Converting crypto to fiat means selling digital assets through a regulated platform and withdrawing the proceeds to a bank account or card. The process sounds simple — and it is, in a single transaction. The complexity compounds when you're doing it at scale: multiple assets, recurring payments, KYC requirements across multiple jurisdictions, withdrawal fees that vary by rail, and reconciliation records that auditors expect to be clean and consistent.

This article is a practical walkthrough for CFOs, finance leads, and payment infrastructure teams who need to convert crypto to fiat as part of a business workflow, not a one-time transaction. It covers the three main conversion methods, a step-by-step wallet-to-bank workflow, compliance essentials, the real cost of off-ramping, and when API-driven auto-conversion is the right call.

Key Takeaways

- Converting crypto to fiat requires selecting a regulated platform, completing KYC/KYB verification, depositing crypto, executing a sell order, and withdrawing funds to a bank account or card. Each step carries distinct fee and timing implications.

- Payment gateway auto-conversion eliminates manual sell orders by instantly converting incoming crypto payments to fiat at the point of receipt, reducing volatility exposure to near zero.

- KYC and AML compliance are non-negotiable for fiat withdrawals on regulated platforms; businesses should prepare corporate documentation and banking details before initiating any off-ramp workflow.

- Total conversion costs include trading fees, network fees, withdrawal fees, and potential FX spreads. Comparing these across platforms prevents margin erosion on high-volume flows.

- API-driven gateways like B2BINPAY automate the entire crypto-to-fiat workflow, enabling businesses to accept 350+ cryptocurrencies while settling in USD or EUR without holding volatile assets.

What Crypto-to-Fiat Conversion Means for Your Business

Crypto-to-fiat conversion is the process of exchanging cryptocurrency holdings for government-issued currency that can be deposited into a bank account and used for normal business operations. The business case is straightforward: most suppliers, employees, and tax authorities require payment in fiat. Crypto holdings, whether from accepted payments or a balance sheet position, need to convert before they can fund those obligations.

The operational contrast matters. Holding unconverted cryptocurrency means carrying volatile digital assets on your books: the value can shift 3–5% in a day, the accounting treatment requires fair-value measurement, and reconciliation demands timestamps that manual workflows often fail to capture consistently. Converting to fiat at the point of receipt — or on a defined schedule — gives your treasury team stable balances, simplified accounting, and audit-ready records.

For a broader view of how crypto compares to fiat in business operations, including the trade-offs for treasury and compliance, see our related guide.

[[aa-cta]]

Fiat Settlement

Crypto In, Fiat Out — Same Day

Accept crypto payments from customers globally and receive USD or EUR in your bank account within hours. Automated conversion, SWIFT/SEPA payouts, and zero rolling reserve. B2BINPAY bridges blockchain and banking.

[[/a]]

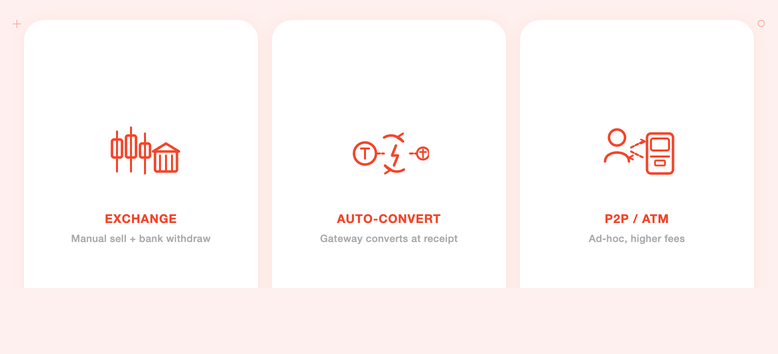

Main Methods to Convert Crypto to Fiat Compared

There are three realistic off-ramp paths for businesses. Each suits a different operational profile.

Exchange Sell and Bank Withdrawal

The traditional approach: deposit crypto to a centralized exchange, place a sell order, and withdraw fiat to a linked bank account. This method is well-understood, available globally, and gives you direct control over timing and price.

The operational trade-off is manual work. Every conversion requires a deposit, order placement, and withdrawal, each with its own processing time and fee. Large conversions carry slippage risk on market orders; limit orders require active monitoring. Bank wire withdrawals typically take 1 to 3 business days after a conversion executes.

