In the world of financial markets, where online transactions and electronic transfers take place, securing your payments with a regulated processor is essential. This is especially important in light of the increasing online frauds and scamming activities that drain peoples wallets of funds.

The money transfer license ensures that the payment processor complies with applicable laws and regulations and that your funds are less likely to be part of a financial crime. Businesses that deal with cryptocurrencies choose a licensed money courier to safeguard their and their users assets, given the immutable nature of virtual coins.

Lets get into more detail about what is a money transfer license and what sets it apart from other payment processors.

[[aa-cta]]

Crypto Swaps

Rebalance Your Crypto Portfolio Instantly

Convert any supported token to another in a single click at institutional VWAP rates. Zero withdrawal fees, transparent pricing, and instant execution — all within your B2BINPAY account.

[[/a]]

Understanding Money Transfer License

Money transmitters are entities that send funds between two parties that are geographically separated across borders. Usually, these operators charge certain fees for their services in the form of a percentage of the transferred amount or a fixed charge.

Wire transactions are the simplest form of money transfers that have evolved as credit cards, tangible assets, and cryptocurrencies entered the conversation. This opened the door for illegal activities to exist, claiming to engage in money transmitting while conducting money laundering.

This necessitated issuing a fiscal management permit: a money transfer license, which indicates that the transaction is being handled by a legal and reliable entity.

Functions of Money Transmitters

While the term money transmitting is broad, European financial regulators aim to promote this concept as MiCA regulations become effective in 2024. Money transfer services include the following.

- Transfer funds: money transmitters send funds from one person (sender) to another (receiver) for a service fee. Payment methods vary according to the transfer destination and origin.

- Sending remittances: Entailing transferring money across borders, usually from immigrants to their homelands, which increases foreign currency inflows.

- Payment services: Money transmitters facilitate purchases of goods and services, including invoice payments and recurring payouts.

- Currency conversion: Money transmitting activities also span exchange from one currency to another for individuals, businesses, or as part of international trade agreements.

- Non-bank financial services: These entities also offer non-banking services, such as paying utility bills and insurance companies.

Why Do You Need a Money Transfer Business License?

If you are operating a financial company tasked with sending money across borders or offering banking and non-traditional banking services, obtaining a money transfer license boosts customer confidence in your company.

Users are becoming more aware of online scam schemes, especially financial operators and exchange companies that take their money without actually delivering it to the intended recipient. Therefore, this can attract more users to your money service business.

On the other hand, if you own a crypto brokerage or trading company, finding a licensed MTL crypto is crucial to have legal backing on your capital storage and transfers.

Money Transmitter License Types in Europe

Money transfer businesses are classified by European standards into two categories: payment institutions and E-Money operators. Each type is given a different license issued and observed by the Electronic Money Directive (EMD2) and Payment Service Directive (PSD2), which define the distinction between these two types as follows.

Payment Institution License

PI licenses are the most widespread type for payment gateways and financial institutions in the European Union. They can be found on most e-commerce sites and online service platforms.

These entities functions range from offering payment account services, including money withdrawals, deposits, and internal exchanges, as well as taking and paying debts and credit transfers.

A payment institution license is mostly chosen by financial institutions that deal with remittances, manage non-banking monetary accounts, and issue payment instruments.

