Bitcoin transactions, much like any transactions in the traditional banking system, can trigger certain tax obligations, according to the IRS rulings. Consequently, any gains or losses from buying and selling digital assets will be considered capital gains/losses and subject to taxation. However, what about transferring your crypto to another wallet? Do you have to pay taxes on it? Let's dive into the specifics.

Basics of Crypto Taxation

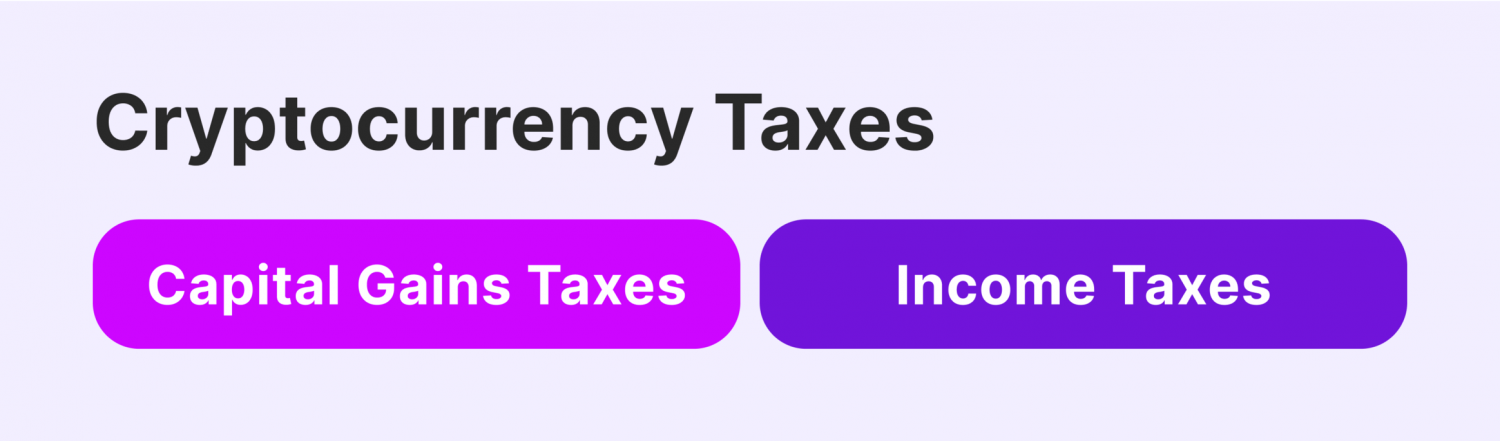

The taxation rules for cryptocurrencies can vary depending on the jurisdiction, as each country has its own set of regulations. However, the two most common ways that cryptocurrencies are taxed are capital gains and income.

[[aa-cta]]

Payment API

Integrate Crypto Payments in Hours

B2BINPAY's RESTful Payment API comes with full documentation, webhooks, and sandbox access. Connect your platform to 350+ cryptocurrencies without building blockchain infrastructure from scratch.

[[/a]]

In the US, the Internal Revenue Service (IRS) treats cryptocurrencies as property for tax purposes if you sell or exchange your crypto tokens for a profit, you must report the gains on your tax return and pay capital gains tax accordingly.

The tax rate for short-term capital gains (assets held for less than a year) ranges from 10% to 37%, while long-term capital gains (assets held for more than a year) are taxed at rates ranging from 0% to 20%, depending on your income bracket.

Similarly, in the United Kingdom, the HM Revenue & Customs (HMRC) agency treats crypto as property as well, which is also subject to certain taxes. If you sell or exchange cryptocurrencies and realise gains or losses, you must report them on your tax return and pay the corresponding capital gains tax.

Overall, these taxation principles are common among many countries, including Australia, Ireland, France, etc.

Is Sending Crypto to Another Wallet Taxable?

