Every quarterly P&L review for an ecommerce operator runs through the same line items: card fees at 2–5% of revenue, chargebacks eating another 50–100 basis points, settlement holds locking up working capital, and reconciliation labor that never actually scales down. The real question isn't whether crypto payment infrastructure is novel — it's whether the math justifies adding it alongside existing checkout rails.

This article is a CFO-level evaluation framework, not a how-to-accept-bitcoin explainer. We'll cover the true cost of card processing (including hidden line items), how an ecommerce crypto payment gateway actually works for merchants, the quantified fee and settlement delta, and the compliance infrastructure regulated operators need to verify before onboarding. Framing adoption as operational timing rather than trend: stablecoin transfer volume reached $27.6 trillion in 2024, exceeding the combined volume of major card networks, according to the Federal Reserve's work on payment stablecoins.

Key Takeaways

- An ecommerce crypto payment gateway can reduce card-fee pressure and remove chargeback risk, which protects gross margin on online sales at scale.

- Auto-conversion and fiat settlement let merchants accept digital assets without holding volatile balances or changing treasury workflows.

- Blockchain networks operate continuously, so crypto payment infrastructure supports faster settlement visibility and fewer delays from banking cutoffs or processor holds.

- For regulated merchants, evaluation should include KYB onboarding, AML and KYT controls, and reporting built for reconciliation and audits.

- API, plugin, and hosted checkout options let teams go live without building wallet infrastructure in-house.

What Card Processing Is Actually Costing Your Business

Total card acceptance cost is rarely the number on the merchant statement. The headline MDR hides at least five additional cost vectors: interchange paid to issuing banks, assessment fees paid to card networks, processor markup, fraud-prevention tooling, reserve drag on disputed or high-risk transactions, and the labor cost of reconciling it all monthly.

For a $10M-revenue online store, a 2.9% blended rate is $290K of fees — before chargebacks, dispute fees, and reserves. U.S. Bank has documented how much of the cost in modern payment systems is structurally opaque, with fee stacks designed to make true acceptance cost difficult to model. For a CFO, the effect is gross-margin compression that doesn't appear on any single line item.

The Hidden Fee Stack: Interchange, Assessment, and Processor Markup

The fee stack splits three ways. Interchange is what the acquiring bank pays the issuing bank — roughly 1.5–2.5% depending on card type (rewards and corporate cards cost more). Card-network assessment is what Visa, Mastercard, and Amex charge per transaction, usually 0.13–0.15%. Processor markup is what the payment company adds on top — variable, negotiable, and often hidden inside a blended rate.

A merchant receiving a 2.9% "flat rate" quote is paying roughly 2.1% interchange + 0.14% assessment + 0.66% processor markup — and the processor markup is the only component that's actually negotiable. That framing usually doesn't appear in a pricing conversation until a finance team forces it.

Chargeback Fraud as a Revenue Leak, Not Just an Inconvenience

Chargebacks are a margin problem, not a customer-service problem. A $100 disputed transaction doesn't just lose $100 in revenue — it loses the cost of goods, the fulfillment cost, the $15–$40 dispute fee the processor charges, and the labor cost of preparing evidence. At 1% chargeback rate on $10M GMV, that's roughly $100K in direct revenue loss plus another $30–40K in operational overhead.

Blockchain settlement is different by design. Once a transaction is confirmed on-chain, it cannot be reversed through card network dispute rules. This matters most for high-risk ecommerce verticals, cross-border merchants, and digital goods sellers, where friendly fraud routinely drives chargeback rates well above the 0.1% general-commerce benchmark.

How an Ecommerce Crypto Payment Gateway Works

A crypto payment gateway sits as middleware between customer wallet activity and merchant settlement. The merchant never holds the asset, the customer never manages a blockchain integration, and the checkout flow looks functionally identical to a card redirect from the buyer's perspective. Everything interesting happens in the processing layer.

For ecommerce teams, the mental model is: existing checkout continues to exist, the gateway sits alongside it as another payment method, and settlement routes back to bank accounts via SEPA or SWIFT. Stablecoins handle the technical heavy lifting; the merchant's P&L sees fiat. The Federal Reserve work on stablecoins notes 24/7 processing and faster cross-border settlement as the structural reason adoption is accelerating, not hype.

