custodial infrastructure is not philosophical. It determines exposure to counterparty failure, reserve requirements, and settlement timing. Finance leaders should evaluate key control the same way they evaluate any other treasury policy: as a deliberate allocation of risk, not a default.

Self-custody is also not risk elimination. It is risk transformation. A custodial arrangement embeds counterparty credit risk inside the payments stack. A self-custody arrangement replaces that with technology risk, governance risk, and internal-control risk that the firm now manages directly. The right question is which set of risks the organization is better equipped to control.

High-risk merchant categories feel this trade-off most sharply. Forex brokers and iGaming operators routinely face stricter custodial conditions: rolling reserves, capped daily payouts, and discretionary account freezes during compliance reviews. Each of those is a counterparty constraint, not an on-chain limitation.

[[aa-cta]]

Evaluate B2BINPAY's regulated infrastructure

See how a CNAD PSAD-licensed and FSC VASP-licensed provider structures crypto payment workflows for forex, iGaming, and high-volume merchants.

[[/a]]

Counterparty Risk in Custodial Payment Flows

Counterparty risk in a custodial flow is straightforward. The provider's failure, freeze, or regulatory action can impair the business's access to its own funds, even when nothing has gone wrong inside the business.

Centralized exchange insolvencies and processor account holds over the past three years have left operators waiting months for fund release, often during peak working-capital periods.

The credit-risk concept that applies is expected exposure. In treasury terms, a custodial wallet decision is a counterparty-credit decision wearing a payments label.

The questions worth asking are the same ones a treasurer asks about any other credit exposure: who is the counterparty, what is their balance sheet, what is their regulatory standing, and what is the documented process when they act against the business's interest.

Key Ownership as a Treasury Policy Choice

Owning the keys means no third party can freeze a payout, impose a rolling reserve, or delay settlement by a banking day. That is not a philosophical benefit. It is a treasury policy choice with measurable effects on working-capital availability and intraday liquidity planning.

It also reframes how internal controls are written. With custodial accounts, controls focus on access to the provider portal. With non-custodial accounts, controls focus on the signing process itself: who initiates a transaction, who approves it, what threshold triggers additional review, and how recovery is structured if a signer becomes unavailable. The control language stays familiar to any audit committee already running a segregation-of-duties framework.

Wallet Types for Business Payment Infrastructure

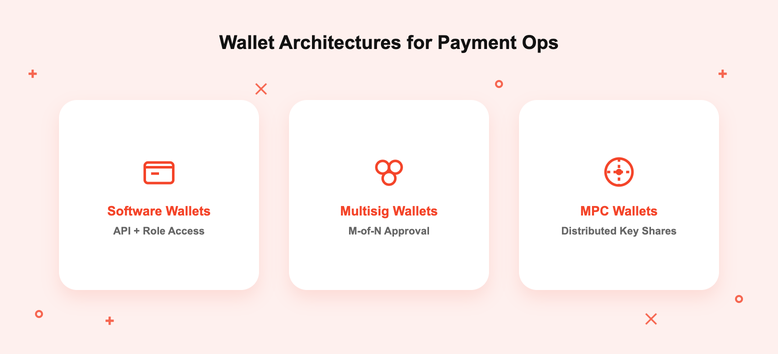

Not every wallet type is suitable for high-volume business payment operations. Hardware wallets and paper wallets serve individual holders, but they do not scale to the API-driven, multi-signer workflows that payment infrastructure demands. Businesses need wallet architectures that support programmatic access, organizational signing controls, and on-chain auditability at volume.

Hardware devices such as Ledger or Trezor remain useful for cold reserves, the long-dated treasury positions that do not need to move frequently. Paper wallets are essentially out of scope for any operational use case. The wallet types that matter for active payment infrastructure are software wallets with role-based API access, multisig contracts, and MPC architectures.

Software Wallets and API-Accessible Architectures

A software wallet in a business context is a programmatically accessible key store that integrates with payment APIs and supports automated transaction signing at volume. Consumer software wallets like MetaMask or Phantom illustrate the category but are designed for individual holders. Enterprise-grade software wallet infrastructure adds API key provisioning, role-based access, address whitelists, and audit logging, features that consumer wallets do not expose.

