The global economy is growing more interdependent, which makes money laundering and other forms of financial crime harder to prevent. Everywhere in the world, governments are taking new steps to detect and prevent financial crimes. Transaction monitoring (TM) is one example of such a tool. In this piece, we'll look at how the AML transaction monitoring system works to forestall financial wrongdoing.

What is Transaction Monitoring?

TM is the process of keeping track of consumer transactions, withdrawals or deposits, including assessing historical and current customer information and interactions to get a comprehensive picture of customer activity.

[[aa-cta]]

Compliance Suite

Built-In AML & Travel Rule Compliance

B2BINPAY integrates Crystal and Chainalysis for real-time KYT risk scoring on every transaction, plus Notabene for FATF Travel Rule compliance. Stay audit-ready without managing multiple compliance tools.

[[/a]]

Various tools and technologies are used to monitor electronic and non-electronic transactions, for example, credit card transactions, cash transactions, etc. Monitoring systems help recognise suspicious behaviour, which could signal money laundering or other fraudulent activity.

TM is obligatory for organisations that manage money on behalf of customers, whether individual customers or businesses, since it helps prevent money laundering and other money-related crimes.

How And Where Does Transaction Monitoring Work?

Transaction monitoring systems eliminate the need for manual transaction review. They use advanced analytics and machine learning algorithms to track customer transactions and automatically flag suspicious ones. For example, among the red flags that can trigger a monitoring system are the following:

- Anonymous entities - Using anonymous organisations to move money makes it more difficult for law enforcement to trace the money and identify criminals.

- Suspicious geographic activity - Typically, transactions from unusual geographic locations trigger monitoring systems and are further investigated.

- Large transfer amounts or frequent and unusual transactions - Transferring large sums or frequently occurring transactions might indicate money laundering activity.

- Layering - This refers to the type of money laundering when a significant amount of money is broken down into multiple layers using various accounts and financial institutions to conceal the source of funds.

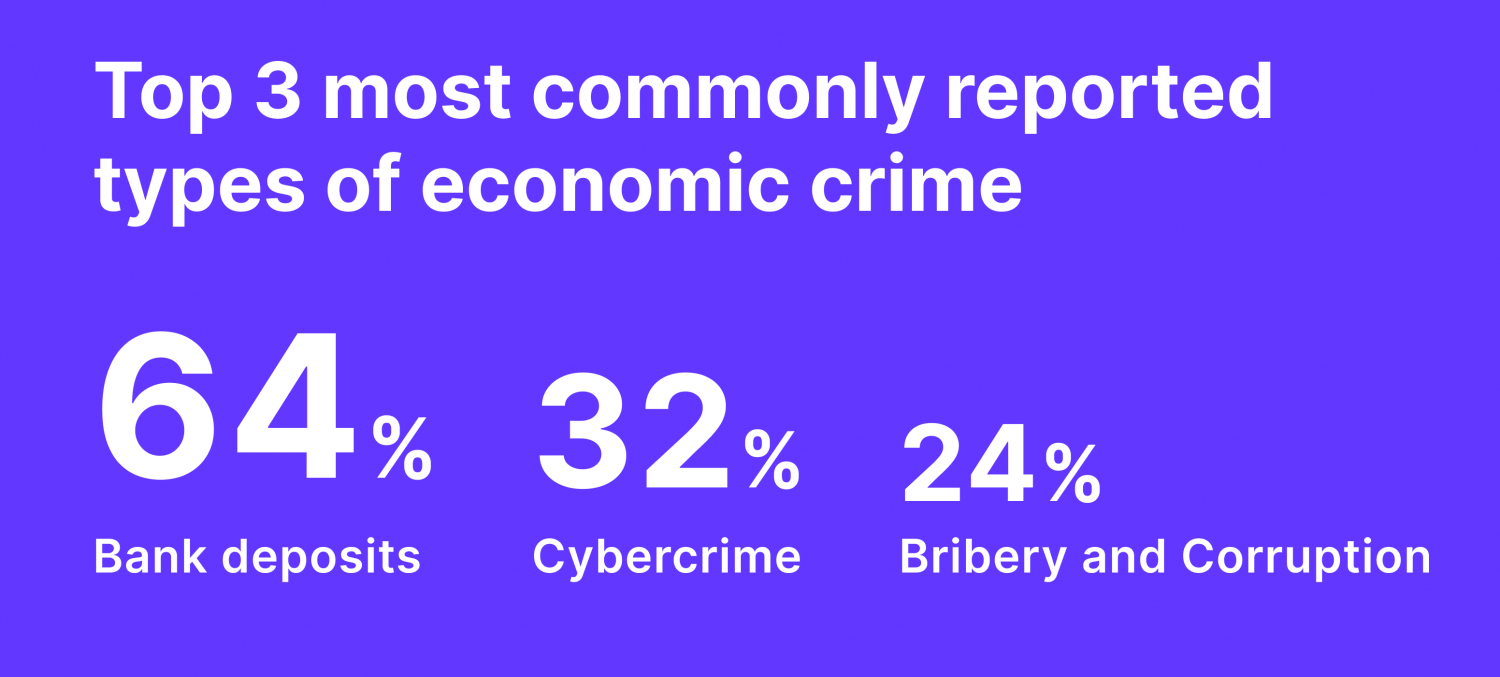

By monitoring transactions, finance institutions can detect and prevent associated crimes. Among many criminal acts that can be prevented thanks to proper TM are the following:

