If you run payments or treasury for a merchant, broker, or exchange, RWA tokenization for DeFi is no longer a research topic you can park for next year. It's already inside your payment stack. The stablecoins your customers pay with are tokenized real-world assets, and so are the on-chain T-bill funds your competitors use to earn yield on idle balances. The question has shifted from "what is this trend?" to "which of these instruments do we accept, hold, and settle in?"

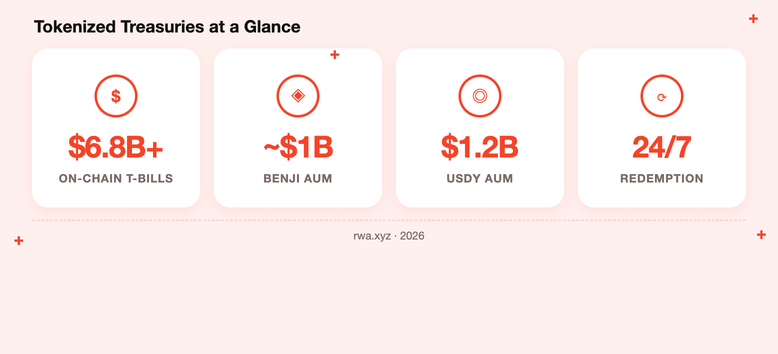

The numbers explain the urgency. Stablecoins now hold roughly $295 billion in circulation according to rwa.xyz data from mid-2026, while tokenized US Treasury products have climbed past $6.8 billion. That's not speculative volume. It's settlement money and working capital moving on-chain.

This article skips the retail investing angle entirely. We'll cover what RWAs are, why stablecoin dominance forces an acceptance decision, how tokenized treasuries work as cash management tools, and the compliance obligations attached to both.

Key Takeaways

- Stablecoins are the dominant layer of RWA tokenization for DeFi, which makes USDT and USDC the most operationally relevant assets for merchants evaluating crypto payment acceptance.

- Tokenized treasury products, such as on-chain T-bills, can serve as yield-bearing cash alternatives for businesses managing idle on-chain balances outside traditional banking infrastructure.

- Choosing between stablecoins for settlement means weighing liquidity depth, jurisdictional regulatory status, and counterparty risk, not just payer preference or market familiarity.

- Stablecoin transactions carry specific KYT obligations, including sanctions screening at the transaction level, which is distinct from one-time KYC onboarding.

- Smart contract vulnerabilities and custody risk in tokenized assets create operational exposure that businesses should evaluate before integrating RWA infrastructure into payment or treasury workflows.

What Are RWAs in DeFi?

Real-world assets in DeFi are off-chain instruments, including fiat currencies, government bonds, and private credit, represented on-chain as tokens. This category matters to business operators for one simple reason: stablecoins, the most widely accepted crypto payment assets, are themselves RWAs. How an asset is tokenized determines its settlement properties, its compliance obligations, and its liquidity, and all three affect your payment infrastructure choices.

Defining RWAs for Business Operators

An RWA is a blockchain token that represents a claim on something that exists off-chain. A dollar in a reserve account. A short-dated Treasury bill. A slice of a private credit pool. The token moves on-chain; the underlying value sits with an issuer or custodian legally responsible for backing it.

For operators, the most familiar RWA is the stablecoin in your settlement wallet. Every USDT or USDC balance is a tokenized claim on reserves held by Tether or Circle. From there, the category extends to tokenized bonds and private credit, which matter increasingly to treasury teams rather than traders.

What Tokenization Actually Does On-Chain

Tokenization wraps an off-chain claim in a smart contract so it can be held, transferred, and settled like any other crypto token. The contract enforces the rules: who can hold the token, how it transfers, and how redemptions process. Once issued, the token settles peer-to-peer with no card network or correspondent bank in the middle.

Most RWA tokens are issued on a small set of standards. ERC-20 and TRC-20 dominate stablecoin issuance, so your wallet infrastructure should support both before you commit to an acceptance strategy. Network choice affects fees, confirmation speed, and which customers can actually pay you.