For payment operations, the relevant evaluation criteria are throughput, role separation, integration with reconciliation tooling, and the ability to enforce policy at the signing layer. A wallet that requires a human to approve every signature does not scale to thousands of daily deposits. A wallet that allows unrestricted programmatic signing without policy controls is an audit finding waiting to happen.

Multisig Wallets for Organizational Control

A multisig wallet requires multiple approvals before funds move on-chain. A typical organizational configuration uses an M-of-N policy: for example, two signatures out of three authorized key holders. The signature requirement is enforced at the protocol or smart contract level, which means no internal override and no single compromised employee or device can unilaterally drain a treasury.

Multisig maps cleanly onto existing segregation-of-duties frameworks. The treasury team initiates a transfer, an authorized approver signs, and a third key, often held by an executive or external auditor, provides the optional escalation path. Audit logs are visible on-chain, and any deviation from the policy is visible to anyone with the contract address.

MPC Wallets and Distributed Key Governance

Multi-party computation (MPC) wallets are the institutional evolution of multisig. Instead of producing multiple complete signatures on-chain, MPC distributes cryptographic key shares among the parties that need signing authority. The full private key is never reconstructed in any single location, and the resulting on-chain transaction looks like a standard single-signer transfer.

The operational advantages are meaningful for high-volume operators. MPC reduces gas costs because the on-chain footprint matches a standard transaction. It also removes the requirement to publish signer-set membership through on-chain multisig contracts, which can be relevant for privacy-sensitive operators. Fireblocks, Copper, and BitGo all offer MPC architectures aimed at regulated institutions.

How Non-Custodial Payment Workflows Operate

Non-custodial payment infrastructure changes how funds move from customer to merchant. Instead of routing through a custodial processor that holds balances on the merchant's behalf, transactions settle directly on-chain to addresses the business controls. Understanding the mechanics helps finance teams evaluate whether this model fits their settlement and reconciliation requirements.

In a typical workflow, the merchant provisions an address per customer or per invoice, the customer pays directly to that address, and the funds settle on-chain into a wallet structure the business owns. The processor's role narrows to address generation, monitoring, KYT screening, and reconciliation tooling. Settlement timing is governed by block confirmations, not by the processor's internal cycle.

On-Chain Invoicing and Address Generation

A unique deposit address per customer or per transaction is the operational backbone of a non-custodial workflow. The pattern eliminates address reuse, isolates each customer's fund flow on-chain, and creates a one-to-one map between invoice and settlement. Auto-consolidation of those addresses into a designated treasury wallet removes the manual overhead of tracking dozens or hundreds of incoming addresses.

For the reconciliation team, the result is a cleaner ledger. Each invoice has a matching on-chain transaction, identifiable by the deposit address that generated it, with a timestamp and confirmation count visible to anyone with read access to the blockchain.

[[aa-cta-blue]]

Test non-custodial flows in a fee-free sandbox

B2BINPAY offers a sandbox environment with no fees so finance and engineering teams can validate workflows before connecting to production.

[[/a]]

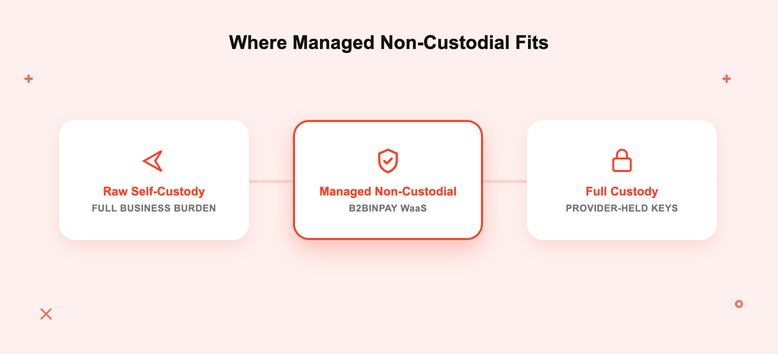

Managed Non-Custodial Infrastructure Explained

Between raw self-custody and full third-party custody sits a third model: managed non-custodial infrastructure. The business retains key ownership and on-chain control, while the provider handles operational complexity including API integration, smart contract auditing, monitoring, and reconciliation tooling.

For regulated payment operators, this is often the most relevant configuration. It preserves the counterparty-risk advantages of self-custody while removing the engineering burden of building a payment stack from scratch.

