Adopting web3 payments is not a research project anymore. It is an operational decision with real trade-offs: who holds the private keys, which chains you support, how invoices reconcile, and what happens to your balance sheet when the market moves 8% overnight.

Forex brokers, iGaming operators, and cross-border merchants are past the "what is Web3" stage. They are choosing between custodial and self-custody infrastructure, configuring multi-chain wallets, and deciding whether to hold crypto or settle every transaction straight to fiat.

This guide skips the primer. It walks through the concrete decisions involved in adopting web3 payments: custody models, on-chain invoicing mechanics, wallet architecture, provider evaluation criteria, and a five-step implementation roadmap for businesses ready to go live.

Key Takeaways

- Adopting web3 payments starts with choosing between custodial and self-custody infrastructure before configuring assets, chains, or settlement workflows.

- On-chain invoicing ties payment confirmation directly to immutable blockchain records, which can automate reconciliation and cut manual finance overhead.

- Businesses can accept crypto and settle in fiat within 24 hours, removing balance sheet exposure to price swings.

- Web3 payment rails can bypass correspondent banking dependencies, cutting settlement delays for Forex brokers and global merchants.

- Built-in AML and KYT compliance tooling is a non-negotiable evaluation criterion for regulated businesses in iGaming and financial services.

Why Web3 Payment Infrastructure Is Ready

Web3 payment infrastructure is enterprise-ready because licensed providers now combine regulated custody, real-time compliance screening, and instant fiat settlement, capabilities that did not exist at this scale two years ago.

The Bank for International Settlements' 2026 Annual Economic Report put total stablecoin market capitalization at around $320 billion as of end-May 2026, and used that scale to argue for integrating tokenization into the regulated financial system rather than treating it as a fringe experiment, even while flagging where stablecoins still fall short of central bank money on singleness and interoperability.

That recognition, paired with regulated providers now offering licensed custody, compliance tooling, and instant fiat settlement, means the infrastructure question has shifted from "is this viable" to "which model fits my business."

Core Components of Web3 Payment Infrastructure

A working web3 payment stack has four moving parts, and skipping any one of them creates gaps that surface after launch, not before.

Blockchain

The blockchain is the settlement layer: a distributed ledger that records every transaction immutably and removes the need for a central clearing intermediary. Ethereum, Polygon, and Avalanche each offer different trade-offs between transaction cost, confirmation speed, and smart contract maturity, and the chain you support directly affects your customers' fees and wait times.

Smart Contracts

Smart contracts are programs deployed on a blockchain that run exactly as written and automatically enforce their own rules once conditions are met. Ethereum's developer documentation describes them as code and data residing at a specific address, executing without a third party able to alter the outcome.

For payments, that means an invoice, an escrow release, or a payout can trigger without manual approval once the contract's conditions are satisfied.

Digital Wallets

Digital wallets store the cryptographic keys that control access to funds on-chain. The distinction that matters for a live business is not the wallet interface but who controls the keys behind it, which is exactly the custody question the next section addresses.

AML and KYT Compliance

Anti-money laundering and Know Your Transaction (KYT) tooling screen incoming and outgoing transfers against risk databases before funds settle. For Forex brokers and iGaming operators operating under regulatory obligations, this is not an add-on. It is the component that determines whether a payment provider is usable at all.

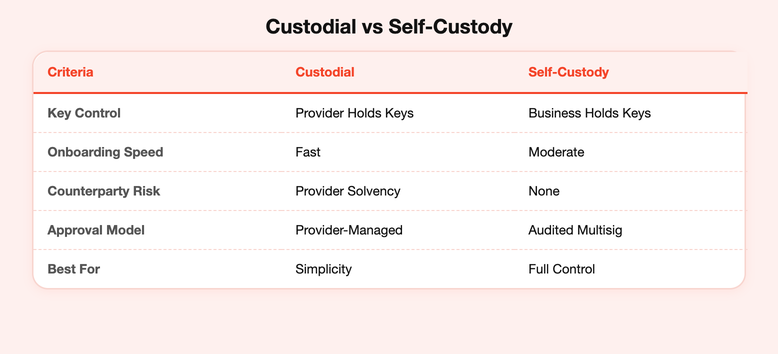

Custodial vs. Self-Custody Payment Models

Before touching chains, assets, or integration, a business adopting web3 payments has to answer one question: who holds the keys? That question sits at the center of the shift from Web2 to Web3 payment infrastructure, and it shapes everything downstream, from onboarding speed to counterparty risk exposure.

