In the current era of global connectivity, it is vital to engage in business operations across different countries. It allows for simple money transfers between individuals and businesses, no matter where they may be situated.

SWIFT has been the key player in supporting these transactions for many years. The emergence of blockchain tech is transforming the landscape of international payments and rapidly establishing itself as a strong rival to SWIFT's dominance in this area.

As these systems progress, a vibrant competition between established practices and fresh ideas is impacting the future of global payment systems.

[[aa-cta]]

Payment API

REST API for Crypto Payment Processing

Accept, convert, and settle crypto payments through a single REST API. B2BINPAY supports custom callbacks, real-time transaction webhooks, and a full sandbox environment for rapid integration.

[[/a]]

This article explores the strengths and weaknesses of blockchain vs. SWIFT, comparing their impact on todays global financial system.

What is SWIFT?

SWIFT, the Society for Worldwide Interbank Financial Telecommunication, was established in 1973 and revolutionized cross-border financial transactions by replacing the older and error-prone TELEX system TELEX system.

Today, it serves over 11,000 financial institutions in more than 200 countries, handling around 45 million messages per day. This network doesnt physically transfer funds but facilitates communication between banks, allowing them to send and receive payment instructions using standardized codes.

Each transaction is transmitted through SWIFT using unique Bank Identifier Codes (BIC), which ensure that money reaches its intended destination. Monetary institutions rely on SWIFTs robust infrastructure to process trillions of dollars in daily transactions.

As global payment demands evolve, SWIFT has introduced innovations like the Global Payments Innovation (GPI) to improve speed and transparency. Yet, it faces increasing competition from emerging blockchain-based payment platforms, which offer faster, cheaper, and more transparent alternatives for cross-border transactions.

How SWIFT Payment Works

At its core, SWIFT facilitates payments between banks by transmitting finance messages, known as SWIFT codes, that instruct where and how funds should be transferred.

These messages allow banks to initiate and confirm transactions securely, relying on standardized codes for efficient global operations.

Each participating institution is assigned a unique SWIFT code, which identifies the institution during transactions, ensuring the correct funds transfer.

SWIFT transfers transmit payment orders between institutions using a standardized messaging system. Each bank in the transfer chain must have a corresponding relationship, either directly or through intermediary banks.

When a transaction is initiated, a payment order is sent through the SWIFT network, passing through various correspondent banks until it reaches the final destination. This method is efficient for global transfers but comes with inherent delays, as multiple intermediaries are often involved.

While SWIFT payment offers reliable and secure messaging, it does not physically transfer money. Instead, it facilitates communication between institutions, requiring intermediary banks to settle transactions.

Advantages and Limitations of SWIFT

The SWIFT network has long been the standard for cross-border and domestic payments, offering several distinct advantages. Its global reach is unmatched, connecting thousands of finance institutions across more than 200 countries. This extensive network provides a secure and reliable platform for banks to communicate, ensuring that international transactions are processed efficiently and in compliance with global regulatory standards.

SWIFTs well-established infrastructure also supports high-value transactions with confidence, offering encryption and authentication protocols that maintain the confidentiality and security of payment information.

Despite these strengths, SWIFTs cross-border payments face some significant limitations. One of the primary drawbacks is speed. Transactions often take several days to settle, especially when multiple intermediary or correspondent banks are involved, causing delays that can disrupt business operations. The complexity of the payment chain also increases costs, with high fees often incurred due to the involvement of intermediary banks.

Another limitation is transparency. While this traditional financial messaging service provides secure messaging, it lacks real-time transaction tracking, which has become a priority in todays fast-paced economic landscape.

Additionally, its reliance on a centralized network leaves it vulnerable to global political decisions, as seen when certain countries or institutions are restricted from using SWIFT services due to international sanctions. As competition grows from blockchain-based alternatives, SWIFT is under increasing pressure to innovate.

What is Blockchain?

Blockchain is a decentralized digital ledger that revolutionizes how transactions are recorded and verified. Unlike traditional systems, which rely on intermediaries like banks, blockchain operates through a distributed network of nodes, making it more secure and transparent.

Each transaction is grouped into a "block" and linked to a previous one, creating an unalterable "chain" of records. This process eliminates the need for third-party verification, significantly speeding up transaction times and reducing costs.

Originally developed for cryptocurrencies like Bitcoin, blockchain technology is now being used in cross-border payments, where it offers several key advantages over systems like SWIFT.

By removing the need for intermediaries, blockchain enables faster, more cost-efficient international payments, making it a disruptive force in the financial industry and an attractive alternative for businesses seeking streamlined global transactions.