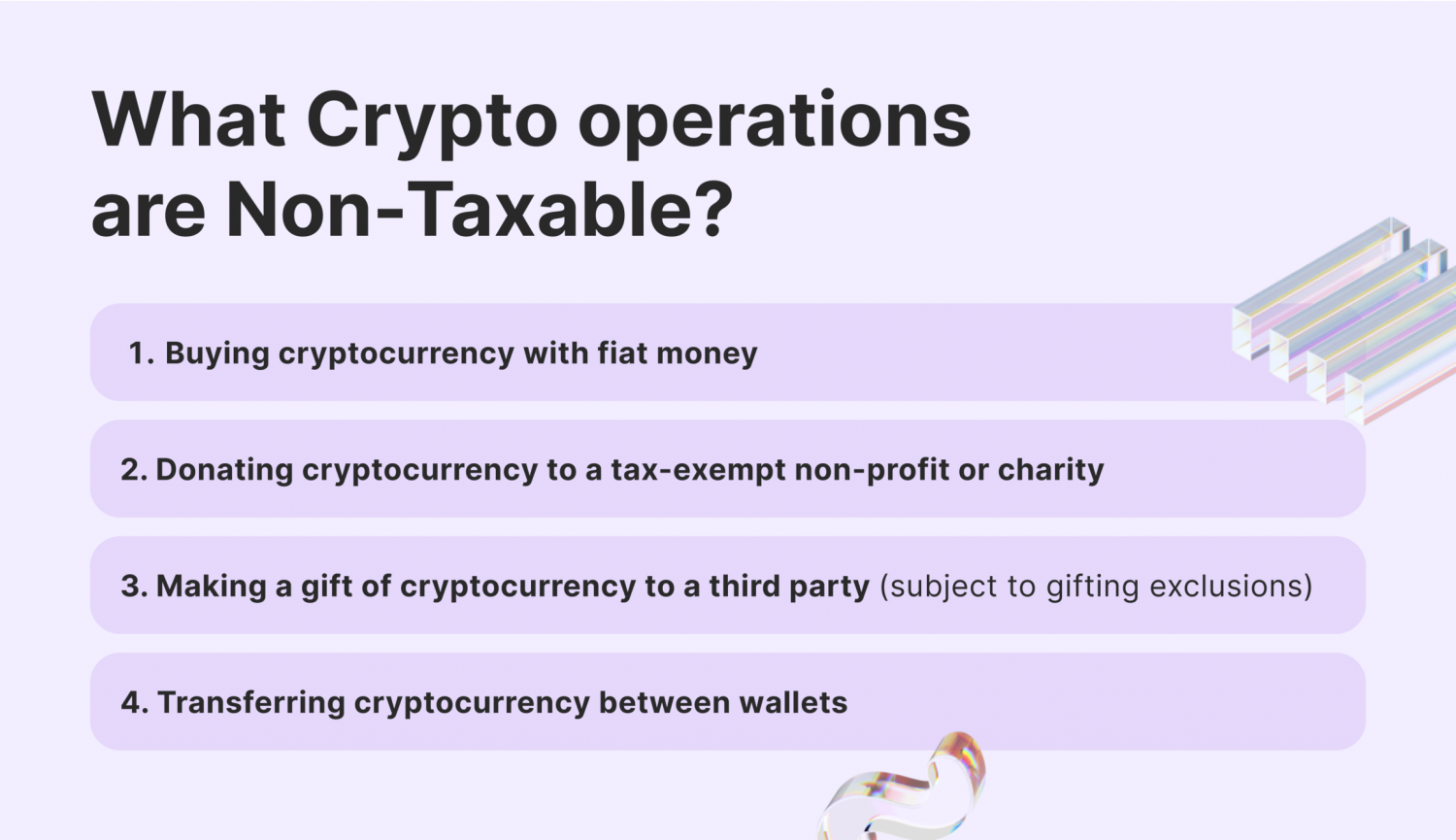

Typically, transferring crypto from one wallet to another is not considered a taxable event. This is because a wallet-to-wallet transfer does not involve selling or exchanging the cryptocurrency; you retain ownership of the cryptocurrency throughout the process.