From Investment Trend to Settlement Rail

Tokenized assets stopped being an investment story the moment businesses started using them to move money. Stablecoins now function as a settlement rail: a merchant in Dubai can receive USDC from a customer in Brazil in minutes, at any hour, without a correspondent bank chain taking days and fees along the way.

The European Central Bank has noted that stablecoin adoption is increasingly linked to cross-border payments rather than crypto trading, with US dollar stablecoins accounting for around 99% of the global stablecoin market (ECB, 2025). When regulators frame an asset class as a payment instrument, operators should treat it as one.

How Tokenized Assets Create On-Chain Finality

Settlement finality is the property that matters most for payment operations: once a tokenized transfer confirms on-chain, it's done. There's no chargeback window, no pending ACH reversal, no bank batch cycle. Programmability adds automated sweeps and conversions on top, and every transfer is auditable on a public ledger.

Compare that with correspondent banking, where a payment can sit in limbo across time zones and intermediaries; we've broken down that contrast in our comparison of blockchain settlement versus SWIFT. For a CFO, the takeaway is cash flow certainty: finality tells you exactly when funds are yours to deploy.

[[aa-cta]]

Accept Stablecoins Without Building Compliance From Scratch

B2BINPAY's Merchant Wallet screens every incoming USDT and USDC payment with built-in KYT, then settles to fiat when you want it.

[[/a]]

Types of RWAs Businesses Should Know

Not all RWA categories carry the same operational weight for merchants and brokers. Stablecoins dominate market activity and directly shape which assets you should accept. Tokenized bonds and treasury securities come next, increasingly used for corporate cash management rather than speculation. Real estate, commodities, and art tokens are growing but rarely touch payment or treasury workflows today.

Stablecoins as the Dominant RWA Layer

Stablecoins are the largest RWA category by a wide margin, with roughly $295 billion in circulating value as of mid-2026 (rwa.xyz). USD-pegged tokens make up nearly all of it. Tether's USDT remains the global liquidity leader, while Circle's USDC has become the preferred asset in regulated markets.

The operational conclusion is hard to argue with: if you're building crypto payment acceptance, USDT and USDC infrastructure comes first. Every other RWA category is a rounding error next to the stablecoin float your customers already hold and want to spend.

Tokenized Bonds and Treasury Securities

Tokenized debt instruments put bonds and treasury bills on-chain, and the sector has moved well beyond pilots. Platforms like Centrifuge and Maple Finance built the early infrastructure for on-chain credit markets, originating tokenized private credit against real-world collateral. Treat them as infrastructure providers, not investment tips.

The fastest-growing sub-category is tokenized US T-bills, past $6.8 billion in on-chain value by mid-2026. For finance teams, these are working capital tools, and the treasury section below covers how they're used.

Stablecoin Dominance and Merchant Acceptance

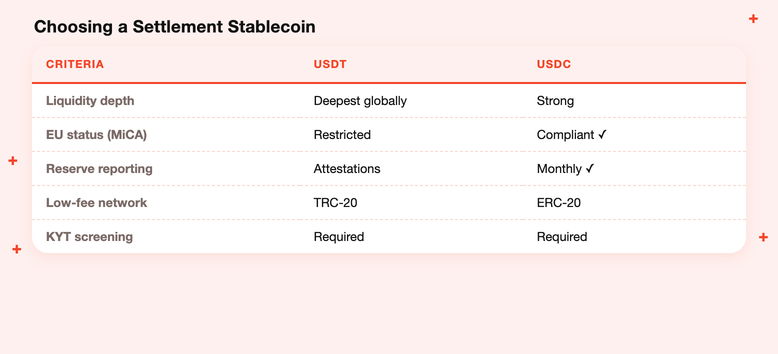

Stablecoins represent the overwhelming majority of RWA market activity, and that concentration creates a direct decision point for any business accepting crypto. Choosing between USDT and USDC isn't a preference question. Each carries distinct liquidity, compliance, and jurisdictional implications that affect your settlement speed and regulatory exposure.

