The cryptocurrency sector has grown exponentially over the past few years and is now one of the most talked-about topics in finance. With the potential to revolutionise the global financial system, its future impact on banking cannot be underestimated from blurring the boundaries between decentralised networks and centralised institutions to democratising access to financial services. What is the ultimate trajectory for crypto? In this blog post, we delve into predictions for how crypto could shape up in the banking industry around both developed and emerging markets.

Current State of Crypto in Banking

Currently, crypto is still in its early stages of adoption within the banking industry. Most banks hesitate to invest heavily in cryptocurrencies due to their limited regulatory framework and volatile nature. This hesitation is most prominent in developed markets, while some banks in emerging markets have been more eager to explore the technology.

[[aa-cta]]

Crypto Payment Gateway

Enterprise Crypto Payments, Built for Scale

B2BINPAY connects your business to 350+ cryptocurrencies with automated fiat conversion, bank-grade security, and full API access. Regulated, reliable, and ready to deploy in under 24 hours.

[[/a]]

The recent news of bank collapses has also caused concern amongst banking regulators, who have yet to develop an appropriate regulatory framework. The collapse of Silvergate Bank, a crypto-friendly financial institution, sent ripples throughout financial institutions. Some people are worried and making pessimistic predictions because of the problems faced by Silicon Valley Bank, which suffered losses due to its investment in low-interest instruments that devalued rapidly, and Signature Bank, which had been investigated multiple times in the past. The fact that these banks entered the cryptocurrency market and faced even more scrutiny only added to people's concerns.

However, there has been a growing acceptance of its use as an asset class for hedging against risk or diversifying portfolios. Some financial institutions have even begun offering services related to crypto transactions, custody and payments using blockchain technology. This activity has become more commonplace in developed markets such as the US and Europe than in emerging markets such as Africa and Asia.

Major Challenges and Limitations Facing Crypto Adoption in Banking

The adoption of crypto in the banking sector is still facing major challenges. The lack of an adequate regulatory framework, legal uncertainties, and difficulties related to Know Your Customer and Anti-Money Laundering requirements have been some of the main hindrances that have held back its mainstream adoption.