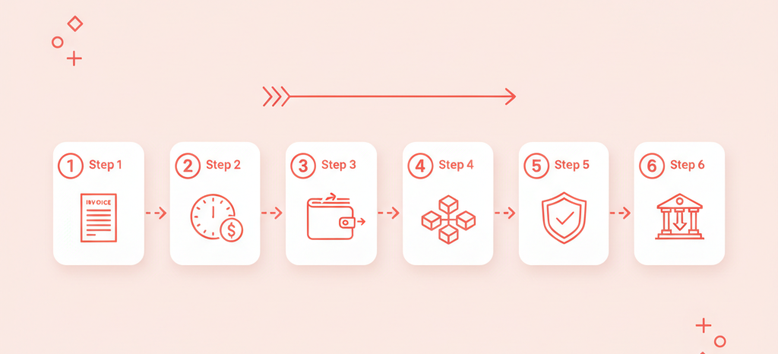

From Customer Checkout to Merchant Settlement in Six Steps

- Invoice creation — merchant backend calls the gateway API with amount and accepted currencies

- Rate lock — gateway fixes the crypto amount for a defined window (usually 10–15 minutes)

- Customer payment — buyer sends from their wallet (BTC, ETH, USDT, USDC are typical; stablecoins dominate in practice)

- Blockchain confirmation — network produces required confirmations (seconds to minutes depending on chain)

- Gateway verification — gateway verifies on-chain data, runs KYT, and updates invoice state

- Merchant settlement — funds auto-convert if configured and route to merchant account

For most ecommerce use cases, stablecoins are the practical payment currency because they eliminate the rate-lock risk and keep the customer-side UX simple. Bitcoin and Ethereum are accepted, but not optimal for high-frequency small-ticket commerce.

Auto-Conversion and Fiat Settlement: Accepting Crypto Without Holding It

Auto-conversion is the feature that makes this category adoptable for traditional treasury teams. At the moment of confirmation, the gateway swaps incoming crypto into the merchant's chosen fiat or stablecoin, at the locked rate, before the funds ever sit on the merchant's balance sheet. Volatility risk between payment and payout is structurally eliminated.

Chainalysis has documented stablecoins as payment infrastructure rather than speculation — primarily used for treasury operations, cross-border transfers, and merchant settlement. B2BINPAY's Merchant Wallet runs this pattern natively: customer pays in their preferred crypto, merchant receives EUR or USD in their bank account under 24 hours, and the treasury team never touches a blockchain wallet.

The CFO-Level Cost Comparison: Crypto Rails vs. Card Processing

This is where the evaluation gets concrete. Most competitor content stops at feature lists. For a CFO modeling whether to add a crypto rail alongside existing card processing, three numbers matter: the fee rate delta, the chargeback exposure delta, and the working-capital impact of settlement timing. All three favor crypto at volume.

Fee Rate Differential: 0.5–1% vs. 2–5% at Scale

Crypto payment processors typically charge 0.5% to 1% per transaction, with some enterprise providers coming in below that range. Traditional card processing runs 2% to 5% once interchange, assessments, and processor markup are summed, per Federal Reserve analysis. The spread is 150–400 basis points.

For a $10M-revenue online store running a 15% operating margin, shifting 20% of volume ($2M) from cards at 2.9% to crypto at 0.75% saves $43K in direct fees annually. For a $50M merchant, the same shift saves $215K. Those numbers don't include chargeback savings, reserve release, or reconciliation labor reduction — all of which compound the headline savings.

Working Capital Freed by Faster Settlement Cycles

Card settlement cycles run T+1 to T+3 depending on the acquirer, with high-risk merchants often facing T+5 holds or rolling reserves of 5–10% held for 90–180 days. Crypto settlement is near-instant at the network layer, with fiat payout under 24 hours for enterprise gateways like B2BINPAY (via SEPA or SWIFT).

The working-capital math: a $1M weekly processor at T+3 has $3M continuously tied up in float. Moving $500K of that weekly volume to same-day crypto settlement frees $1.5M of working capital on a rolling basis. At a 6% blended cost of capital, that's $90K annually in freed financing cost — before the operational benefits of inventory planning, ad-spend pacing, or vendor payment timing improve.