Why USDT and USDC Lead the Market

USDT and USDC lead because liquidity begets liquidity. USDT offers the deepest markets and widest payer adoption across Asia, the Middle East, and Latin America, especially on TRON where transfer fees stay low. USDC trades on regulatory transparency: Circle publishes monthly reserve attestations and secured a MiCA-compliant EU licence.

Jurisdiction complicates the picture. Since MiCA's stablecoin rules took effect on 31 March 2025, EEA-regulated exchanges have delisted USDT because Tether didn't pursue authorization. Merchants serving European customers can still receive and hold USDT under ESMA's custody-and-transfer guidance, but converting it through EU venues got harder. That one regulatory fact should shape your default settlement asset in Europe.

Choosing Between Stablecoins for Settlement

Here's the checklist we'd put in front of any CFO making this call:

- Liquidity depth. Can you convert the volumes you expect to fiat or other assets without slippage, on the networks your customers actually use?

- Regulatory status per jurisdiction. Is the stablecoin authorized where you operate? USDC holds MiCA compliance in the EU; USDT dominates in most other regions.

- Counterparty risk. Who issues the token, what backs it, and how transparent are the reserves?

- Freeze and blacklist exposure. Both major issuers can freeze addresses. Screening payments before settlement matters more than most operators realize.

B2BINPAY supports both USDT and USDC across major networks with KYT screening applied to every incoming transaction automatically, so the compliance layer of this decision doesn't have to be built in-house.

[[aa-cta-blue]]

📢 One Wallet Layer for USDT, USDC and 350+ Assets

Consolidate multi-network stablecoin acceptance, auto-conversion, and fiat settlement under a single B2BINPAY account.

[[/a]]

Tokenized Treasuries for Corporate Treasury Management

Tokenized US Treasury products have moved from investment trend to operational tool for corporate cash management. A business holding idle on-chain balances can now earn short-dated government debt yields without exiting the crypto ecosystem or routing funds back through a bank. The practical question for finance operators is how these instruments work and what infrastructure they require.

How Tokenized T-Bills Work as Cash Alternatives

A tokenized T-bill fund issues tokens representing a claim on a portfolio of short-dated US government debt. Yield accrues daily, through a rising token price or rebasing, and redemption happens on-chain rather than through a broker.

Functionally, these products compete with money market funds. The yield profile is similar, but the wrapper behaves differently: 24/7 redemption requests instead of banking hours, on-chain auditability of holdings, and no bank intermediary required for settlement.

For a business already holding stablecoins from payment flows, moving idle balances into a tokenized T-bill product is an on-chain transaction, not a wire transfer and a two-day wait. The trade-off: final redemption to cash can take longer than the marketing suggests, which we cover in the risk section.

Franklin Templeton and Ondo Finance Examples

Two live products show how far this infrastructure has matured. Franklin Templeton's on-chain US Government Money Fund, with its BENJI token, holds around $1 billion in assets and paid a 7-day yield near 3.5% as of March 2026.

It's an SEC-registered 1940 Act fund, meaning traditional fund regulation applies to an on-chain wrapper. Ondo Finance's USDY, a yield-bearing note backed by short-term Treasuries and bank deposits, manages roughly $1.2 billion for non-US holders.

Neither is an endorsement; they're reference points, and BlackRock's BUIDL fund sits alongside them as the sector's largest by assets. Together they prove regulated, audited, yield-bearing cash alternatives now exist natively on-chain, and finance teams can evaluate them like any money market instrument.