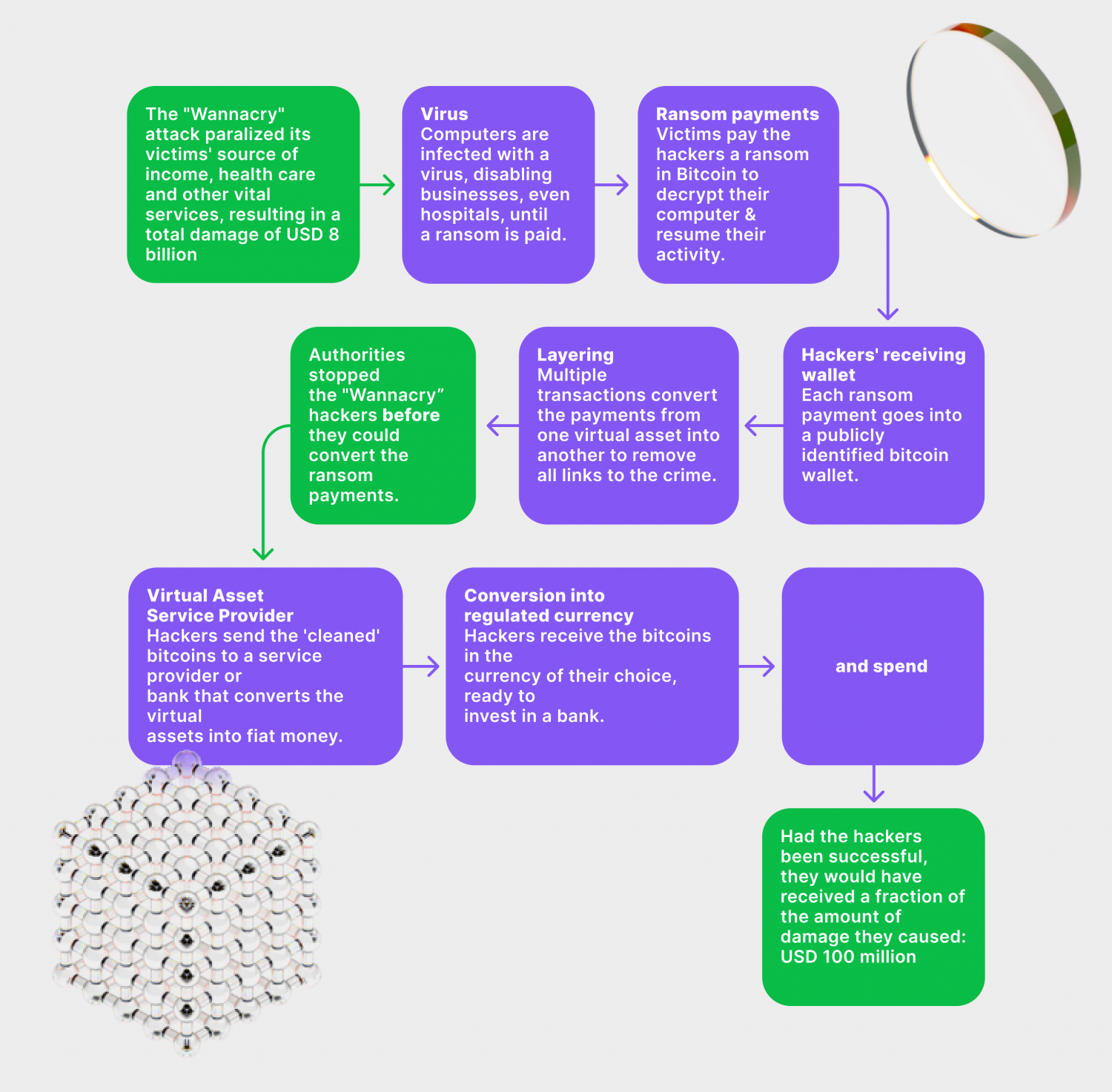

Furthermore, security is also seen as a major risk factor for other institutions investing in cryptocurrency assets. As more value gets locked into digital tokens, the potential damages caused by hacker attacks, such as the recent QuadrigaCX scandal where over $200 million was lost due to the death of its founder grows.

The increasing value of cryptocurrencies also heightens the risk of money laundering and other illegal activities. Most banks have implemented stringent KYC/AML protocols to reduce the chances of criminal and illegal activity and fight off money launderers. Still, these measures may not be enough in decentralised and anonymous spaces like blockchain networks.

Consumer protection is another concern, as there are few legal safeguards for users unaware of their rights or don't understand how to use cryptocurrency services properly. Numerous examples exist of people being scammed by sending money to an unknown person and never seeing those funds again.

Impact of Crypto on Traditional Banking Services and Business Models

However, despite the risks and bad experiences, cryptocurrency has the potential to profoundly change how banking services are delivered in both developed and emerging financial markets. In terms of payment services, it could reduce settlement times and increase transparency and security through distributed ledgers. This could drive down costs for users as well as financial institutions.

At the same time, it could lead to a shift towards digital banking models and open access to financial services for those excluded from traditional banking systems due to a lack of resources or identity documents.

Moreover, crypto can be used to improve existing banking products such as loans by providing more reliable data points on which lenders can base their decisions creating higher quality loan portfolios at lower risk levels. It can also enable banks to issue digital tokens backed by assets on the blockchain, allowing them to offer services like peer-to-peer lending or payment streams.

In terms of business models, it could enable banks to move away from transactional banking and towards more asset management services ultimately creating new sources of revenue which could be used to offset declines in other areas.