It is important to note that while the transfer itself is not taxable, there are certain circumstances where tax liability may arise. These are some examples:

- Using cryptocurrency as payment for goods or services may be regarded as a taxable event, and income tax may apply.

- Similarly, sending cryptocurrency as a gift may have gift tax implications, depending on the quantity of cryptocurrency sent and the tax regulations in your area.

To ensure compliance with tax regulations, it is advisable to record all cryptic transactions and consult with a tax professional.

Reporting Requirements for Cryptocurrency Transfers

Reporting payments made in cryptocurrency is essential if you are a merchant or rely on crypto assets for income. While the specific reporting requirements may vary depending on the country, keeping detailed records of all crypto transactions and declaring them properly when filing your tax returns is important.

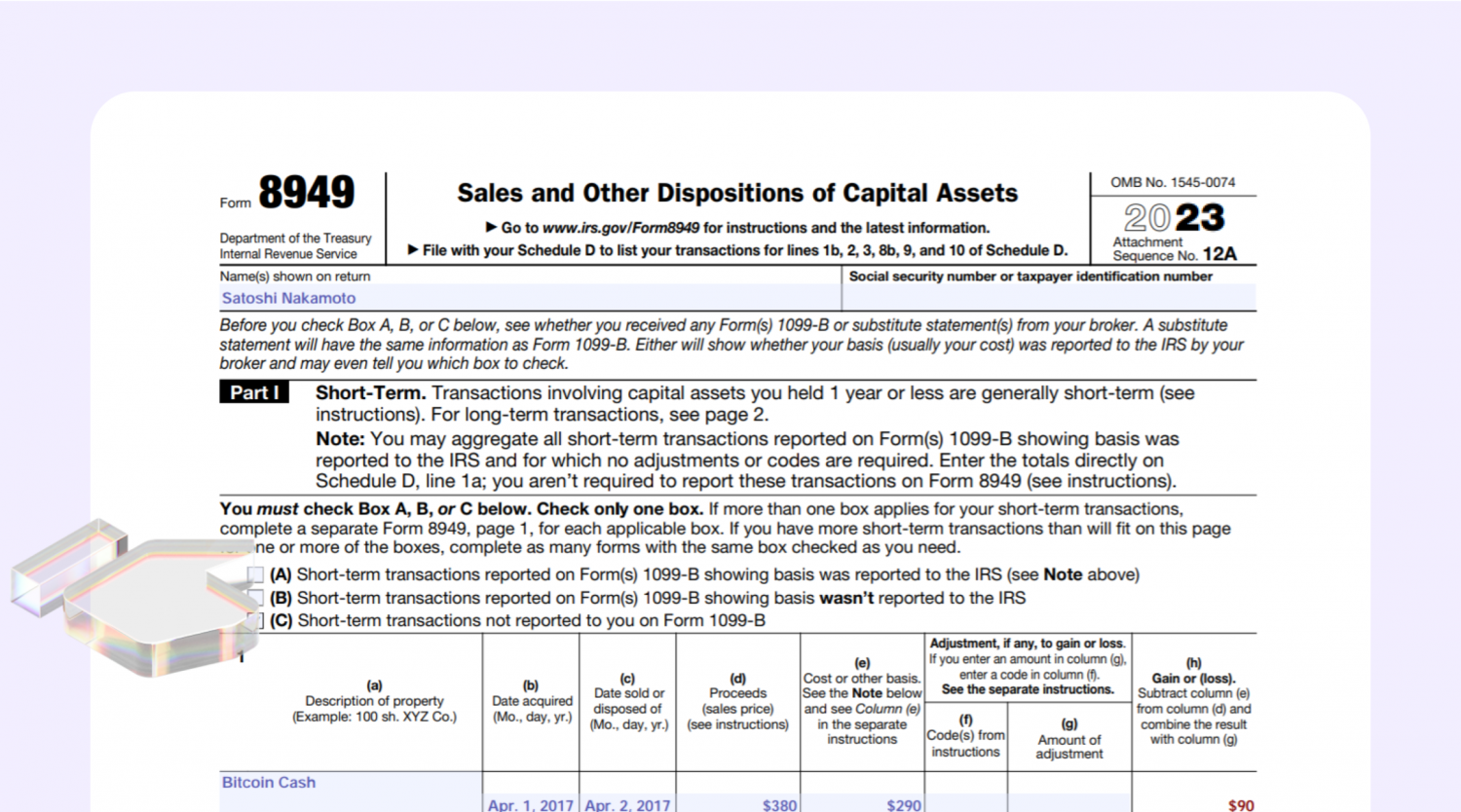

All crypto payments for goods or services must be reported to the IRS in the United States. This information can be reported on Form 8949 and Schedule D of the individual income tax return. To accurately report these transactions, taxpayers must include the cryptocurrency's fair market value at the time of the transaction and the cost basis of the asset.

In the UK, individuals earning from digital currencies must include their gains or losses in the Capital Gains Tax section of their tax return. All transactions must be documented accurately, including the dates, sums, and values of the cryptocurrency at the time of the transaction.

[[aa-note]]

RESTful APIs have become the standard for crypto payment integration, enabling businesses to automate the full payment lifecycle — invoice creation, status monitoring, conversion, and settlement — without manual steps.