This category is structurally underserved in the current landscape. Consumer-focused content treats self-custody as binary: either the user holds the keys on a personal device, or a custodial provider holds them. The middle ground, where the merchant holds keys and a regulated provider supplies the infrastructure around them, is where most institutional crypto payment activity actually happens.

B2BINPAY's documentation on its crypto custody options walks through the full spectrum, from full-custody arrangements to non-custodial setups with managed support.

Where B2BINPAY Fits This Model

B2BINPAY operates as regulated crypto payment infrastructure. The company is licensed through B2BINPAY EL SALVADOR S.A. DE C.V. (CNAD PSAD and Central Reserve Bank PSB, supervised by the SSF) and B2BINPAY MAURITIUS LTD (FSC VASP licence GB24203002 under the Virtual Asset and Initial Token Offering Services Act 2021). The platform has processed $5.1 billion in incoming volume by 2025 across 6.7 million transactions and 983 business customers.

Within that regulated framework, B2BINPAY's Wallet-as-a-Service product is explicitly non-custodial: the merchant holds the private keys and retains complete control over the assets. The platform layers operational features on top, including multi-factor authentication, transaction signing controls, manual approval for outgoing transactions, address blocking, callback URLs, and cross-chain address duplication across ETH, Polygon, and Avalanche. KYT screening runs on every transaction, and the sandbox environment is fee-free.

For merchants that prefer the opposite end of the spectrum, B2BINPAY also offers a regulated custody service with dual-approval withdrawals, SumSub video verification, and 24/7 monitoring across 350+ supported currencies. The choice between the two models is exactly the treasury-policy decision this article is built around.

Compliance in a Non-Custodial Setup

Non-custodial architecture does not mean operating outside compliance requirements. Businesses in forex, iGaming, and e-commerce still need AML controls, transaction monitoring, and auditability regardless of who holds the keys. The right non-custodial infrastructure can satisfy these requirements without surrendering key ownership.

Regulators have made this position increasingly clear. The Financial Action Task Force (FATF) Recommendation 16, the Travel Rule, applies to virtual asset service providers regardless of whether the counterparty wallet is hosted or unhosted. The EU's Markets in Crypto-Assets Regulation (MiCA) draws similar boundaries: crypto-asset service providers carry compliance obligations whether the architecture is custodial or non-custodial. The control surface for compliance moves from the wallet itself to the screening and monitoring layers around it.

KYT Integration at the Transaction Level

Know Your Transaction (KYT) is transaction-level risk scoring applied to on-chain fund flows, distinct from the KYC identity verification that happens at onboarding. KYT screens deposits and withdrawals for exposure to sanctioned addresses, mixer services, darknet markets, and other risk categories, and flags transactions for review before they settle into treasury wallets.

KYT can be integrated into non-custodial payment flows without requiring the business to surrender key control. The provider supplies the screening engine and the policy-management layer; the merchant retains signing authority on the underlying wallet. B2BINPAY runs KYT screening on every transaction inside its regulated infrastructure, which means the screening layer travels with the merchant's settlement flow regardless of which wallet model the merchant chooses.

On-Chain Auditability for Regulatory Reporting

Every on-chain transaction is permanently recorded and publicly verifiable. For a regulated business, that creates a native audit trail that supports regulatory reporting without additional reconciliation overhead. Examiners can verify settlement records directly against a public block explorer, and internal audit can run independent checks without depending on the processor's database exports.

The contrast with custodial processor reporting is instructive. Custodial reports are sourced from the provider's internal records, which may be sufficient for routine reporting but cannot be independently verified by a regulator without the provider's cooperation. On-chain records do not have that dependency. They are verifiable by anyone with the wallet address, immediately and at no cost.

Operational Risks and How to Mitigate Them

Self-custody transfers operational risk from the custodian to the business. Key loss, access control failures, and internal fraud are now the business's responsibility to prevent rather than the provider's. The mitigation frameworks for each risk are well-established and map directly to existing enterprise security and treasury governance practices. Owning keys is not safer or riskier than custodial in the abstract; it shifts where the controls have to live.

For businesses that prefer to outsource these controls entirely, a regulated custody service handles them on the merchant's behalf. B2BINPAY's overview of its crypto custody service details how dual approvals, video-verified withdrawals, and 24/7 monitoring can substitute for an internal control framework that the merchant would otherwise need to build.