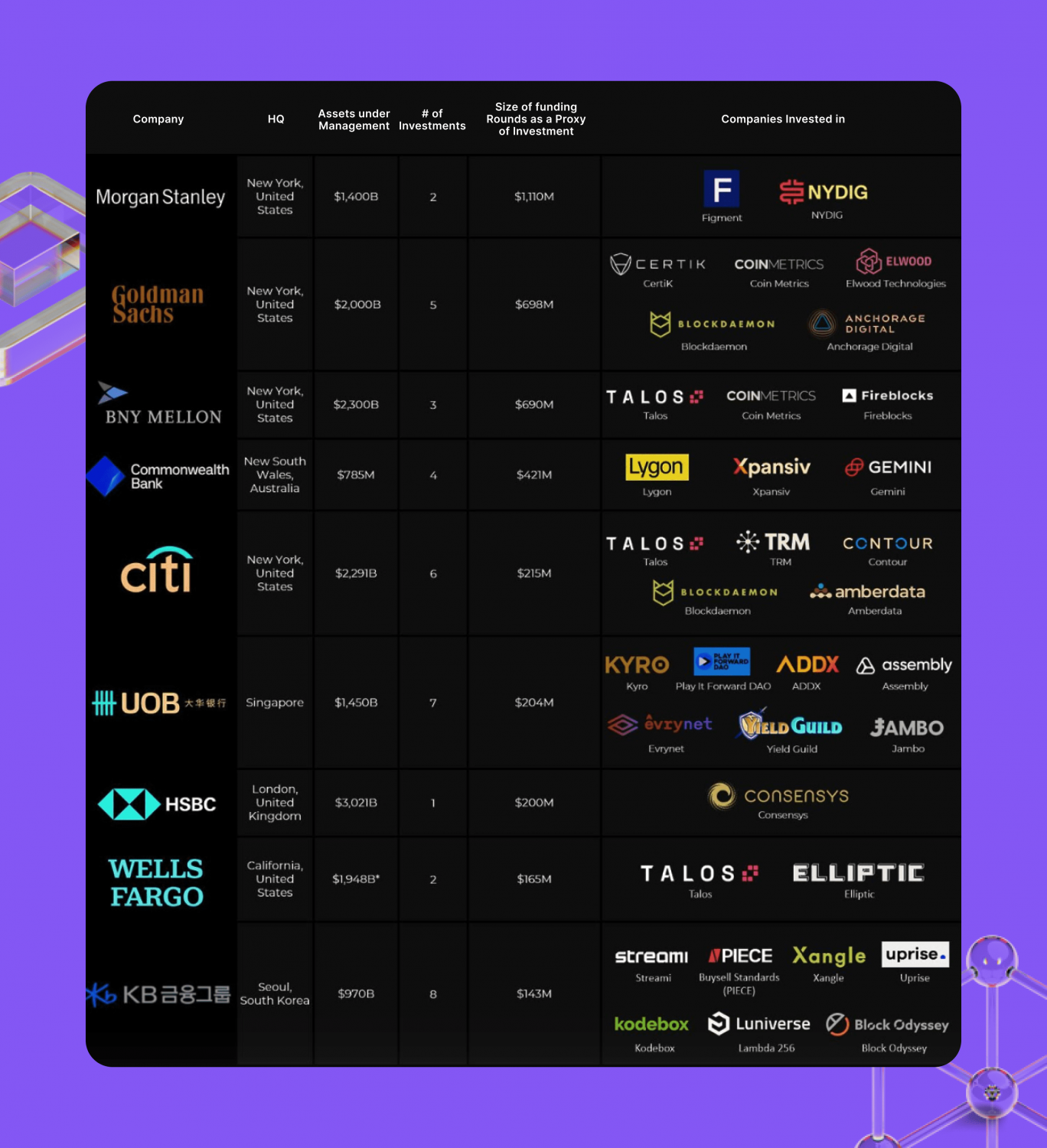

In fact, several institutions have already "seen the light" and have integrated crypto into their banking services.

Case Studies of Successful Crypto Adoption in Banking

Goldman Sachs

Several banks have already started to integrate cryptocurrency into their banking services. In 2021, Goldman Sachs launched its first cryptocurrency trading desk. Goldman Sachs, led by CEO David Solomon, aims to expand its market presence by accepting crypto trading institutions on a selective basis to broaden its offerings. In addition, the company has unveiled a new software platform that delivers real-time cryptocurrency prices and news to its customers.

BBVA

More recently, BBVA became the first global bank to offer crypto asset custody services in Spain. The Spanish-based financial institution provides end-to-end management of digital assets such as tokens and stablecoins for crypto investors who want to use these products as part of their portfolios.

UBS

UBS, the world's largest private bank, recently launched its blockchain platform to provide asset management services. UBS AG has introduced a digital bond that is publicly traded and settled on both blockchain-based and traditional exchanges, making it the first of its kind in the world. This bond allows investors to easily invest in a digital bond, regardless of whether they have blockchain infrastructure or not. This move by UBS aims to remove obstacles to implementing innovative technology that can simplify and expedite bond issuance.