[[/a]]

Deducting Transfer Fees and Crypto Taxes

In certain cases, expenses associated with crypto transactions may be eligible for deduction.

Generally, taxpayers can include transaction expenses in the property's cost basis if the transaction meets certain criteria. These criteria may include the transaction being an essential component of buying or selling the property or enhancing the underlying value of the property.

However, it should be noted that the IRS has not provided specific guidance on whether fees associated with wallet-to-wallet transfers meet these criteria. As a result, there are different approaches to reporting fees for such transfers, depending on the taxpayer's risk tolerance.

- Aggressive approach: Transfer fees are part of the property's cost basis. This approach assumes that wallet-to-wallet transfers are necessary for the buying or selling of the property and, therefore, can be included in the cost basis.

- Conservative approach: All wallet-to-wallet transfers are non-deductible since they are not directly linked to the purchase or sale of the cryptocurrency.

Is Converting Cryptocurrencies Taxable?

Converting one cryptocurrency to another, such as using Bitcoin to purchase Ethereum, is considered a taxable event because this action involves selling the original coin to acquire a new asset.

The IRS deems this transaction taxable as a disposal, and taxpayers will need to report and pay taxes on any capital gains realised from the conversion.

If you sell the original cryptocurrency at a higher price than what you initially paid for it, you will be liable to pay taxes on the capital gains.

What Crypto Operations Are Taxable?