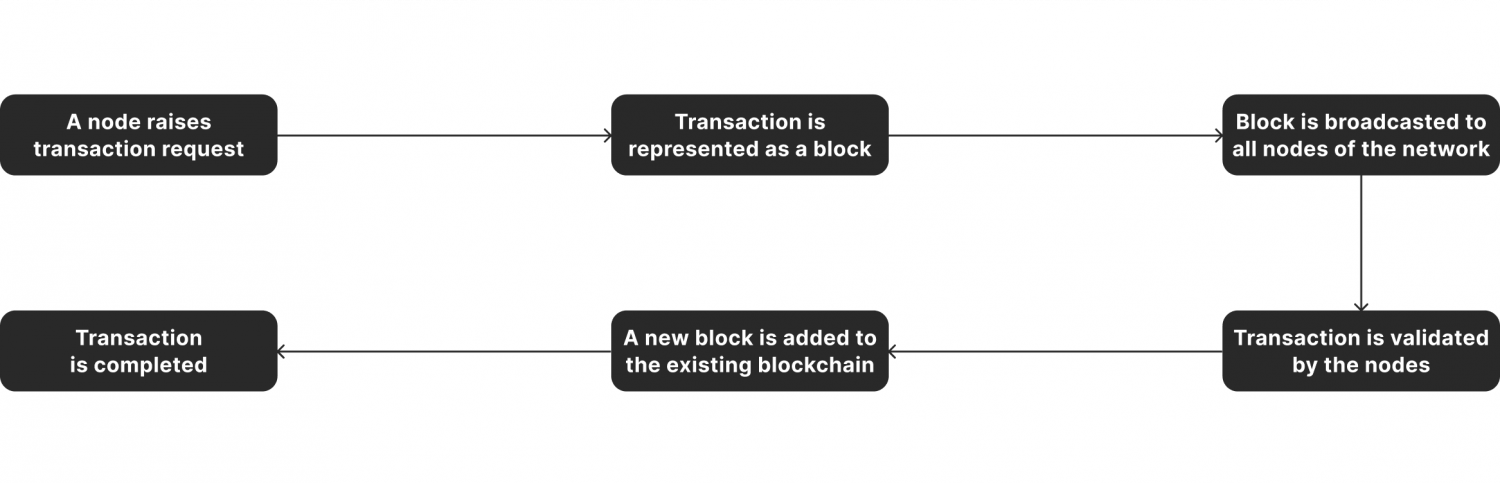

How Blockchain Payments Work

In blockchain-based payments, users can send cryptocurrency or digital assets directly to recipients without intermediaries. Once a payment is initiated, nodes in the blockchain network validate the transaction.

After validation, it is added to a block, which is then appended to the blockchain. This process is completed within minutes or seconds, depending on the blockchain used.

Advantages and Challenges of Blockchain Payments

Blockchain payment solutions offer significant advantages in the world of cross-border transactions. One of the key benefits is speed. Unlike traditional systems like SWIFT, which can take days to process payments, blockchain transactions are often settled in real time or within minutes. This fast settlement drastically reduces delays, making it ideal for businesses and consumers needing quick transfers.

Cost efficiency is another major advantage. Blockchain eliminates intermediaries, reducing transaction fees significantly compared to traditional banking networks. Moreover, its transparencyevery transaction is recorded on an immutable ledgerprovides enhanced security and traceability, reducing the risk of fraud.

However, the blockchain payment system faces some challenges. Regulatory uncertainty remains a concern, as different countries have varying crypto money and blockchain tech rules. The volatility of certain cryptocurrencies also poses risks, although stablecoins have helped address this issue.

Lastly, blockchain still faces scalability issues, especially when transaction volumes surge, which can slow down the network and increase costs. Despite these challenges, blockchain continues to disrupt the financial industry with its innovative payment solutions.

Comparing Blockchain vs. SWIFT for Cross-Border Payments

In cross-border payments, SWIFT and blockchain offer distinct advantages and challenges. Let's compare the two systems and gain insights into how each shapes todays global payment landscape.