The UK Government

The UK is implementing various measures to encourage the use of blockchain technology and crypto assets in the country. It aims to create a favourable regulatory landscape to attract investments. The UK wants to establish a regulatory sandbox to test distributed ledger technology projects, which regulators will oversee. Sandboxes are secure test environments in which companies can execute new projects with minimal risk to consumers.

Other Institutions

At the same time, crypto-focused startups also make headway into traditional finance by partnering with banks and other financial service providers. Ripple Labs has already struck deals with major Japanese and South Korean banks, which allow them to send money internationally with greater ease and speed than traditional systems can provide.

Overall, the use of cryptocurrency in banking is becoming increasingly mainstream as banks recognise its potential benefits and move towards embracing it more fully. This could revolutionise banking operations, reduce costs and open access to financial services for those excluded from traditional banking systems due to a lack of resources or identity documents.

Future Trends of Digital Assets in the Banking Sector

The banking sector is rapidly adapting to cryptocurrency and blockchain technology, with more banks integrating these technologies into their services. This trend will likely continue in the future as the advantages of using crypto assets become increasingly evident. As such, it is important to understand the potential future trends that could shape the banking sector.

[[aa-note]]

Regulated crypto payment providers must maintain compliance across multiple layers: AML screening, Travel Rule data sharing, sanctions list monitoring, and local licensing — a set of requirements that take years to build independently.

[[/a]]

Increased Adoption of Cryptocurrency by Banks

As cryptocurrency is becoming more accepted worldwide, banks are beginning to recognise the potential advantages of using digital currencies as a medium of exchange. This could result in banks offering services such as custodial accounts for customers who wish to hold digital assets.

An increase in the use of distributed ledger technology (DLT) is another potential trend that could shape the future of banking. DLT can be used to create tamper-proof records and facilitate faster global payments through smart contracts. This would enable banks to process transactions quickly while reducing costs associated with manual reconciliations. Furthermore, it could lead to faster and more secure cross-border payments, eliminating the need for costly intermediaries.

Even though crypto assets like Bitcoin are not commonly used in regular banking, their expansion can impact banks. While many banks have refrained from dealing with crypto assets, a few have looked into implementing a decentralised ledger to enhance their offerings. One instance is the European Investment Bank, which has leveraged DLT to generate digital bonds.

The Basel Committee on Banking Supervision (BCBS), one of several European authorities, has established regulations to safeguard banks against the possible risks associated with crypto assets. The rules classify crypto-assets into two categories - Group 1 (lower risk) and Group 2 (higher risk). Tokenised traditional assets and stablecoins with robust stabilising mechanisms fall under Group 1, while crypto-assets such as Bitcoin and unstable stablecoins fall under Group 2. Stricter rules and limits apply to banks holding Group 2 crypto-assets. Such rules and regulations are a welcome step and will help create an even playing field in banking.

All this points to a future where cryptocurrency and blockchain tech will become increasingly integrated into the banking sector. As such, the future of banking looks set to be shaped by the growth of cryptocurrency and blockchain technology.

Integration of Blockchain Technology in Financial Institutions

Blockchain technology promises to revolutionise the banking and finance industry. Blockchain-based solutions offer banks new ways of conducting transactions, increasing transparency and reducing costs.

Integrating blockchain technology into existing banking systems could result in faster payments, improved digital identity verification processes, and lower customer transaction fees. It could also help reduce fraud by ensuring that transaction data stored on the blockchain is immutable and tamper-proof. In 2016, a poll indicated that 90% of payment industry professionals in the EU anticipate that blockchain technology will impact payments by 2025.

Blockchain integration will simplify clearance and settlement systems for banks, even for the biggest banks in the world. Currently, there are numerous difficulties when transporting money, even for a basic bank money transfer, which must pass through multiple intermediaries or a trusted third party and adhere to regulatory requirements before it can be delivered. More often than anyone would like, the bank transfer fails, causing the customer to incur additional costs.