This approach suits businesses with infrequent, larger conversions where timing flexibility matters. For example, converting a monthly treasury balance rather than converting each individual payment. It's less suited to high-volume recurring payment flows where manual intervention doesn't scale.

For detailed guidance on the bank withdrawal side of this flow, see our guide on how to transfer Bitcoin to a bank account.

Payment Gateway Auto-Conversion

Payment gateways with auto-conversion eliminate most of the manual steps. When a customer pays in crypto, the gateway converts it to fiat immediately at the point of receipt — before the asset can experience price movement — and credits the merchant's account in the target currency.

The operational benefit is significant: no manual sell orders, no volatility exposure, and no scattered wallet management. According to Microblink's 2025 gateway comparison, crypto payment gateway fees range from 0.23% to 1% per transaction — materially lower than card processing at 2.9% plus a per-transaction fee.

This method is ideal for merchants, brokers, and platforms accepting recurring crypto payments from customers. It also simplifies accounting because every transaction produces a fiat-denominated record at the moment of receipt, with timestamps and exchange rates documented automatically. B2BINPAY supports auto-conversion across 70+ tokens to USD or EUR, settling in under 24 hours. For context on how the on-ramp and off-ramp concepts differ, our explainer walks through the full ecosystem.

Peer-to-Peer and ATMs

P2P platforms match buyers and sellers directly, often with more flexible terms and fewer identity requirements. Bitcoin ATMs provide instant cash withdrawals at physical locations. Both methods are available and used — but neither is suited to business treasury operations at scale.

P2P introduces counterparty risk. You're relying on an individual's payment, and disputes or scams are the buyer's problem to resolve. ATMs charge 5–10% in fees and have per-transaction limits that make them impractical for amounts above a few hundred dollars. These methods fit individual or small, ad-hoc conversions better than recurring business treasury workflows.

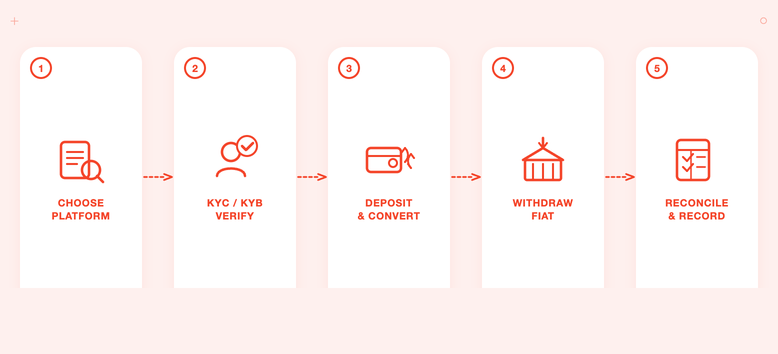

Step-by-Step Workflow to Move Funds From Wallet to Bank

Regardless of platform, the underlying workflow to convert crypto to fiat follows the same five steps. Here's the sequence and what to watch at each stage.

1. Choose a Regulated Off-Ramp Platform

Select a platform based on: regulatory status (VASP registration, MSB license, or equivalent), supported fiat currencies and withdrawal rails, trading fee structure, withdrawal fee schedule, and processing time.

Prioritize platforms with transparent, all-in fee schedules — trading fee, network fee, and withdrawal fee disclosed upfront. Hidden spreads add up quickly on high-volume flows. A platform charging a low trading fee but applying a wide conversion spread can cost more in practice than one with a higher headline fee and no spread.

Also check whether the platform can handle your asset range. A service that supports only BTC and ETH leaves you managing manual conversions for every other token you accept.

2. Verify Your Business and Banking Details

KYC/KYB verification is mandatory before fiat withdrawals on any compliant platform. For business accounts, typical documentation requirements include: company registration documents, proof of business address, director and beneficial owner identification, and linked bank account details.

Complete this verification before depositing any crypto. Deposits held pending verification create an operational bottleneck — your funds are on the platform but inaccessible until the review completes. Treat verification as a one-time setup cost that unlocks all future conversions without delay. Higher verification tiers typically unlock larger withdrawal limits and faster processing.