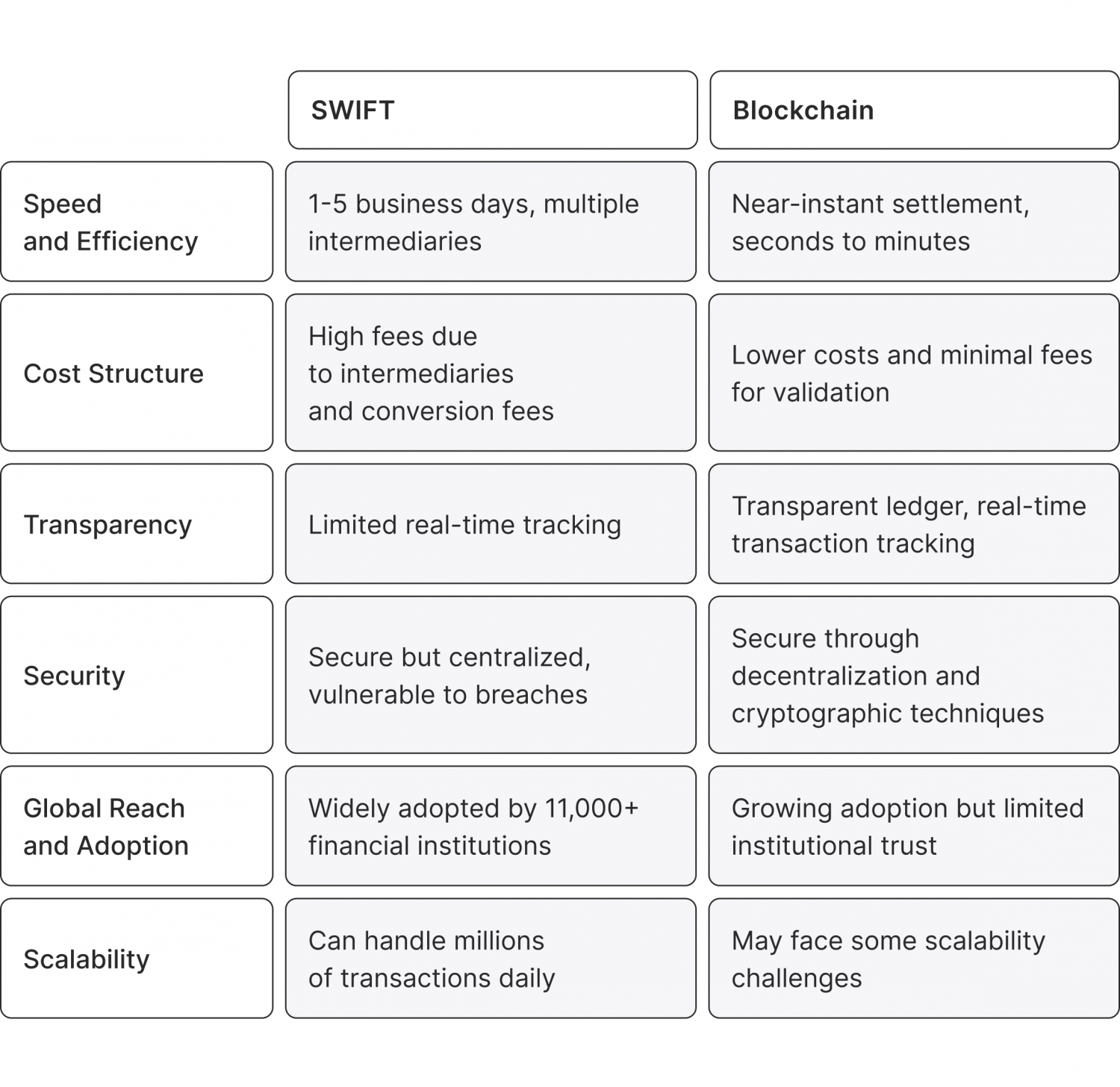

Speed and Efficiency

[[aa-note]]

API-first payment infrastructure allows businesses to embed crypto acceptance directly into existing checkout flows, back-office systems, or custom trading platforms without redirecting users to third-party pages.

[[/a]]

SWIFTs biggest disadvantage compared to blockchain is speed. SWIFT transactions can take anywhere from one to five business days to settle, depending on the number of intermediaries involved. On the other hand, payment processing using blockchain offers near-instantaneous settlement, with most transactions completed in a matter of seconds to minutes.

Cost Structure

SWIFT transactions incur significant fees, especially when multiple intermediary banks are involved. These fees can include transaction fees, currency conversion fees, and charges from intermediary banks.

Blockchain transactions, by contrast, are generally much cheaper. Blockchain eliminates the need for intermediaries, reducing costs significantly, though minor fees for network validation (e.g., gas fees) still apply.

Transparency and Security

SWIFT transactions offer limited transparency, as users cannot easily track a payments progress in real time. In contrast, blockchain provides a transparent ledger, allowing participants to verify and track the status of payments instantly.

Security is another area where blockchain excels, thanks to its decentralized nature and use of cryptographic techniques. While SWIFT is secure, its centralized structure makes it vulnerable to potential breaches.

Global Reach and Adoption

SWIFT payment system boasts a global network of over 11,000 financial establishments, making it the most widely used system for cross-border payments. Blockchain, while growing in adoption, still lacks the same level of institutional trust and regulatory integration. However, blockchains global, decentralized nature makes it well-suited to expand into regions lacking traditional banking infrastructure.