Incorporating blockchain technology in banking systems would make it easier for banks to execute transactions quickly, securely, and cost-effectively. Banks could also use smart contracts to automate many of their processes and reduce paperwork. Smart contracts are self-executing agreements that can be programmed to execute tasks based on predetermined conditions automatically. This would eliminate the need for manual intervention and speed up financial transactions.

Experts suggest blockchain technology can simplify compliance procedures and enhance bookkeeping processes for accounting and auditing purposes. The technology also acts as a virtual notary to validate each transaction. By adding data to a single book instead of maintaining separate transaction receipts, businesses can create decentralised and accessible records that are safer.

Development of Central Bank Digital Currencies (CBDCs)

Central Bank Digital Currencies (CBDCs) are digital versions of traditional fiat currencies issued by the government's central bank. CBDCs differ from cryptocurrencies because they are backed by the government rather than completely decentralised.

CBDCs have several potential benefits for financial institutions, including providing faster and more secure payments, reducing costs associated with traditional banking systems, and increasing financial inclusion. In addition, CBDCs could give central banks better control over monetary policy and give them more insight into economic activity.

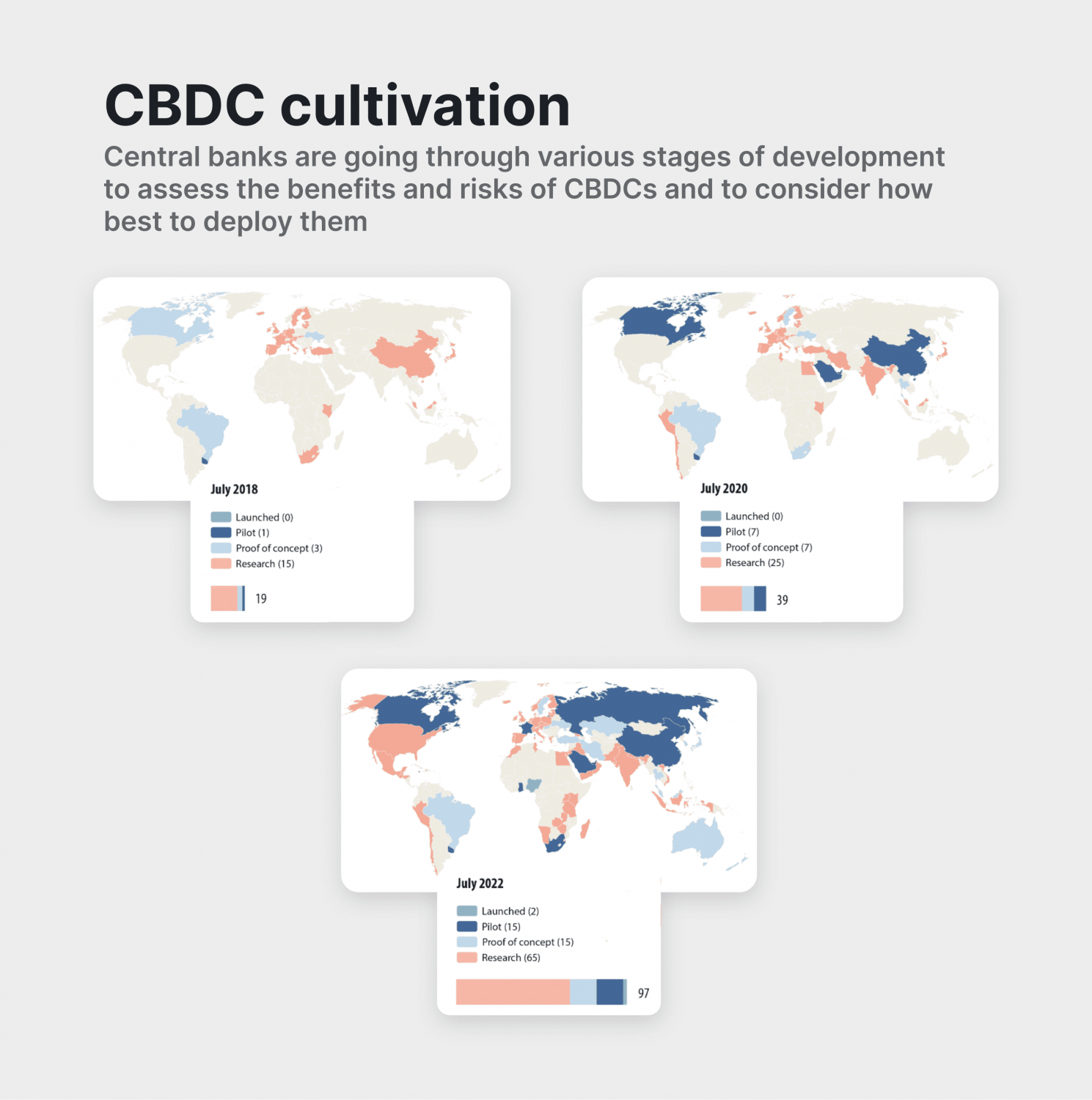

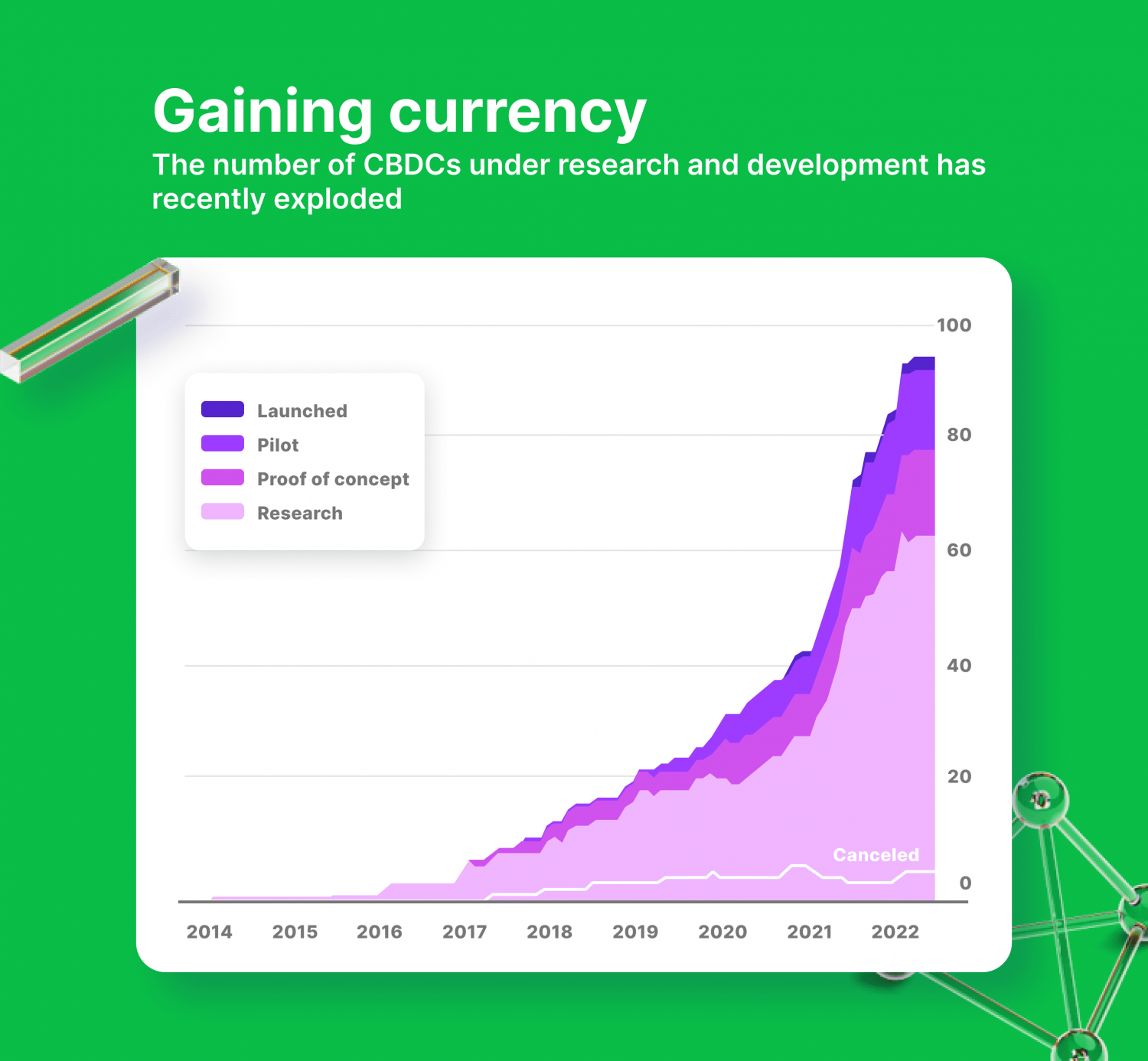

While the development of CBDCs is still in its early stages, many central banks and their countries are already exploring the possibilities. As of July 2022, there were nearly 100 CBDCs in research or development stages and two fully launched: the eNaira in Nigeria, unveiled in October 2021, and the Bahamian sand dollar, which made its debut in October 2020.