Key Loss and Business Continuity Planning

Irrecoverable key loss can freeze treasury operations permanently. On-chain consensus recognises cryptographic proof of ownership, not job titles, contracts, or legal agreements. If the keys are gone, the funds are gone in any practical sense.

Enterprise mitigation strategies are well-established. Sharded key backups distribute key material across geographically separated and physically secured locations. Hierarchical deterministic wallet structures allow derivation of subordinate keys from a parent seed under controlled conditions.

Smart contract accounts can embed on-chain recovery logic, including time-locked recovery paths and pre-authorised emergency signers. The common principle is that key material is protected separately from any data that could compromise it.

Access Control and Segregation of Duties

Aligning key-signing roles with the organisation's existing segregation-of-duties framework is the practical starting point. No single employee should hold sufficient key material to authorise high-value transfers unilaterally. Multisig thresholds enforce this policy at the protocol level. Internal-audit and finance committees should treat key-share assignment with the same rigour as treasury signatory authority on bank accounts.

API key governance deserves equal attention. Each integration that touches the wallet should have a separately provisioned key with the minimum permissions required, time-limited where possible, rotated on a regular schedule, and revocable at the policy layer. Operational hygiene at this level is what separates a controlled non-custodial setup from an audit finding.

Take the Next Step: Evaluate Your Infrastructure Policy

Whether self-custody fits the business depends on the trade-offs the finance team is best positioned to manage: counterparty exposure on one side, internal control and key governance on the other. Regulated managed non-custodial infrastructure narrows that decision by giving the merchant key ownership inside a compliance-first stack, with KYT screening, sandbox testing, and licensed operating entities behind the platform.

Open a B2BINPAY account to evaluate non-custodial WaaS, the regulated custody alternative, and the supporting compliance infrastructure against the requirements of a forex, iGaming, or high-volume merchant operation.

Frequently Asked Questions about Self Custody Wallet

What is a self-custody wallet in a business payment context?

A self-custody wallet is a signing system where the organization controls the private keys that authorize on-chain transactions, rather than delegating that authority to a third-party processor.

Key control determines who can move funds, at what speed, and under what conditions, which makes self-custody an infrastructure governance decision rather than a personal security preference. For merchants and brokers, it sits inside treasury policy alongside banking signatories, payment processor agreements, and counterparty-credit limits.

What is the difference between a self-custody wallet and a custodial wallet?

In a custodial arrangement, the payment processor or exchange holds the private keys, and the business holds a contractual claim on the funds rather than direct on-chain control. In a self-custody model, the organization retains the signing credentials, which means no third party can unilaterally freeze, re-route, or impose reserve requirements on settlement funds. The practical difference shows up most clearly when custodial providers restrict access during audits, insolvency events, or regulatory actions, situations where self-custody removes the third party as a point of failure.

How does a business use self-custody without relying on one employee or one device?

Multisig and MPC wallet architectures distribute signing authority across multiple key holders or devices, so no single person can authorize a high-value transfer unilaterally. A common configuration requires two or three approvals before funds move, which maps directly onto existing segregation-of-duties policies in finance operations. Managed non-custodial platforms layer audited smart contracts and policy controls on top, reducing the operational burden of building this governance layer in-house.

Can a self-custody payment setup still support AML and compliance requirements?

Yes. Non-custodial infrastructure can integrate KYT (Know Your Transaction) controls at the transaction level, screening on-chain fund flows for risk signals without requiring the business to surrender key ownership.

Every on-chain settlement also creates a permanent, publicly verifiable audit trail, which may support regulatory reporting more reliably than custodial processor records alone. Platforms designed for regulated operators in forex and iGaming layer AML controls directly into non-custodial payment workflows; B2BINPAY runs KYT screening on every transaction across its regulated infrastructure.

What happens if a business loses access to a self-custody wallet?

Without a tested recovery mechanism, key loss can freeze treasury operations permanently because on-chain consensus recognizes only cryptographic proof of ownership. Enterprise mitigation strategies include sharded key backups, hierarchical deterministic wallet structures, and on-chain recovery logic embedded in smart contract accounts. Protecting key material separately from encrypted data and restricting access through strict role-based controls are foundational practices for any business operating non-custodial payment infrastructure.

Disclaimer: The service has legal and jurisdiction limitations. Please check T&Cs on https://b2binpay.com/en/risk-disclaimer

.svg)