As regulated businesses accepting crypto payments, KYC/KYB compliance isn't just a platform requirement — it's part of your own AML obligations as a payment acceptor.

3. Deposit Crypto and Execute the Conversion Order

Send crypto from your wallet to the platform's deposit address. Before initiating the transfer, always confirm the deposit network — sending an ERC-20 token on the wrong network can result in permanently lost funds. Copy the deposit address from the platform directly; never rely on a saved or pasted address from an external source.

Once the deposit confirms, you have two order types to choose from. A market order executes immediately at the current price — best when immediate fiat access is the priority and the conversion amount is small enough that slippage is negligible. A limit order executes at a specific target price — useful for larger conversions where a few basis points matter, but requires active monitoring until the order fills.

Check the effective conversion rate before confirming. The displayed market price includes a spread; the actual rate applied to your order may differ. On larger conversions, this spread is material.

4. Withdraw Fiat via Your Preferred Rail

After conversion, initiate a fiat withdrawal to your linked bank account. Options vary by platform and region, but typically include: SEPA transfer (EUR, 1 business day within the EU), SWIFT wire (multi-currency, 1–3 business days internationally), ACH transfer (USD, 1–3 business days in the US), and card-linked withdrawal (near-instant, higher fees, lower limits).

Choose the rail based on timing and cost requirements. SEPA is typically fast and low-fee within Europe; SWIFT handles cross-border but carries correspondent bank fees. Card withdrawals are fastest for smaller amounts. Wire transfers suit larger amounts despite higher fees.

Confirm withdrawal fees upfront — these vary significantly across platforms and rails, and can erode a material share of proceeds on smaller conversions. For a complete guide to the cash-out process, including pro tips for minimizing withdrawal fees, see our detailed guide.

5. Reconcile and Record the Transaction

Every crypto-to-fiat conversion creates a taxable event in most jurisdictions and requires an accounting entry. Record the following for each conversion: cryptocurrency asset sold, quantity, conversion price (exchange rate at execution), fiat amount received, all fees paid, and the date and time of execution.

Most platforms provide exportable transaction reports — download these promptly after each conversion. Waiting until month-end to reconcile creates gaps if a platform limits historical export depth. Store records in a format your accounting system can import directly.

Note that crypto-to-fiat conversions may trigger capital gains tax obligations depending on your jurisdiction and how long you held the asset. Work with a qualified accountant to understand the specific treatment in your operating jurisdiction.

Compliance and KYC Essentials Before You Off-Ramp

Every regulated fiat off-ramp is required to verify user identity and monitor transactions for AML compliance. This isn't optional for platforms that want to maintain banking relationships and operate legally — and it protects businesses from unknowingly receiving or converting illicit funds.

KYC (Know Your Customer) verifies the identity of individual account holders. KYB (Know Your Business) verifies business entities — corporate structure, beneficial ownership, and source of funds. For corporate accounts, expect to provide all of the above.

Beyond account-level verification, KYT (Know Your Transaction) screening checks individual transactions for risk signals — links to sanctioned wallets, mixer services, or flagged counterparties. Well-implemented platforms run KYT automatically, so clean transactions process without delay.

Prepare your documentation before you open an account. Incomplete documentation submitted mid-process typically delays verification by days or weeks. Completing KYB upfront unlocks full platform functionality from your first transaction.

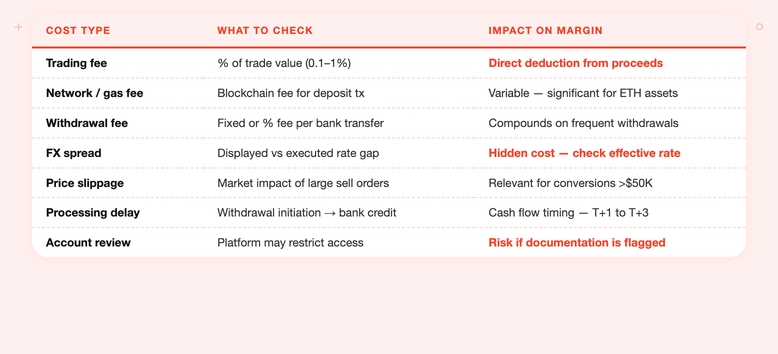

Costs, Security, and Operational Risks to Plan For

Understanding the total cost of converting crypto to fiat prevents margin surprises. Here's a breakdown of what to account for:

For security, enable two-factor authentication on every platform, use address whitelisting so funds can only withdraw to pre-approved accounts, and select platforms that have undergone third-party security audits. Never share API keys or account credentials across team members — use role-based access with the minimum permissions each role requires.