RWA Compliance: What Businesses Must Understand

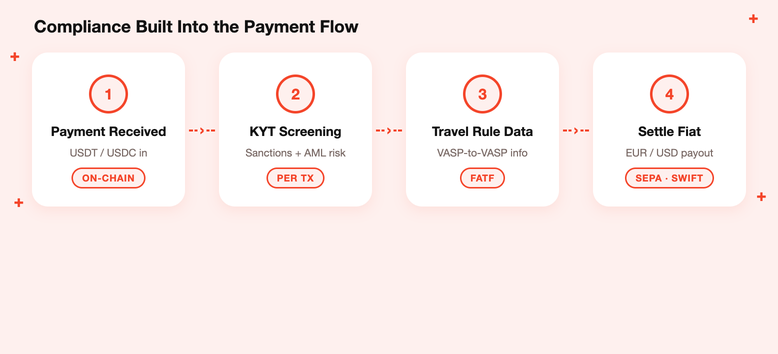

Accepting stablecoins or holding tokenized assets creates compliance obligations beyond standard crypto AML basics. KYT screening, Travel Rule data-sharing, and jurisdiction-specific rules each introduce concrete risks to handle before building on RWA infrastructure. This is where most operators underestimate the workload.

KYT Requirements for Stablecoin Transactions

KYT, or know your transaction, is ongoing monitoring that screens every individual transaction for sanctions exposure and AML risk. It's different from KYC, which verifies a customer's identity once at onboarding. KYT never stops: every incoming stablecoin payment gets checked against risk databases in real time.

Stablecoins carry specific KYT stakes because issuers can and do act on-chain. Tether and Circle both maintain blacklists, and a payment from a flagged address can leave you with frozen funds you cannot settle. Pre-screening incoming transactions is the only reliable protection, and doing it manually at real payment volume isn't feasible. Transaction screening belongs in your gateway, not in a spreadsheet.

Travel Rule Obligations for VASP-to-VASP Transfers

The FATF Travel Rule requires virtual asset service providers to share originator and beneficiary information on transfers above threshold amounts, and it explicitly covers stablecoin transfers between exchange and custodial wallets. As of the FATF's 2025 review, 85 of 117 surveyed jurisdictions had passed Travel Rule legislation, and the EU's Transfer of Funds Regulation now applies data-sharing requirements to crypto transfers with no minimum threshold.

In practice, stablecoin payouts to exchanges or receipts from custodial platforms trigger data obligations your infrastructure must fulfil automatically. A licensed VASP whose systems handle Travel Rule messaging removes a compliance project most finance teams aren't staffed to run.

[[aa-cta-grey]]

📢 Compliance Built Into Every Transaction

B2BINPAY applies KYT risk scoring and Travel Rule messaging automatically, backed by regional VASP licences.

[[/a]]

Key Risks of RWA Tokenization

RWA tokenization introduces risks that differ materially from holding native crypto assets. Liquidity constraints, smart contract vulnerabilities, and custody arrangements each create operational exposure, and honest evaluation of all three should happen before tokenized assets enter your payment or treasury workflows. Regulatory uncertainty sits across all of them, since rules for tokenized securities are still forming in most jurisdictions.

Liquidity and Redemption Risk

Tokenized doesn't mean instantly liquid. Stablecoin liquidity is near-instant on major networks, but tokenized bond and T-bill redemptions can run on T+1 or longer windows depending on the issuer's process for selling underlying assets and settling cash.

That gap matters for cash flow planning. If a tokenized T-bill position is working capital, you need to know how long a full redemption takes under normal and stressed conditions. Secondary market depth for many tokenized securities remains thin, so exiting a large position quickly may cost more than the yield earned. Plan redemption timing the way you'd plan any liquidity ladder.

Smart Contract and Custody Risk

Every tokenized asset inherits the risk of the code it runs on. Smart contract bugs have drained protocols before, and a token wrapper is only as safe as its contract and the bridge it crosses. Wrapped tokens that move RWAs across chains add another contract layer, and each layer is additional attack surface.

Custody risk sits underneath: someone holds the actual T-bills or reserves backing your token. If that issuer defaults or its custodian fails, your token becomes a legal claim in a bankruptcy process, not spendable money. Read the redemption terms and custody structure before position size matters.

Build on Tokenized Infrastructure With B2BINPAY

Every thread in this article points the same direction. Stablecoins dominate RWA activity, so merchants need USDT and USDC acceptance done properly. Tokenized treasuries turn idle on-chain balances into productive cash, so finance teams need wallet infrastructure that holds and moves these assets safely. And compliance expectations keep tightening, so KYT and Travel Rule handling can't be an afterthought.