- Drugs trafficking

- Corruption

- Human trafficking

- Terrorist financing

- Bribery

- Fraud

- Laundering of money and other financial crimes

Transaction monitoring systems are an irreplaceable component for various financial institutions such as banks, investment firms or credit card companies. However, the systems can be used in other sectors that deal with customers' finance and may encounter illicit activity: insurance, accounting, the gaming industry, real estate and more.

What Is Transaction Monitoring In AML?

Anti-money laundering transaction monitoring is aimed at transactions that might signal money laundering.

Fraud transaction monitoring is a critical component of AML compliance; it is used to help a financial institution gain insight into customer activity.

Compliance analysts stick to a set of monitoring rules to define a suspicious transaction. They monitor information such as bank accounts for deposits, money transfers and withdrawals, etc.

The ultimate objective of transaction monitoring is to stop criminals from utilising companies' platforms and services to launder money. Similarly, AML transaction monitoring aids in creating evidence that regulators might employ to trace the money and punish the guilty.

As a result, transaction monitoring becomes a vital component of the AML strategy for companies subject to anti-money laundering laws.

[[aa-note]]

The FATF Travel Rule was extended to crypto in 2019 and has since been adopted by 40+ jurisdictions. Compliance requires VASPs to identify both the sender and recipient before processing qualifying transactions.

[[/a]]

What Is The Process Of AML Transaction Monitoring?

Banks and other financial institutions must keep track of their client's transactions while using their services to spot any unusual behaviour associated with laundering funds or other crimes. The potential risk of these transactions is then automatically determined by comparing them to internal regulations.

When suspicious behaviour is detected, specific transactional information is recorded, and a suspicious activity report (SAR) is sent to the relevant regulator within the specified time range.

Some other reports are also required, along with suspicious activity reports when a customer completes a transaction with specific characteristics. Each country's relevant authorities are in charge of analysing and looking into these reports.

When analysing transactions for suspicious behaviour, banks take many risk indications into account. These include:

- Geography - It refers to the indication of the locations where a transaction was initiated and completed and identifies whether the locations can be defined as high-risk regions.

- Amount - It refers to monitoring the sum of the transaction.

- Velocity - It refers to comparing the customer's average activity to the current activity and identifying whether it increased significantly.

- Recipient - It refers to defining whether transfer recipients are regarded as high-risk customers (for example, a recipient is on a company's watchlist, sanctions list, or a politically-exposed person).

Most AML procedures for monitoring transactions are performed as batch processes, meaning that the transactions are uploaded to the system for analysis at the end of the day.

However, transaction analysis can also be real-time when transactions are monitored as they occur. The regulation does not require a real-time transaction monitoring process, but it can help with quicker, more accurate decision-making and even real-time payments.

How Does an AML Transaction Monitoring Software Work

AML transaction monitoring software helps financial institutions implement their AML programs. AML software may be used to track and detect smaller, individual transactions and widespread suspicious activity comprising significant value assets.

AML software is commonly grouped into four main categories:

- Monitoring of transactions: This AML software focuses on finding suspicious trends and patterns in consumer transactions using historical data and the specifics of certain account profiles.

- Name screening: 'Some jurisdictions keep blacklists' of high-risk clients and businesses, and financial institutions are forbidden from doing business with them. This AML software helps swiftly locate banned individuals and flag them as suspicious. Screening is used to detect penalties, politically exposed persons (PEPs), and anyone obtaining negative media attention.

- Currency transaction reporting (CTR): Anti-money laundering software may be used to spot suspicious transactions involving substantial sums of money and a number of small transactions that add up to a sizable sum of cash.

- Compliance: AML software may be used to carry out compliance obligations on a daily basis. AML software's data management features may be used to track reports filed to financial authorities and records of staff training and planned audits.

Due to the complexity of the regulatory environment, AML software is a crucial component of the AML strategies of various financial institutions.

[[aa-cta-blue]]

Merchant Wallet

From 70+ Tokens to Your Bank Account

Every crypto payment automatically converts to USD or EUR and settles to your bank account. No manual steps, no custody risk, no chargebacks. B2BINPAY processes the transaction end-to-end.

[[/a]]

Conclusion

Despite the necessity, it may be difficult for firms to implement effective protocols for monitoring transactions and preventing money laundering. The complexity of financial transactions, the ever-evolving nature of financial crime, and the sheer volume of data to monitor make it challenging to detect malicious behaviour. However, keeping an eye out for fraudulent transactions is crucial for any enterprise dealing with monetary exchanges, and integrating software for monitoring payment transactions may be put in place to assist in discovering and preventing criminal activity.

.svg)