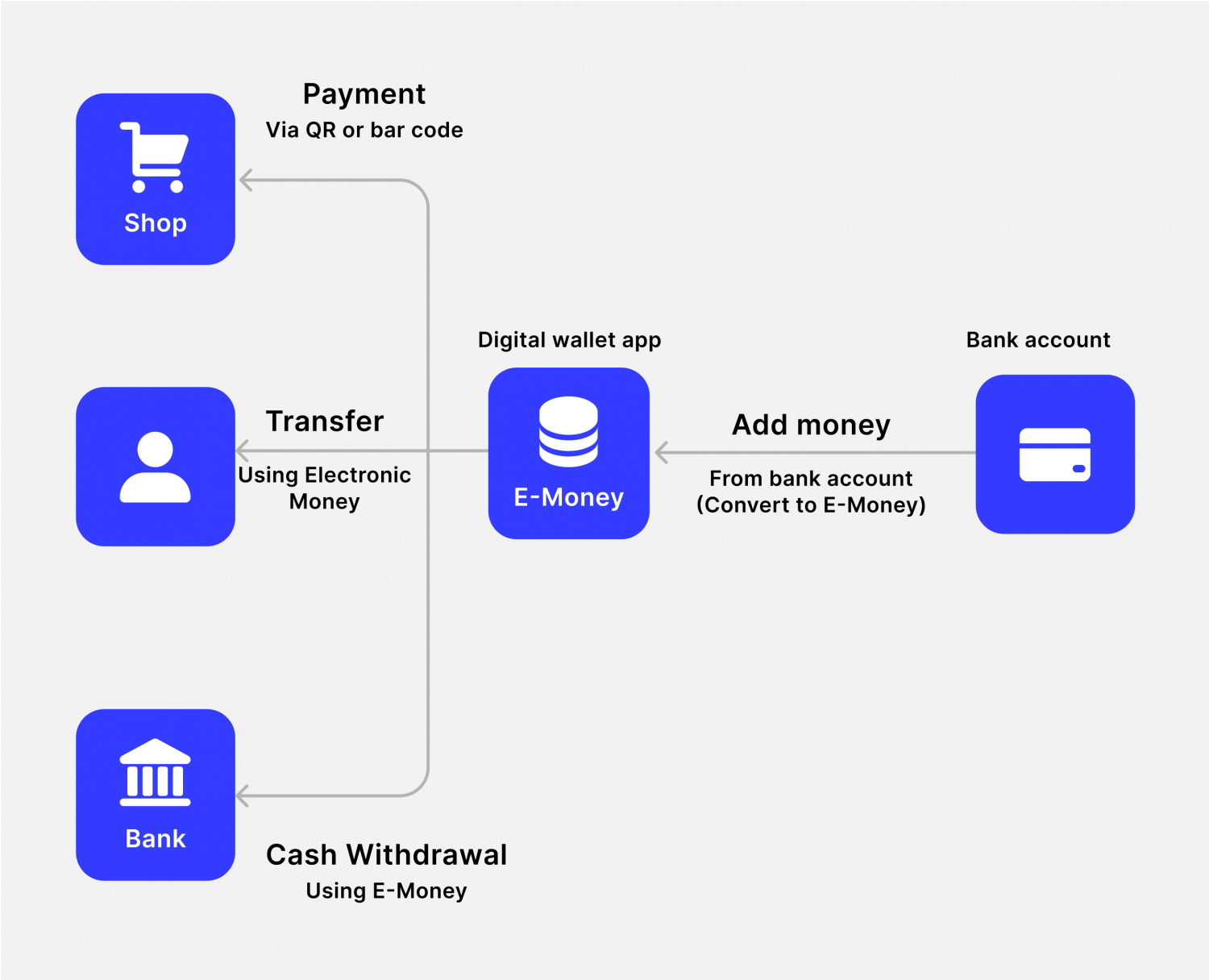

E-Money Institution License

The European Central Bank (ECB) defines e-money as an electronic means of payment that resembles the physical Euro in all EU states.

[[aa-note]]

Cross-chain token swaps between non-compatible blockchains typically require wrapped assets or bridge protocols, each adding settlement risk. Providers that aggregate off-chain liquidity avoid these mechanics.

[[/a]]

E-money is used to pay for goods and services online through mobile phone applications, digital asset wallets, or credit cards. Operators that provide payment services must obtain an electronic money institution license to perform online transactions legally.

Electronic money institutions are primarily concerned with developing the most advanced payment solutions and cooperate with FinTech firms to provide users with a wide range of non-banking financial services.

Money Transmitters vs Processors

Transferring and processing money can be similar. In fact, both entities are tasked with sending cash between users or businesses. However, there are a few differences between them. Lets break them down.

- Transacting funds: Transmitters mainly move funds from senders to receivers for different purposes, such as remittances, personal transfers, and business reimbursements. Processors fulfil payments for purchasing goods and services through online purchases, point of sale, recurring charges, crypto payments, and credit/debit card operations.

- Regulatory compliance: transmitters and processors are subject to financial regulations, requiring registration at fiscal authorities such as FinCEN in the US and the EBA in Europe. Both agencies may have different provisions, but they regulate policies to comply with anti-money laundering and combat financial crimes.

- Supported services: Money transfer entities may offer bill payment, currency exchange services, and non-bank operations. Processors may provide fraud protection, chargeback prevention, and crypto merchant services for paying with cryptocurrencies.

- User base: Transmitters serve individuals and businesses that want to send money from point A to B without using banks. On the other hand, processors serve a large number of users, including e-commerce sites, online stores, platforms, and businesses.

Money Transmitter License Crypto Requirements

If you are launching a payment processing startup, getting a money transfer license is crucial to boost your business and encourage clients to use your services. Therefore, preparing for a thorough licensing process that includes the following steps is essential.

Registration

Submit your application to your local regulator, such as the US FinCEN, EU EBA or UK FIU. The requirements may differ between jurisdictions, but they usually include business type declaration and plan, owner(s) information, organisational chart details, and internal operation projection and offered services.

Capital Requirements

Money-transferring agencies usually must declare operational capital before obtaining an MT license. Besides owning a particular amount in the account, regulators may require financial statement audits, providing sufficient cash reserves, the companys financial backings like bonds and other assets, and security protocols to safeguard users funds.

Checking Legal Records

Transferring and processing businesses are subject to legal checks to inspect the background of the organisations executives, board members, managers and owners. These checks may include criminal records, fingerprints, past financial sanctions or prosecutions, and tax records.

This policy is made to evaluate participants and ensure no financial criminals are involved in transferring or processing.

Compliance & Audits

Funds-transferring businesses must provide a compliance protocol for processing transactions and checking customers backgrounds. This includes KYC policies to prevent financial crimes, funding terrorism, money laundering, and other illegal money operations.

Ongoing Reporting

Both money transmitters and financial processors are required to submit periodic reports to regulators. These reports include transaction details, payment service user data, sources and destinations of transfers, and other documentation required by authorities.

Conclusion

[[aa-cta-grey]]

Merchant Wallet

Flat-Fee Crypto Payments That Scale

B2BINPAY charges a flat 0.25–0.40% per transaction regardless of volume. No percentage markups, no monthly fees, no withdrawal charges. The more you process, the more you save compared to card rails.

[[/a]]

A money transfer license requires financial processors and transmitters to register their businesses with local regulatory authorities. This ensures the legality of these companies and promotes confidence among customers, ultimately improving the fiscal ecosystem.

While money transfers are divided into two types: financial institutions and electronic money processors, both entities must obtain an MTL before serving e-commerce websites, online stores, crypto merchant accounts, and processing business payment transactions.

.svg)