How Custodial Payment Processing Works

In a custodial model, the provider acts as custodian, holding merchant funds between receipt and payout in much the same way as crypto custodians work for institutional asset storage.

That arrangement simplifies onboarding because the business does not manage private keys directly, but it introduces counterparty and solvency risk: settlement now depends on the provider's solvency and internal controls, not just the blockchain's finality.

How Self-Custody Infrastructure Works

Self-custody flips that arrangement. The business retains its own private keys and controls funds at all times, typically through audited multisig smart contracts that require multiple approvals before any transfer executes.

That control comes with a real tradeoff: if a business loses access to its own keys or misconfigures its multisig setup, there is no third-party support desk to recover the funds, so self-custody demands internal key-management discipline that a custodial model does not.

B2BINPAY's DeFi App is built around this model: businesses keep custody of their own assets while still getting on-chain invoicing and payment infrastructure, rather than handing funds to a third party between receipt and settlement.

Choosing the Right Model for Your Business

There is no universal answer here. Run the decision through four questions: What are your compliance obligations? Does your team have the internal capacity to manage keys securely? How fast do you need settlement to happen? And how much counterparty risk is your finance team willing to carry?

A high-volume iGaming operator with a compliance mandate might prioritize custodial simplicity with strong built-in KYT. A crypto-native merchant that wants full control over funds might prefer self-custody instead. Match the model to your operational reality, not to whichever option launched first.

How On-Chain Invoicing Works

On-chain invoicing replaces the traditional invoice-and-wait cycle with a smart contract interaction. Here is the sequence: an invoice is generated as a smart contract call rather than a PDF, the payer sends funds to a deterministic address tied to that invoice, and the transaction is recorded immutably on the blockchain the moment it confirms.

Once that confirmation lands, a finance team can reconcile the payment automatically, without waiting on a bank confirmation email or manually matching a wire against a spreadsheet. This mechanism draws directly on the same programmable logic behind Ethereum smart contracts, applied specifically to payment reconciliation rather than general-purpose code execution.

For a CFO running monthly close on hundreds of transactions, that is the difference between a two-day reconciliation task and one that runs itself.

[[aa-cta]]

See Your Fiat Settlement Options

Check how B2BINPAY converts 350+ cryptocurrencies to EUR or USD automatically.

[[/a]]

Volatility Management and Fiat Settlement

The most reliable way to manage crypto volatility is instant auto-conversion to fiat, which removes price risk before it ever reaches the balance sheet. Holding crypto on the balance sheet is the biggest objection finance teams raise about web3 payments, and it is a fair one: price swings of 5-10% in a day are not unusual.

Customers paying in crypto do not need a bank account to complete the transaction, but your business still receives standard fiat currency in its own bank account once auto-conversion completes, typically within 24 hours.

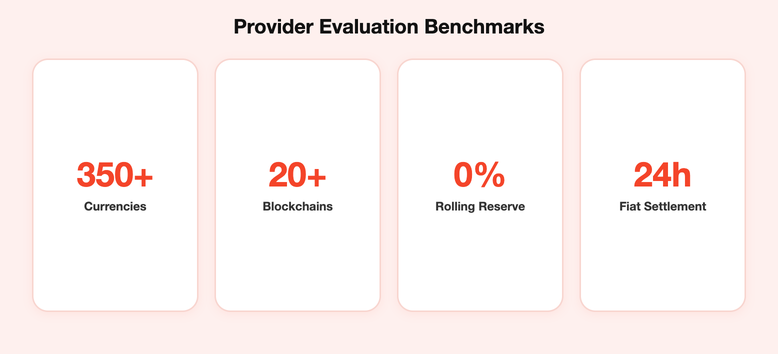

B2BINPAY's Merchant Wallet auto-converts 70+ tokens to USD or EUR via SEPA or SWIFT, charges a flat 0.25-0.40% processing fee, and carries a 0% rolling reserve. Compare that to providers using spread-based pricing or holding a percentage of merchant funds in reserve for weeks at a time, and the difference in cash flow predictability becomes the real evaluation criterion, not the headline processing fee.

Web3 Payment Benefits for Business Operators

The core benefits of web3 payments for business operators are chargeback elimination, lower reconciliation overhead, and faster cross-border settlement, but each one only matters if it maps to a problem you actually have.