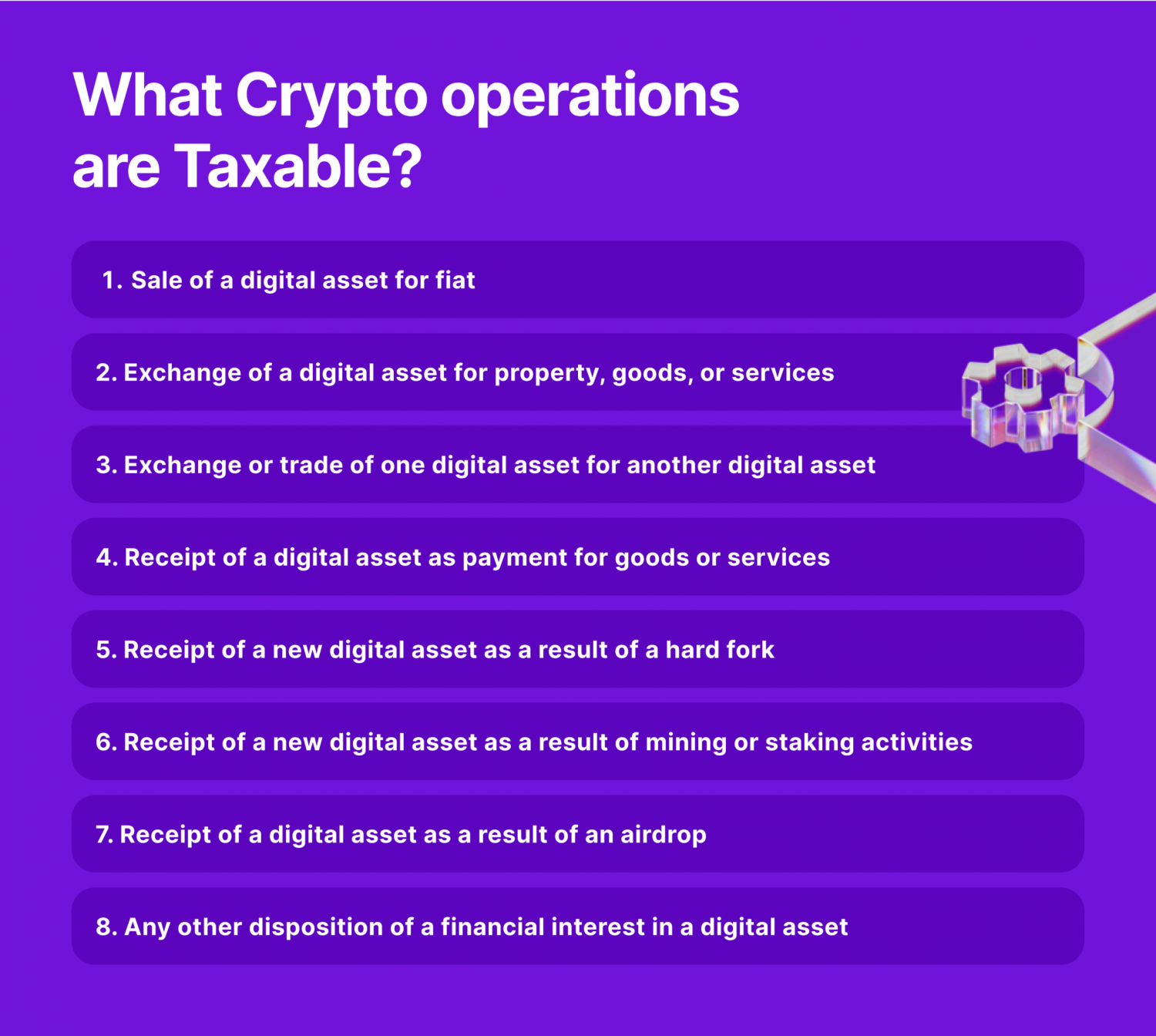

Depending on the cryptocurrency transaction, it can trigger different tax events, resulting in varying taxable consequences. Some common crypto capital gains tax events are:

- Purchasing goods or services with crypto: As mentioned earlier, this is considered a sale of the token and can result in a capital gain or loss based on the current value of the asset.

- Exchanging one virtual asset for another: If you traded one coin for another, you would need to submit a tax report of any gains or losses on the transaction.

- Mining cryptocurrency: Mining crypto can result in either regular income or business income, depending on the purpose and scale of your mining activities.

- Cashing out cryptocurrency: When exchanging crypto for fiat, you'll need to know the cost basis of the tokens you're selling. The capital gains or losses will be calculated based on this cost basis.

- Airdrops or hard forks: If new tokens are received, they may be subject to capital gains tax upon sale.

- Gifts and donations: Donating tokens to a tax-exempt organisation or gifting them to a third party may have varying tax implications, depending on the amount and purpose of the gift.

[[aa-cta-blue]]

Compliance Suite

One Platform. Full Regulatory Coverage.

Meet AML screening, Travel Rule, and transaction monitoring requirements through a single integration. B2BINPAY's Compliance Suite is built for regulated entities operating across multiple jurisdictions.

[[/a]]

Bottom Line

Understanding the tax rules for crypto transactions means keeping up with the latest regulations and being meticulous about recording your activities. Transferring crypto between wallets isn't taxable by itself, but other actions like trading one crypto for another, using crypto to pay for things, or mining can lead to tax obligations. Stay up to date with the latest info, seek advice from tax experts, and make sure you're following the rules properly to make correct financial decisions.

.svg)