Compliance Infrastructure: What Regulated Merchants Must Verify Before Onboarding

Compliance infrastructure in this category means the combined KYB (know-your-business), KYC (know-your-customer), KYT (know-your-transaction), sanctions screening, transaction monitoring, and licensing posture of the gateway provider. For regulated verticals — iGaming, Forex, cross-border marketplaces — this is a procurement criterion, not a disclaimer.

The compliance checklist for an ecommerce CFO evaluating a crypto payment gateway:

- KYB onboarding: documented business verification with ultimate beneficial owner review

- AML and KYT: on-chain transaction monitoring applied programmatically, not sampled after the fact

- Licensing: regulated VASP status in relevant jurisdictions (MiCA in the EU, US frameworks evolving)

- Sanctions screening: OFAC, EU, UN sanctions list checks on both counterparties

- Reporting: exportable transaction logs and audit trails matching internal control requirements

Regulatory clarity has improved meaningfully. MiCA went into full effect across the EU in 2024, and US frameworks continue evolving for stablecoin issuers and processors. Merchants evaluating providers now have documentary evidence to assess, not just marketing claims. See the crypto payment gateway comparison for a side-by-side of major providers on these criteria.

Start Accepting Crypto Payments Without Rebuilding Your Stack

The decision framework for an ecommerce CFO comes down to four questions: Does the provider preserve margin at scale? Does it automate conversion so treasury workflows don't change? Does it shorten settlement to free working capital? Does it fit existing checkout infrastructure with minimal developer lift? An enterprise-ready gateway answers all four with evidence, not claims.

B2BINPAY's Merchant Wallet was built around exactly this profile — flat, transparent processing fees, 0% rolling reserve, auto-conversion of 70+ tokens to EUR or USD, fiat payout under 24 hours via SEPA or SWIFT, and KYT plus AML tooling embedded at the API layer rather than bolted on. The result is a crypto payment rail that a CFO can model, a compliance team can audit, and an engineering team can integrate in days.

[[aa-cta]]

Ready to evaluate the numbers on your own volume?

B2BINPAY's regulated crypto payment infrastructure with 0% rolling reserve and sub-24-hour fiat settlement.

[[/a]]

Frequently Asked Questions about Ecommerce Crypto Payments

How does ecommerce crypto payment integration work for merchants?

An ecommerce crypto payment gateway creates an invoice, receives the customer's transfer, monitors blockchain confirmations, and posts a settlement result back to your checkout. B2BINPAY Merchant Wallet offers API, hosted checkout, and platform plugins, so merchants can go live without building wallet, compliance, or reconciliation logic in-house. The customer-side UX matches a standard card redirect.

Can I accept crypto payments and still receive fiat currency?

Yes — auto-conversion lets the gateway swap incoming crypto into your chosen fiat or stablecoin at receipt, limiting volatility exposure to near zero. B2BINPAY Merchant Wallet supports automatic conversion of 70+ tokens to USD or EUR with fiat settlement in under 24 hours, so finance teams avoid holding volatile assets entirely.

How do crypto payments eliminate chargebacks?

Blockchain payments reach settlement finality after network confirmation, which means the transfer cannot be reversed through card-network dispute rules. For ecommerce operators, this reduces fraud leakage tied to friendly fraud, dispute fees, and reserve pressure that accompany card acceptance. Settlement finality varies by network, from seconds on Solana to roughly 12–15 minutes on Bitcoin.

How do crypto payments compare to card processing fees?

Stablecoin transfers on efficient networks can cost only cents in network fees, while card rails layer processor, FX, and dispute costs. Crypto processors typically charge 0.5–1% flat; card processing runs 2–5% total cost once all fees are summed. For CFOs, the bigger difference is usually the total fee stack, because chargebacks, FX spreads, and reserve holds can erode margin beyond headline rates.

Do I need KYB and KYT checks to accept ecommerce crypto payments?

Usually, yes. Regulated gateways verify your business through KYB and screen transactions with AML and KYT controls before enabling merchant processing. This matters most in regulated sectors — Forex, iGaming, high-risk ecommerce — where provider compliance directly affects onboarding risk. Regulatory clarity has improved under MiCA in the EU and evolving US frameworks, which makes documented provider compliance easier to verify.

.svg)