For e-commerce merchants, that problem is chargebacks: crypto transactions settle on-chain and cannot be reversed by a cardholder dispute, which removes an entire category of fraud loss.

For iGaming operators, it is reconciliation overhead: manual matching of thousands of small transactions against player accounts consumes finance headcount that automated on-chain settlement eliminates.

For Forex brokers, it is cross-border friction, which is significant enough to warrant its own explanation below.

Cross-Border Payments Without Correspondent Banks

Traditional cross-border transfers route through a chain of correspondent banks, each adding a fee and a delay. Web3 payment rails bypass that chain entirely: funds move directly between wallets on a shared ledger, with no intermediary bank in the loop.

For a Forex broker serving clients in markets where card processing is restricted, expensive, or simply unavailable, this is not a marginal improvement. It is often the difference between being able to serve a market and not.

Which Businesses Benefit Most

Three verticals see the clearest return from adopting web3 payments. Forex and CFD brokers use multi-chain support and instant fiat settlement to serve clients in regions where correspondent banking is slow or unreliable. iGaming operators, particularly licensed ones with strict compliance obligations, rely on built-in KYT to screen deposits and withdrawals without building a compliance stack from scratch.

E-commerce merchants with cross-border customer bases use crypto payment rails to accept payment from markets where card networks charge high cross-border fees or decline transactions outright. In each case, the value is not "crypto is innovative." It is a specific friction point that web3 infrastructure resolves.

How to Evaluate a Web3 Payment Provider

Choosing a provider is where most businesses adopting web3 payments either save themselves months of integration pain or create it. Run every candidate through the same checklist: supported chains and assets, custody model, fee structure transparency, settlement speed, built-in compliance tooling, API documentation quality, and licensing status.

Treat this as a benchmark, not a shopping list to satisfy minimally. A provider that clears six of seven criteria but fails on licensing status is not a viable option for a regulated business, regardless of how attractive its fees look.

Supported Chains, Assets, and Settlement Options

Verify chain count, asset count, stablecoin support, and whether fiat off-ramp is built in or requires a separate third-party integration. B2BINPAY supports 350+ currencies across 20+ blockchains, which is a useful benchmark for what multi-chain coverage should look like at this stage of the market. A provider limited to two or three chains will force you back into this evaluation within a year as customer demand shifts.

Built-In Compliance Tooling and Licensing Status

AML and KYT compliance in practice means transaction screening, risk scoring, and Travel Rule readiness, not a checkbox on a sales page.

As of August 2025, only 11 jurisdictions had finalized comprehensive regulatory frameworks for cryptoasset activities, with supervision and enforcement lagging further behind, and that gap makes building a compliance layer independently increasingly expensive as rules catch up.

A provider with a regulated VASP license and compliance tooling built into the payment flow, rather than bolted on afterward, removes that cost from your roadmap entirely.

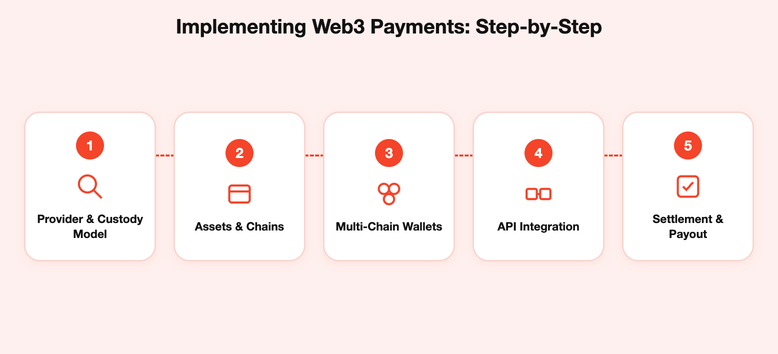

Implementing Web3 Payments: Step-by-Step

Once you have chosen a provider, the implementation sequence matters. Reordering these steps is one of the most common sources of integration debt after launch.

Step 1: Select Your Provider and Custody Model

Confirm your custody model first, using the evaluation criteria above, before verifying chain coverage or compliance tooling. This decision constrains everything that follows, so make it deliberately rather than defaulting to whichever provider your developer found first.

Step 2: Configure Supported Assets and Chains

Build an asset whitelist and select which chains you will support at launch. Chain selection is not a cosmetic choice: it affects gas fee management, settlement speed, and how complex your reconciliation process becomes as transaction volume grows. Start narrower than you think you need and expand once you have operational data.