Countries are exploring alternative payment systems that bypass the US dollar due to financial sanctions on Russia. The number of cross-border wholesale CBDC tests has increased to 9, while the number of cross-border retail projects has risen to 7. This represents almost twice as many projects as there were in 2021. In 2023, more than 20 countries, including Australia, Thailand, Brazil, India, South Korea, and Russia, will be undertaking significant measures to test and develop a Central Bank Digital Currency. Some countries will continue their pilot programs, while others will begin new test phases. Additionally, the European Central Bank (ECB) is expected to initiate a pilot program next year.

Expansion of Use Cases for DeFi and Traditional Finance

Slowly, different financial institutions began to adopt cryptocurrency as a viable asset for their customers. Many banks have started offering crypto storage and trading services, while others use blockchain technology in their business processes. Banks are also exploring the potential of DeFi, an ecosystem of financial applications built on blockchain networks.

Cryptocurrencies and DeFi need to adopt some financial regulations to become more stable. According to journalist Michael Casey, incorporating DeFi and crypto into traditional finance can aid in tackling the energy crisis and addressing climate change. By utilising renewable sources such as wind, solar, and geothermal energy and decentralising energy sources, we can improve funding for climate action and enhance energy reliability.

Crypto technology can facilitate the creation of distinct tokens that symbolise renewable energy. These tokens can then be utilised as security for DeFi loans, enticing more investment in eco-friendly initiatives. Although Bitcoin mining necessitates significant energy usage, it can be used for renewable sources rather than non-renewable ones. This, in turn, can stimulate the expansion of decentralised energy production and renewable energy projects.

The Emergence of New Business Models in The Banking Industry

The fintech industry is rapidly expanding and disrupting traditional banking models. Banks are developing new strategies to keep up with the changing technology landscape, such as launching digital banks or entering into partnerships with fintech firms. Banks also leverage blockchain technology to increase efficiency and reduce transaction costs.