What a CFO or payments lead needs is one infrastructure layer that handles all of it: multi-network stablecoin acceptance, transaction-level KYT screening, automatic fiat settlement via SEPA and SWIFT, and enterprise wallets that consolidate treasury operations without in-house blockchain engineering.

That's the gap B2BINPAY fills, as a regulated practitioner rather than a software vendor. A licensed VASP processing payments for brokers, exchanges, iGaming operators, and high-volume merchants, B2BINPAY supports 350+ cryptocurrencies across 20+ blockchains with a flat 0.5% processing fee, 0% rolling reserve, and instant auto-conversion to EUR or USD. Merchant Wallets cover payment acceptance; Enterprise Wallets give treasury teams the custody, sweeping, and reporting layer that tokenized asset operations demand.

RWA-backed settlement is becoming standard faster than most payment stacks are adapting. The winners won't be the businesses that picked the perfect asset; they'll be the ones that built on infrastructure ready for whatever tokenized instrument comes next.

[[aa-cta]]

📢 Ready for the Tokenized Settlement Era?

Open a B2BINPAY account and start accepting stablecoins with compliance, conversion, and settlement handled for you.

[[/a]]

Frequently Asked Questions about RWA Tokenization

What are real-world assets in DeFi?

Real-world assets, or RWAs, are off-chain instruments such as fiat currencies, government bonds, and private credit that are represented on-chain as tokens.

Stablecoins are the most operationally familiar example: USDT and USDC are themselves RWAs, which is why their dominance directly shapes merchant payment acceptance decisions. For business operators, understanding RWAs matters less as an investment thesis and more as a framework for evaluating settlement assets and treasury instruments.

Why are stablecoins considered a major real-world asset use case?

Stablecoins represent the overwhelming majority of RWA market activity because they combine the programmability of blockchain tokens with the price stability of fiat-pegged instruments.

For merchants and brokers, this dominance has a direct operational implication: USDT and USDC carry the deepest liquidity pools and the widest payer adoption, making them the default settlement layer for crypto payment infrastructure. Selecting between them still requires evaluating jurisdictional regulatory status, counterparty risk, and KYT screening requirements, not just payer preference.

How are tokenized treasuries used by businesses and institutions?

Tokenized treasury products, such as on-chain representations of short-dated US government debt, let businesses earn yield on idle on-chain balances without exiting the crypto ecosystem or routing funds through traditional banking infrastructure.

Products from issuers such as Franklin Templeton and Ondo Finance offer daily yield accrual with on-chain redemption, functioning as alternatives to money market funds for corporate cash management. Businesses considering this approach need compatible wallet infrastructure that supports on-chain custody, auto-sweeping, and AML compliance at the account level.

What should merchants consider before accepting stablecoin payments?

Merchants should evaluate three factors before committing to a stablecoin acceptance strategy: liquidity depth on the networks their customers use, the regulatory status of each stablecoin in their primary operating jurisdictions, and whether their payment processor applies KYT screening at the transaction level. USDT faces restrictions for merchants serving European customers under MiCA, while USDC offers stronger regulatory transparency but shallower liquidity in some markets. A payment gateway with built-in KYT and multi-stablecoin support, such as B2BINPAY's Merchant Wallet, reduces the compliance burden of managing these variables manually.

What are the main risks of RWA tokenization in DeFi?

The primary risks fall into three categories: liquidity and redemption constraints, smart contract vulnerabilities, and custody risk tied to the underlying asset issuer. Tokenized bonds and treasury products may carry T+1 or longer redemption windows, which can affect cash flow planning for businesses using them as working capital alternatives.

Smart contract risk is compounded when wrapped RWA tokens move across chains, since each bridging layer introduces additional attack surface that businesses should assess before integrating these instruments into payment or treasury workflows.

Disclaimer: The service has legal and jurisdiction limitations. Please check T&Cs on https://b2binpay.com/en/risk-disclaimer

.svg)