Step 3: Set Up Multi-Chain Wallet Architecture

This is where most integration debt actually originates. You need unique receiving address generation per customer, auto-sweeping to consolidate funds into a central wallet, and a gas fee plan for each chain you support.

B2BINPAY automates address generation and fund consolidation, which removes a substantial amount of manual wallet management from the finance team's plate.

Step 4: Integrate the Payment API

Before touching production traffic, test integration quality in a sandbox environment and confirm you understand what connecting a crypto payment API involves end-to-end.

API documentation quality is itself an evaluation criterion, not just an engineering detail. Poor documentation here means longer integration timelines and more support tickets once you go live, so review the docs before you commit to a provider, not after.

Step 5: Configure Settlement and Payout Workflows

Set your auto-conversion preferences, payout thresholds, and reserve model. This is the step where your volatility management decision from earlier in the process actually gets implemented: if you want zero balance sheet exposure to crypto, this is where you configure automatic conversion to fiat on receipt, not an afterthought bolted on later.

Start Accepting Crypto on Your Terms With B2BINPAY

Adopting web3 payments comes down to five decisions: custody model, asset and chain configuration, wallet architecture, API integration, and settlement workflow. Get the sequence right and the rest of the implementation follows without surprises. Get it wrong and you are rebuilding parts of your payment stack within a year.

B2BINPAY is a regulated crypto payment infrastructure provider, not a generic gateway. It combines licensed custody and self-custody options, built-in AML and KYT compliance, 350+ supported cryptocurrencies across 20+ blockchains, and instant fiat settlement with a 0% rolling reserve.

Forex brokers, iGaming operators, and high-volume merchants use it to accept crypto without taking on volatility risk, manual compliance overhead, or banking relationships that freeze accounts without warning.

Whether your business needs custodial simplicity or full self-custody control, the infrastructure decisions covered in this guide determine how well your payment stack holds up once transaction volume grows.

Once that infrastructure is live, the same on-chain logic extends to the broader Web3 toolchain your customers already use, from wallets to browsers.

[[aa-cta-blue]]

Ready to Accept Crypto Payments?

Set up your account and start accepting 350+ cryptocurrencies with automatic fiat settlement.

[[/a]]

Frequently Asked Questions about Web3 Payments

Should a business use self-custody or a custodial provider for crypto payments?

The right model depends on your counterparty risk tolerance and internal key management capacity. Custodial providers simplify onboarding but introduce settlement dependency on the provider's solvency and operational controls.

Self-custody infrastructure, such as B2BINPAY's DeFi App with audited multisig smart contracts, gives your business full control over funds at all times.

How does on-chain invoicing work for business payments?

On-chain invoicing ties a payment request to a smart contract interaction, routing funds to a deterministic address recorded immutably on the blockchain. Once the transaction confirms, your finance team can reconcile it automatically without relying on third-party confirmation emails or manual matching against bank statements. This can significantly reduce back-office overhead for high-volume operators.

How do businesses manage payments across multiple blockchains and wallets?

Multi-chain wallet architecture requires unique receiving address generation per customer, auto-sweeping to consolidate funds, and chain-specific gas fee planning. Platforms like B2BINPAY support 350+ currencies across 20+ blockchains with built-in auto-consolidation, which reduces the reconciliation complexity of operating across multiple networks. Skipping this architecture planning is one of the most common sources of integration debt post-launch.

What compliance checks are required when accepting crypto payments?

Regulated businesses accepting crypto payments typically need AML screening and KYT (Know Your Transaction) monitoring to assess the risk profile of incoming and outgoing funds. Jurisdictions globally are developing formal supervisory frameworks for cryptoasset activities, which means building this compliance layer independently has become increasingly costly and complex.

Selecting a provider with built-in KYT and licensed VASP status, such as B2BINPAY holds in El Salvador, addresses this requirement without separate compliance tooling.

How do you adopt web3 payments for your business step by step?

Start by selecting your provider and confirming the custody model, then configure your supported assets, chains, and multi-chain wallet architecture before integrating the payment API.

After sandbox testing, configure your settlement and payout workflows, including auto-conversion to fiat if you want to eliminate balance sheet exposure to crypto volatility. Each step builds on the previous one, and reordering them typically creates costly integration issues after launch.

Disclaimer: The service has legal and jurisdiction limitations. Please check T&Cs on https://b2binpay.com/en/risk-disclaimer

.svg)