How an API-Driven Gateway Automates Crypto-to-Fiat Payouts

For businesses processing recurring crypto payments, the five-step manual workflow above describes the baseline — and a gateway with API-driven auto-conversion eliminates most of it.

The automated workflow: a customer initiates a payment in crypto. The gateway detects the incoming transaction on-chain, executes the conversion at the current rate, and credits the business's account in fiat. No manual deposit. No sell order. No withdrawal initiation. The entire flow from customer payment to fiat credit runs automatically.

The accounting benefit is equally significant. Every conversion produces a fiat-denominated record with an execution timestamp and exchange rate. Month-end reconciliation becomes a report download rather than a manual matching exercise.

B2BINPAY's off-ramp solution supports this workflow across 350+ cryptocurrencies, with auto-conversion to USD or EUR for 70+ tokens. The flat 0.25–0.40% processing fee covers conversion and settlement with no rolling reserve — 100% of converted proceeds are available immediately. API integration includes a full sandbox environment for testing before any real funds are involved. Settlement completes in under 24 hours.

According to Cobo's 2026 gateway overview, gateway-based payment processing handles invoice generation, payment confirmation, optional conversion, and settlement in a single integrated flow — which is what makes it the most operationally efficient path for high-volume recurring conversions.

Ready to Streamline Your Off-Ramp?

The core decision is simple: manage conversions manually through an exchange, or automate them through a payment gateway. For occasional large conversions, manual exchange workflows give you direct price control. For recurring business payments, auto-conversion eliminates the operational overhead and volatility exposure that come with manual conversion workflows.

B2BINPAY handles both paths. The exchange flow is supported for businesses managing balance sheet conversions. The API-driven auto-conversion path handles incoming customer payments — converting 70+ tokens to USD or EUR in under 20 seconds, settling in under 24 hours, with KYT screening built in and 0% rolling reserve.

If you're evaluating whether crypto payment acceptance makes sense for your business, start with our guide on accepting crypto payments as a business before configuring your off-ramp workflow.

[[aa-cta-blue]]

Convert Crypto to Fiat Automatically, at the Point of Receipt

B2BINPAY: 350+ currencies, 70+ auto-convert tokens, flat fee, 0% reserve. Sandbox available.

[[/a]]

Frequently Asked Questions about Converting Crypto to Fiat

Can you convert crypto to fiat?

Yes, businesses and individuals can convert cryptocurrency to fiat through centralized exchanges, payment gateways, P2P platforms, or crypto ATMs. Most fiat withdrawals require identity verification (KYC/KYB) on regulated platforms. The method you choose depends on your transaction size, speed requirements, and whether you need recurring conversions or one-time cash-outs.

How do I turn crypto into cash?

Send your crypto to a regulated exchange or payment platform, sell it for fiat, and withdraw the proceeds to your bank account or card. Timing ranges from near-instant for some card withdrawals to 1 to 3 business days for bank transfers. For businesses processing recurring crypto payments, automated gateways can convert and settle fiat without manual sell orders.

How fast can a business typically receive fiat funds?

It depends on the provider and withdrawal rail. Auto-conversion gateways may settle fiat within 24 hours; traditional exchange withdrawals typically take 1 to 3 business days. Card-linked payouts are usually fastest for smaller amounts. Processing speed also depends on your KYC verification tier and the destination bank's processing schedule.

Can I auto-convert every incoming payment to a single fiat currency?

Yes. Payment gateways with auto-conversion settle incoming payments from multiple crypto assets automatically in a single fiat currency like USD or EUR. This eliminates wallet sprawl, removes the need for manual conversion orders, and locks in fiat value at the moment of receipt — eliminating volatility exposure entirely.

.svg)