Several banks began offering services such as asset tokenisation, blockchain-based payments and transfers, digital wallets, and other fintech solutions. Banks are also exploring the potential of artificial intelligence (AI) to improve their customer experience, risk management systems, trading models, and fraud detection capabilities.

Banks began entering into strategic partnerships with fintech firms to incorporate their services into existing banking infrastructure. By working with fintech startups, banks can create innovative products and services that make them more competitive.

This trend of collaboration between banks and fintech firms will grow in the coming years as more companies recognise the potential of these partnerships. Banks will likely embrace digital banking capabilities further and adopt agile development models to keep up with changing customer needs.

Conclusion

[[aa-cta-grey]]

Merchant Wallet

Flat-Fee Crypto Payments That Scale

B2BINPAY charges a flat 0.25–0.40% per transaction regardless of volume. No percentage markups, no monthly fees, no withdrawal charges. The more you process, the more you save compared to card rails.

[[/a]]

The global financial system is undergoing considerable transformation due to the emergence of new technologies such as cryptocurrency, decentralised finance, and artificial intelligence. Banks are leveraging these technologies to improve their operations, offer better services to customers, and create distinct business models. Additionally, banks are forming strategic partnerships with fintech firms to incorporate their solutions into existing banking infrastructure.

The banking sector is poised to witness a new future, a period of rapid growth and development in the coming years as banks continue to embrace digital technologies, although it won't happen overnight. The increasing use of blockchain, cryptocurrency, DeFi, AI, and other emerging technologies will create more opportunities for banks to explore new models and remain competitive in an ever-evolving industry.

.svg)