Scalability

SWIFT's established infrastructure can handle millions of transactions daily. Distributed ledger technology, while scalable, has encountered bottlenecks when transaction volumes surge, leading to slower processing times and higher fees. Innovations such as layer-2 solutions and sharding are helping to address these issues, but blockchain has yet to match SWIFTs capacity fully.

Examples of Crypto Winning Over SWIFT

Blockchain tech rapidly redefines cross-border payments, challenging traditional systems like SWIFT with faster, more cost-effective solutions. One standout example is Ripple, whose blockchain-based payment protocol leverages its native cryptocurrency, XRP, to facilitate real-time, low-cost international transactions.

Unlike SWIFT, Ripple bypasses multiple intermediary banks, streamlining the payment process and significantly reducing both time and fees. This efficiency has attracted numerous financial institutions looking for a modern alternative to SWIFTs slower, more expensive transfers.

Another major player in this space is Stellar, whose blockchain network, in collaboration with the IBM World Wire platform, is connecting institutions across the globe. Using Stellars native token, Lumens (XLM), the platform enables seamless cross-border payments, offering both speed and transparency that SWIFTs system currently lacks. Stellars approach reduces reliance on correspondent banking, a core component of SWIFT, which often introduces delays and additional costs.

JPMorgan's Interbank Information Network (IIN) takes a slightly different approach, focusing on enhancing efficiency in correspondent banking by using a shared ledger system. This blockchain-based solution helps banks exchange payment information more quickly and securely, cutting down on manual processes and expediting international transfers.

Platforms like Corda Settler, built on the Corda blockchain, are also making waves by offering seamless cross-border settlements through multiple payment rails. This flexibility bypasses SWIFT's limitations, reducing intermediary costs while maintaining high levels of security.

Finally, stablecoins such as Tether (USDT) and USD Coin (USDC), built on blockchains like ETH, are gaining popularity. These digital currencies offer the stability of traditional fiat currencies combined with the technological advantages of blockchain, making them ideal for secure, low-cost cross-border transactions.

Together, these examples highlight the increasing dominance of crypto over SWIFT in revolutionizing global payments.

Blockchain vs SWIFT: Use Cases and Current Implementations

The growing demand for faster, more efficient cross-border payments has driven both blockchain and SWIFT to innovate. While SWIFT remains the backbone of traditional banking, blockchain is making significant strides with decentralized solutions.

Lets explore how both systems are being utilized in real-world scenarios, and highlight key use cases and the latest implementations that are reshaping the global payments landscape for businesses and economic institutions.

SWIFTs Innovations

Despite its limitations, SWIFT continues to innovate. Its Global Payments Innovation (GPI) service aims to provide faster, more transparent international payments by allowing banks to track the status of payments in real time. SWIFT is also exploring partnerships and integrating with new technologies like blockchain to streamline payment processes.

Blockchain-Based Solutions

Blockchain platforms like Ripple, Stellar, and ETH are changing cross-border payments. Ripples XRP-based system has gained traction with several major financial institutions, offering near-instant transfers at a fraction of the cost. Stellar, similarly, enables low-cost payments using XLM. Stablecoins and Central Bank Digital Currencies (CBDCs) are also gaining popularity as secure, blockchain-based alternatives for cross-border payments.

The Future of Cross-Border Payments

The future of cross-border payments is likely to be shaped by a combination of traditional banking systems like SWIFT and innovative technologies like blockchain. While SWIFT remains dominant due to its extensive network and regulatory trust, blockchains speed, cost-efficiency, and transparency make it a strong contender for the future.

Hybrid systems may emerge, combining the best of both worldsSWIFTs global reach and regulatory integration with blockchains speed and efficiency.

Moreover, innovations like CBDCs and stablecoins could bridge the gap between traditional and decentralized systems, providing the security and trust of government-backed currencies while leveraging the technological advantages of blockchain.

Conclusion

Both SWIFT and blockchain have their unique strengths in shaping todays cross-border payments.

SWIFTs global network, security, and regulatory integration make it a reliable choice for international transfers, but its slower processing times and higher costs are increasingly seen as drawbacks.

Blockchain, meanwhile, offers a fast, transparent, and low-cost alternative, though its adoption is still limited by regulatory uncertainty and scalability challenges.

[[aa-cta-grey]]

Compliance Suite

FATF Travel Rule via Notabene

B2BINPAY's integration with Notabene automates originator and beneficiary data exchange across VASPs, keeping you compliant with Travel Rule requirements in all applicable jurisdictions.

[[/a]]

As the financial landscape continues to evolve, the two systems will likely coexist, with each playing a crucial role in different aspects of the global payments ecosystem.

Blockchains innovation and SWIFTs established infrastructure ensure that international payments will continue to improve, benefiting institutional investors and individuals alike in an increasingly interconnected world.

.svg)